Many investors interested in fixed-income investing usually think of bonds and bond funds. However, brokered certificates of deposit, or CDs, can play a number of different important roles in any portfolio. Because brokered CDs pay a fixed rate of interest over a predefined term, they can be a good way to lock in a certain rate of return, particularly if you believe that interest rates may soon fall. Because brokered CDs return their principal and are FDIC-insured (up to the applicable limits), they also represent one of the safer places to keep your money while you're considering your investment options. Shorter-term brokered CDs can also be a smart way to protect a portion of your money you may need in the near future, such as money you’ve put aside as an emergency savings.

What is a brokered CD?

When it comes to certificates of deposit, people tend to think of the CDs sold at their local bank. However, Fidelity offers investors a different type of CD, called a brokered CD. These offer many of the same features of a traditional CD—such as fixed rates of return and FDIC insurance—while providing some distinct advantages.

Brokered CDs are issued by banks for the customers of brokerage firms. The brokered CDs are usually issued in large denominations and the brokerage firm divides them into smaller denominations for resale to its customers. Because the deposits are obligations of the issuing bank, and not the brokerage firm, FDIC insurance applies.

Brokered CDs can be traded on the secondary market and thus are generally more liquid than bank CDs. Although a brokered CD will return an investor's principal at maturity, its value if sold prior to maturity will fluctuate based on size, time remaining before maturity, and the current interest rate environment. A brokered CD is also portable and can be transferred from one brokerage firm to another, allowing the owner to consolidate assets at one firm.

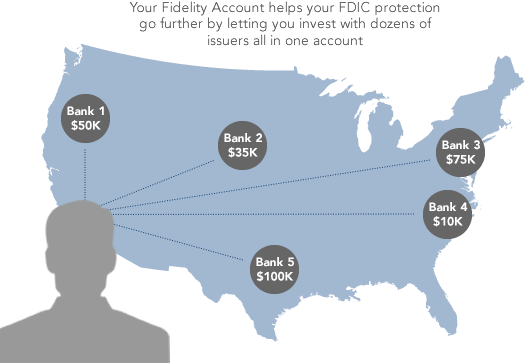

Another advantage of brokered CDs is the ability to expand your FDIC coverage beyond the typical $250,000 per account owner. While banks themselves do not have the ability to exceed FDIC-insurance limits, Fidelity offers many brokered CDs from hundreds of different banks, each of which provides for FDIC protection up to current FDIC limits. By combining a number of CDs issued by different banks in your Fidelity account, you’re able to expand your protection.

While the ability to sell a brokered CD on the secondary market has its advantages, it also has its risks. The secondary market may be limited, resulting in a low bid for the brokered CD you are selling. The market value of a brokered CD in the secondary market may be influenced by a number of factors including interest rates, provisions such as call or step features, and the credit rating of the issuer. Like all fixed income securities, brokered CD prices are particularly susceptible to fluctuations in interest rates. If interest rates rise, the market price of outstanding brokered CDs will generally decline, creating a potential loss should you decide to sell them in the secondary market. Brokered CDs sold prior to maturity are also subject to a concession.

There are other advantages and risks to brokered CDs. For more, see Certificates of Deposit.