After the summer slowdown, fall can feel like the season to get your life back in order. Feel good about your finances with this financial checklist designed to help you save on everyday expenses, prep for the holidays, and get your money on track before the end of the year.

1. Review recurring expenses

Maybe you paused some services while you spent more time away from your place this summer. Now that you're back, consider whether it's worth it to resume or not and take a magnifying glass to your spending. First, grab a recent credit card statement and highlight recurring charges. (Psst ... Fidelity's budgeting dashboard could do this for you.) Note which services you're still using and cancel the rest. Tally up the money you saved, and then create an automatic monthly transfer for that amount to a savings account. You could also use the extra cash to set up a recurring investment. While you're at it, here are 10 ways to cut expenses by 10%.

2. Hit the farmers' market for fall produce ...

You may associate farmers' markets with spring and summer, but you could save in the fall too. Look for bulk discounts or end-of-day specials on in-season produce, such as apples, squash, or carrots. You might also pay less for "ugly" fruits or vegetables that are bruised or misshapen. Picking your own produce at a "U-Pick" farm could also save you on cost per pound. Get more smart money ways to cut your grocery bill.

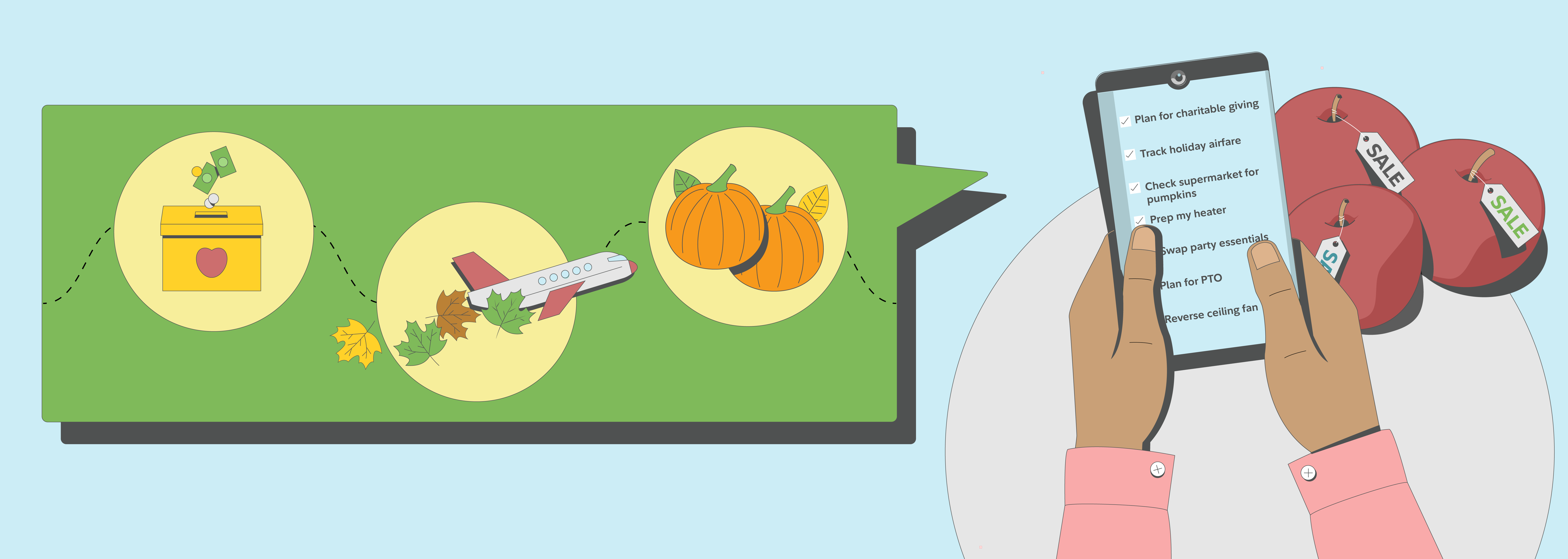

3. … but head to the supermarket for pumpkins

You might get a better deal on a future jack-o-lantern if you skip the pumpkin patch and buy one at a grocery store instead. Why? The patch price might be marked up to help defray costs of the "experience"—aka hayrides, the corn maze, and other fall fun.

4. Pay quarterly taxes

If you don't have an employer withholding taxes on your behalf (because you're a freelancer, side hustler, self-employed, or have substantial investment income) the quarterly deadline to pay taxes is September 15, 2025, for the June 1 to August 31 income period. You may need to make these quarterly estimated payments if you expect to owe more than $1,000 when you file your tax return or if you owed taxes last year.

