Stock prices have soared in recent months, and headlines are full of speculation about whether the rally can last. But history shows that trying to outguess the market often backfires. Instead of chasing headlines or timing trends, focusing on a disciplined, long-term strategy can help you avoid common investing myths and stay on track toward your goals.

Myth #1: I can wait for the best time to get in the market

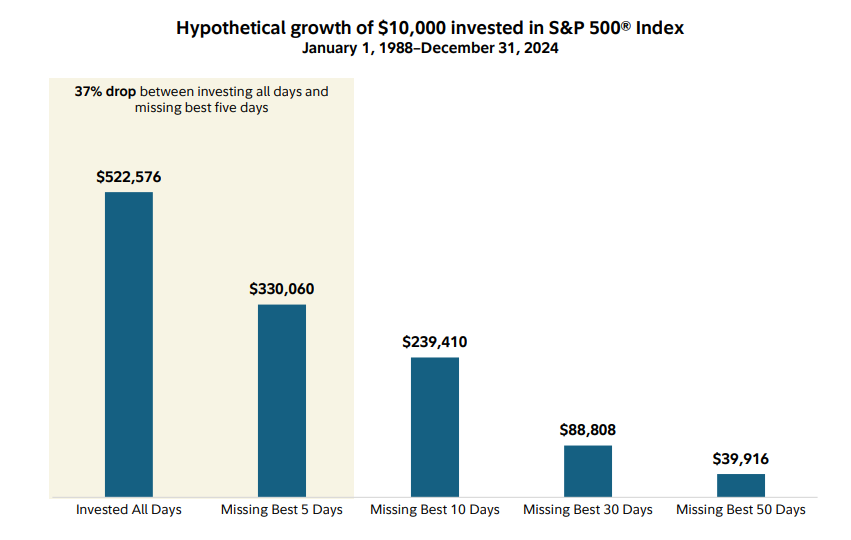

When markets are hitting new highs, it’s tempting to think a correction is just around the corner. But timing the market is notoriously difficult, even for professionals.

If you’re worried about investing a lump sum right now, consider easing in with dollar-cost averaging—investing a set amount at regular intervals. While research shows lump-sum investing often leads to higher returns over time, dollar-cost averaging can help reduce the stress of picking the right time. It's important to understand, though, that periodic investment plans—like dollar-cost averaging—do not guarantee a profit or protect against loss in a declining market.

The bigger risk can often be staying on the sidelines too long. Missing just a handful of the market’s best days can significantly reduce long-term returns. So rather than waiting for the perfect entry point, focusing on getting invested and staying invested with a strategy you can stick to can be a winning formula—even when things feel unpredictable.

Myth #2: It's safer to keep money in a savings account

Many people believe cash is safe. But having too much of your money in cash or a low-yielding savings account can mean your purchasing power shrinks due to inflation. Prices on things like housing, food, and education tend to go up over time. If you have $100 today, it may buy less in 5 years than it does now. By investing in assets that offer the potential to earn a return above the rate of inflation, you have the chance to keep up with price increases.

So the potential boost from investing part of your savings in riskier investments like stocks could help. You don't have to invest it all looking for double- and triple-digit returns—slow and steady may really win the race.

The key is to find a mix of investments, blending stable investments with those that are more risky, that you are comfortable with and could stick with over time.

| Saver | Investor | |

|---|---|---|

| Annual contribution | $15,000 | $15,000 |

| Years contributing | 40 | 40 |

| Average annual rate of return | 2% | 7% |

| Accumulated balance after 40 years | $924,150 | $3,204,144 |

This hypothetical illustration assumes that the saver and the investor each make one annual contribution of $15,000 at the beginning of the year. Taxes and fees are not considered. This example is for illustrative purposes only and does not represent the performance of any security. Consider your current and anticipated investment horizon when making an investment decision, as the illustration may not reflect this. The assumed rate of return used in this example is not guaranteed. Investments that have potential for 7% annual rate of return also come with risk of loss.

