What would you do if you had a reliable source of income besides what you earn from your job? Maybe you would consider making changes to your life and career by exploring a new direction, rediscovering a postponed passion project, starting your own business, or even transitioning into a retirement life that you may not have thought possible.

The good news: There is a strategy you can use that seeks to generate reliable additional income with relatively low risk. How? By building a ladder of bonds or certificates of deposit (CDs) that can provide you with additional income that can act as a bridge to the next chapter of your life.

Bonds and CDs offer a stream of income, and when they mature, they return their principal or face value. Now may be a particularly good time to consider building a bond or CD ladder because interest rates and bond yields are still relatively high compared with the ultra-low levels where they had been for most of the past 2 decades. While many investors may still need some allocation to stocks in order to provide long-term growth and inflation-hedging potential, bonds may be particularly suitable for building an income stream due to the predictability of the timing and amounts of their payments.

Although the prices of the bonds and CDs will move up or down, their coupon payments and repayments of principal are fixed and scheduled for specific dates in the future. The key risk to be aware of is the risk of default, which could jeopardize those future income flows. CDs are FDIC-insured up to applicable limits, and with bonds, you can minimize the risk of a bond defaulting by selecting high-quality bonds and diversifying across different issuers.

How do bond and CD ladders work?

To create a predictable income stream that serves as a short-term bridge, you could buy a series of bonds or CDs with maturity dates that extend into the future and span the period of the bridge. The bonds or CDs pay a fixed income from their coupons and return principal as each bond matures. By holding the bonds to maturity, you can receive the full income from the coupons and maturing principal during the years you want to supplement your cash flow.

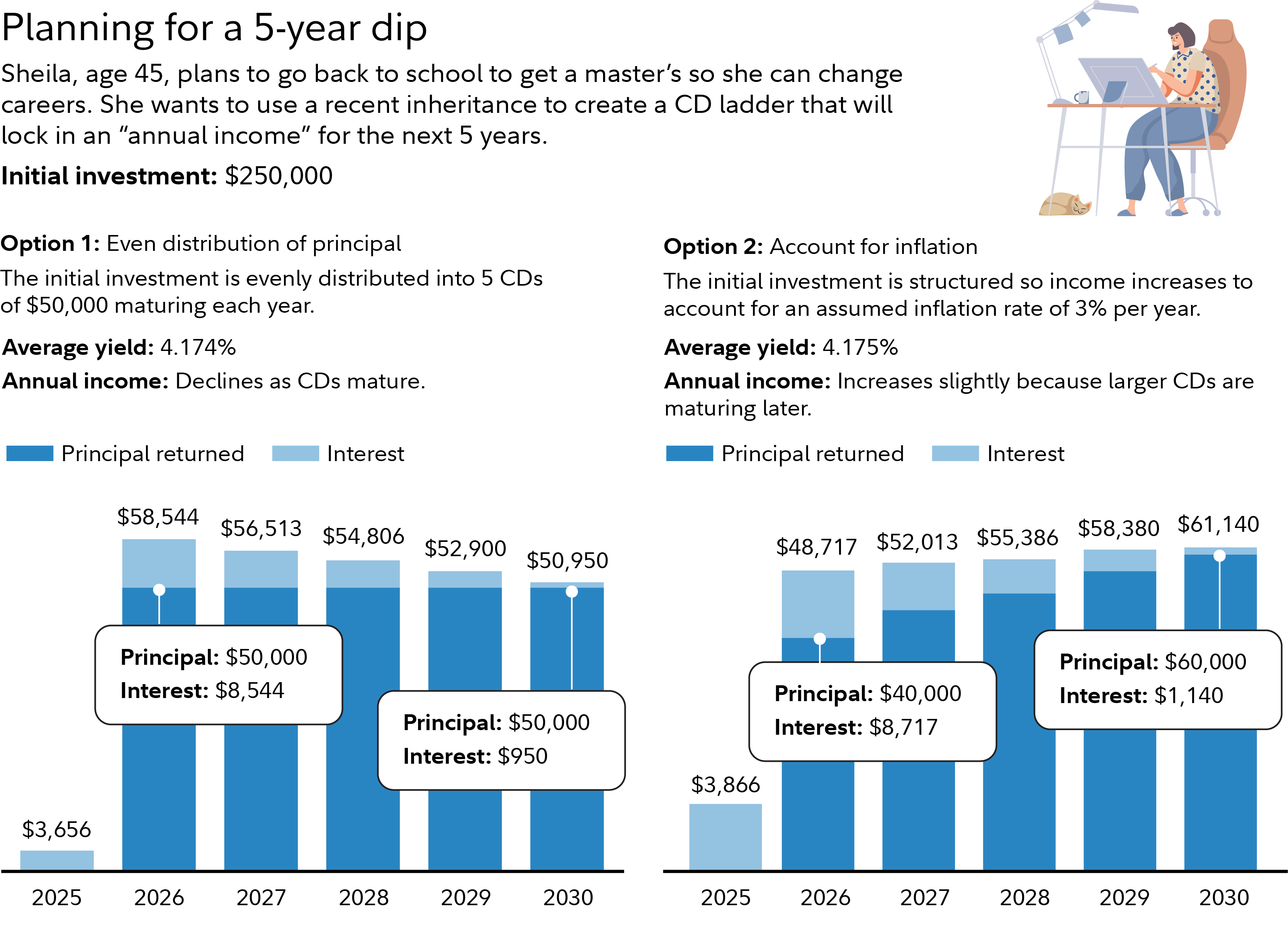

This hypothetical example shows how building a ladder of CDs can help make a mid-life career change easier by providing supplemental income that could be used for living expenses or to pay for tuition.

Because Sheila expects that her income in her new career will eventually be comparable to what she makes in her current job, she is only looking to build a bridge for the next 5 years. However, a bridge built with longer-maturity bonds may be helpful if you are looking to transition from a higher income job to a new career that does not pay as well, or even to having no job at all.

Knowing what to expect from your investment portfolio can help reduce stress as you work through personal or career transitions. It can provide the bridge income you need to retire earlier or to change jobs or careers, perhaps to work where you’ll earn less but be more fulfilled—or just to take a personal break and play more pickleball. An income bridge can give you the financial certainty you may need to make better decisions about the life challenges and opportunities you may face.

Of course, if you’re investing in bonds and CDs for income to live on, you are foregoing the potential higher returns that stocks can offer with that portion of your portfolio. You are also spending down some of your principal. But during certain times of our lives, the tradeoff of potential growth for a higher degree of certainty may be just what you need.

How to build a bond or CD ladder

If you believe that a ladder of bonds or CDs might be what you need, Fidelity can help you. Fidelity offers more than 150,000 individual bonds from various issuers, and our specialists in fixed income can work with you to choose the ones that meets your needs. You can reach them at 800-544-5372.

You can also build a bond ladder or cd ladder yourself if you believe you have the time, skill, and will to select and manage the bonds or CDs in your ladder. You can see current CD interest rates and research individual bonds with the fixed income tools and services available on Fidelity.com. To learn more about whether trying it yourself is for you, read our bond ladder strategy article.