With global markets and interest rates moving in unpredictable ways, many investors are looking for strategies that don’t rely on guessing where the market is headed.

For fixed income investors, one key strategy to consider may be a bond ladder. By spreading maturities across different points in time, a bond ladder can give you exposure to a range of future rate environments, and the flexibility to reinvest as conditions change. It can also help deliver a steady rhythm of coupon payments and maturing principal, making it easier to build an income stream tailored to your personal timeline.

Read on for more on how to build and manage a successful bond ladder.

What's a bond ladder?

A popular way to hold individual bonds is by building a portfolio of bonds with various maturities: This is called a bond ladder. Ladders can help create predictable streams of income, reduce exposure to volatile stocks, and manage some potential risks from changing interest rates.

If yields are likely to fall, a bond ladder structure can help ensure that at least part of your bond portfolio is maintained at the (higher) yields that prevailed when you had originally invested in the ladder. Similarly, a ladder may be useful when yields and interest rates rise, because it regularly frees up part of your portfolio so you can take advantage of new, higher rates in the future. If all your money is invested in bonds that mature on the same date, they might mature before yields rise or after they have begun to fall, limiting your options.

By contrast, bonds in a ladder mature at various times in the future, which enables you to reinvest money at various times and in various ways, depending on where opportunities may exist. Ladders can also offer some protection from the possibility that rising rates might cause bond prices to fall, since bond holders are paid the full principal value of the bond when it matures (assuming the issuer stays in business and can make good on its borrowing as they come due).

"Laddering bonds may be appealing because it may help you to manage interest-rate risk, and to make ongoing reinvestment decisions over time, giving you the flexibility in how you invest in different credit and interest rate environments," says Richard Carter, Fidelity vice president of fixed income products and services. (Note that the chart that follows is for illustrative purposes only and that yields are subject to changing market conditions.)

Things to know before building a bond ladder

Before building a bond ladder, consider these 6 guidelines.

1. Know your limitations

Ask yourself—or a financial professional—whether you have enough assets to spread across a range of bonds while also maintaining adequate diversification within your portfolio. You don't want all of your money in any one type of investment. Even bond enthusiasts recommend leaving at least 40% of your portfolio in stocks. Bonds are typically sold in minimum amounts of $1,000 or $5,000, and it can sometimes be harder to trade small quantities. That’s why you may need a substantial investment to achieve diversification if you’re going to invest in individual bonds containing credit risk, such as corporate bonds or municipal bonds.1 For smaller amounts, consider a Treasury or CD Ladder, where credit risk is considerably reduced.

Make sure that you also have enough money to pay for your needs and for emergencies. You should also consider whether you have the time, willingness, and investment acumen to research and manage a ladder yourself. If not, you may be better off getting help with your ladder or opting instead for a bond mutual fund or separately managed account.

2. Hold bonds until they reach maturity

To invest with bond ladders, you should have a temperament that will allow you to ride out the market’s ups and downs. That’s because you need to hold the bonds in your ladder until they mature to maximize the benefits of regular income and risk management. If you sell early, you will risk losing income and may also incur transaction fees. If you can't hold bonds to maturity, you may experience interest-rate risk similar to a bond fund with comparable duration, which you may want to consider instead.

How many issuers might you need to manage the risk of default?

| Credit rating | # of different issuers |

|---|---|

| AAA US Treasury | 1 |

| AAA-AA municipals | 5 to 7 |

| AAA-AA corporate | 15 to 20 |

| A corporate | 30 to 40 |

| BAA-BBB | 60+ |

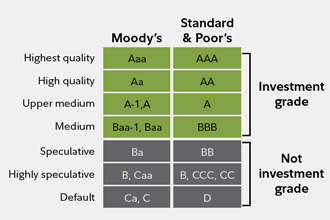

3. Use high-quality bonds

Ladders are intended to provide predictable income over time, so using riskier lower-quality bonds makes little sense. To find higher-quality bonds, you can use ratings as a starting point. For instance, select only bonds rated "A" or better. But ratings can change, so you should do additional research to ensure you are comfortable investing in a bond you may potentially hold for years. If you are investing in corporate bonds, particularly lower-quality ones, you need more issuers to diversify your ladder. The prior table suggests how many issuers you may need.

How do bond ratings work?

Moody's and Standard & Poor's are independent credit rating services that analyze the financial health of bond issuers. The ratings they assign help investors assess how likely an issuer is to be able to make principal and interest payments to bondholders.

4. Don't chase the highest rates or yields

An unusually high yield relative to similar bonds often indicates the market is anticipating a downgrade or perceives that bond to have more risk than others, and has traded its price down and increased its yield. Municipal bonds can be an exception. Some well‑known muni issuers offer high coupons and trade at premium prices, which lowers their yield‑to‑maturity. Still, investors sometimes favor these familiar, highly rated issues over smaller but still creditworthy alternatives.

5. Keep callable bonds out of your ladder

Part of the appeal of a ladder is knowing when you get paid interest, when your bonds mature, and how much you need to reinvest. But when a bond is called prior to maturity, its interest payments cease and the principal is returned to you, possibly before you want that to happen.

6. Think about time and frequency

Another feature of a ladder is the length of time it covers and how often the bonds mature and return principal. A ladder with more bonds will require a larger investment but will provide a greater range of maturities. If you choose to reinvest, a ladder with more bonds can afford more opportunities to gain exposure to future interest-rate environments.

How to build a bond ladder

Here’s an example of how you can build a ladder using Fidelity's Bond Ladder tool. Mike wants to invest $400,000 to produce income for about 10 years. He starts with his investment amount—though he could also have chosen a level of income. He sets his timeline and asks for a ladder where bonds are maturing on a semi-annual basis. Then he chooses bond types. In order to be broadly diversified, each rung contains a range of bonds and FDIC-insured CDs with various investment grade credit ratings.

Mike chooses eligible bonds for each rung and, as he does so, the tool shows a summary of the ladder, including the total par and market values, the average yield to maturity, and yield to worst.

Displayed rates of return, including annual percentage yield (APY), represent stated APY for either individual certificates of deposit (CDs) or multiple CDs within model CD ladders, and were identified from Fidelity inventory as of the time stated. For current inventory, including available CDs, please view the CDs & Ladders tab.

While a well-diversified bond ladder does not guarantee that you will avoid a loss, it can help protect you the way that any diversified portfolio does, by helping to limit the amount invested in any single investment. Also, a bond ladder systematically returns cash to you: coupon payments along the way, plus principal when each rung matures. Because those maturities are staggered, you get a predictable, recurring flow of cash that you can either spend or reinvest. That structural cash‑flow pattern is what makes ladders useful for creating an income stream tailored to a specific time horizon or need.

Need help building a bond ladder? On Fidelity.com, you can research fixed income solutions or fixed income tools and services. Prefer to talk to an expert? Call our specialists in fixed income at 800-544-5372.