5. Prep your heater

Furnaces have filters that keep dirt and dust out of your home's airflow. Clogged filters not only make your house dustier but also make running your appliances more expensive. Change your furnace filters every 60 to 90 days so everything chugs along as efficiently as possible. Here are 6 more ways to lower your utility bill.

6. Save on fall party essentials

Need something you'll only use once? Before buying a Halloween costume, fall party décor, or tailgate necessities, check local social media groups to find out if there are any swaps going on. That's when neighbors come together (IRL or within the comments on a social media site) to donate new or used items and pick up a new-to-them one for free or cheap. Check resale sites too for scary good deals.

7. Track holiday airfare

For the cheapest tickets plan to book Thanksgiving trips in early to mid-October and Christmas flights by Halloween. If you can, traveling on the holiday itself could save you even more. Try these other hacks to score the best airfare deals.

8. Get ahead of gifting

There are only a few more paychecks until the winter holidays. And 'tis the season for overspending: Last year, 36% of Americans took on holiday debt, a LendingTree survey found.1 So make your gift list now when there's plenty of time to check it twice (and score free shipping because you aren't opting for rushed delivery). Then, figure out how much you can spend per paycheck to stay on budget. Also, consider tallying up what you’ll need for holiday tips and set aside (or start saving up) that money. Not sure how much to give? See our tipping guide.

9. Prep for open enrollment

If you get health insurance through your company, find out when open enrollment is this year. If you plan to buy insurance on HealthCare.gov, open enrollment starts on November 1. If you're a first-timer, learn how to pick a health plan. If you've had coverage before, revisit last year's plan. Didn't meet your deductible? Spent a ton out of pocket? Check if another plan could better fit your needs. (Just make sure your doctors are still in-network and you wouldn't lose coverage for, say, prescriptions.) If your benefits include access to a health savings account (HSA), learn how one could make your health care more affordable.

10. Plan for PTO

Unlike elementary school, there's probably no perfect attendance award at your job. So figure out how to use all your vacation days now before the year ends. PTO is part of your total compensation package. Multiply your hourly rate by the number of hours your employer offers in yearly PTO. Saying "no thanks" to time off means leaving that money on the table. Going out of town? Here are 10 cheap vacation ideas that still feel fancy.

11. Reverse your ceiling fan

Cooler autumn temps call for a ceiling fan check. Make sure yours is spinning clockwise—that motion makes the blades pull warm air down from the ceiling. And that may save you on heat use and costs. If the air isn't going your way, there's typically a switch to flip near the fan's motor. Then remember to set your fan to spin counterclockwise in the summer to push cool air to you.

12. Make it a holiday potluck

Hosting a food-focused holiday such as Thanksgiving can get pricey with turkey, sides, pies, and cocktails. Try crowdsourcing the meal instead. You handle the turkey—they often get discounted just before Thanksgiving. Then ask guests to each bring a specific type of dish, so you don't end up with 3 bowls of mashed potatoes. Tell everyone to bring their own containers too for divvying up leftovers. Get 8 holiday party ideas for hosts on a budget.

13. Book medical appointments and spend FSA money

Consider making health checkups now and going before the end of the year. That way, if you've met your insurance plan's deductible, you can pay less for services before the January reset. If your FSA has money left, spend it on eligible expenses, then submit those receipts and get reimbursed before the December 31, 2025 deadline.

14. Check on 401(k) contributions

Log in to your retirement accounts and gauge how you're doing. Fidelity's guideline is to save 15% of your pre-tax income toward retirement savings, including any employer match, toward retirement savings. If you're not there yet, try to inch up your contributions by 1% whenever you get a raise, bonus, or other windfall. If you can, consider contributing at least enough to your 401(k) to get any match your employer may offer.

Looking to max out your accounts? Individual contribution limits went up in 2025 to $23,500 for 401(k)s and $7,000 for IRAs for those under age 50 and $8,000 for those age 50 and older.

15. Plan for charitable giving

Consider what impact you want to make this year—and budget for it now. These tips could help you supercharge your giving. If you plan on donating money, you could lower your tax bill for this calendar year if you contribute to an eligible organization before December 31, 2025. (Do a quick search here before donating.) Also, check if your workplace matches donations, which could make your gift go even further.