Myth #3: Investing in the stock market is too risky

Investors react much more strongly to losses than to gains. The fear that putting money into the stock market could lead to financial ruin keeps many people out of the market and that may keep them from reaching their goals.

The good news is there are things you can do to help manage the amount of risk when investing. For instance, some types of risk can be mitigated with diversification. If all your money was in one stock and the company went out of business, you would have lost your entire investment. But if you own many different stocks, one company likely represents only a small portion of your portfolio. Similarly, you can allocate your assets across different types of investments, like bonds and short-term investments, which can also reduce the amount of risk in your asset mix.

When it comes to investments, stock picking is not necessary—or even encouraged. Investing through mutual funds or exchange-traded funds (ETFs) lets you invest in many companies at once—with professional management and diversification. Keep in mind that diversification and asset allocation do not ensure a profit or guarantee against loss. That's why it's important to build a mix of investments that you can live with—with the potential to hit your goals.

To find out more, read Viewpoints on Fidelity.com: The guide to diversification

The amount of time you plan to allow your investments to stay in the market makes a difference too. With a very long time in the market, history suggests that your chance of permanently losing money in a diversified mix of investments goes down. That's because stocks have tended to rise over time. And as long as you don't sell your investments, they may recover from market downturns.

Myth #4: Investing is too complicated and time consuming

Investing can be really complicated. But it's only as complicated as you want to make it. You can build and maintain a diversified investment mix made up of mutual funds or ETFs—or for many investors it may be easier to turn to a target date fund for retirement goals or an asset allocation fund to handle the investment decisions.

Both types of funds offer a professionally managed, diversified mix of investments based on your goals and financial situation, but target date funds gradually shift to a more conservative mix over time. Asset allocation funds maintain a consistent level of stock investments.

To learn more, read: Diversification through a single fund

Managed accounts are another way to get professional investment management. Some types of managed accounts offer ongoing advice to help you stay on track with your finances.

Robo advisors are a type of managed account. While they offer digital advice and services, they often also provide a full suite of online planning tools. The benefit is lower-cost, hands-off investing compared with traditional investment advisory services.

Myth #5: You need a lot of money to start investing

This used to be true. Back when it cost $50 to place a trade and you had to call a stockbroker, investing was out of reach for many people.

But these days, competition has driven the cost to invest way down. Investment minimums are nonexistent for many mutual funds, and ETFs offer another way to invest with no minimum fees. At many financial institutions, it's possible to start investing with just a few dollars—even with professional investment management if you choose a robo advisor like Fidelity Go®.2

Myth #6: Investment advisors are just trying to sell products

Some people feel comfortable managing their investments, others are happy to choose diversified, professionally managed funds, while another group may prefer the services offered by financial professionals. But many people don't know who they can trust in the financial services world, and that could keep them from investing.

The good news is that there are several different models for the way financial professionals are paid and the services they provide. Some are paid a commission when they sell certain products or do trades, others may charge an hourly fee or a flat fee, while still others charge a percentage of the money you invest with them. There are even more ways they can be paid as well.

There isn't one model that is best for everyone and their financial situation. The Securities and Exchange Commission (SEC) has a thorough series on how to evaluate investment professionals and questions to ask.

The important thing to understand is that you can and should ask how they are compensated, how much you pay directly, and what it means for their recommendations to you.

The bottom line

Investing is accessible for everyone and it can help you reach your financial goals. When investing, you don't have to have tons of money, trade a lot, or employ sophisticated strategies. Just doing the "boring" thing of determining an appropriate asset mix, owning well-diversified and professionally managed investments, rebalancing your portfolio, avoiding the tendency to "tinker," and sticking with that asset mix over time may help you reach your goals. Whether that's through a managed account, a target date fund, or your own hand-picked mix of mutual funds, using this tried-and-true approach has the potential to lead to excellent results.

Your investments are an important component of your overall plan to achieve your goals. You can use Fidelity's Planning & Guidance Center for guidance on retirement and other goals or work with a financial professional to see how your investments fit into your overall planning.