Often it’s the little things in life that can make the biggest difference. That’s true when it comes to saving for retirement. Contributing an additional 1% to a tax-advantaged retirement account like a 401(k), 403(b), or an IRA could potentially enhance your lifestyle in retirement. Whether you choose to make Roth or traditional contributions, the benefits of saving just a little more now can pay off later.

Read Viewpoints on Fidelity.com: Traditional or Roth account? 2 tips to help you choose.

“Saving for retirement may seem like a steep mountain to climb, but the climb doesn’t have to be as steep as it looks,” says Ann Dowd, vice president at Fidelity. “Small steps now can turn into big strides later.”

While 1% is a small percentage of your annual earnings today, after 20 or 30 years it can make a big difference in your account balance when you retire. That’s because the longer you give your money a chance to grow, the better. And it works no matter how old you are—or how far off retirement is.

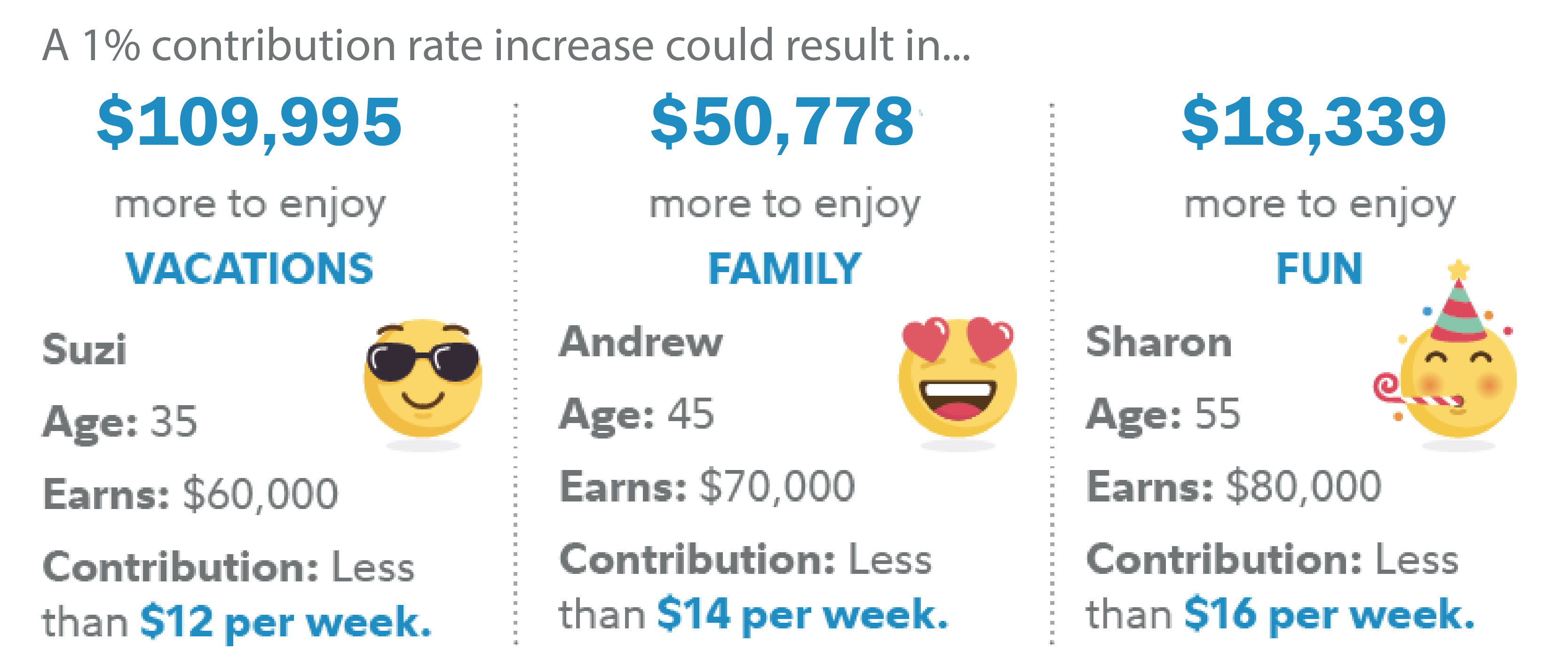

Let’s consider some examples.

Approximations based on a 1% increase in contribution rate. Continued employment from current age to retirement age, 67. Number of years of savings equals retirement age minus current age. Nominal investment growth rate is assumed to be 7%. Hypothetical nominal salary growth rate is assumed to be 4% (2.5% inflation + 1.5% real salary growth rate). All accumulated retirement savings amounts are shown in future (nominal) dollars. This assumes no loans or withdrawals are taken throughout the current age to retirement age.

Your own plan account may earn more or less than this example and income taxes will be due when you withdraw from your account. Investing in this manner does not ensure a profit or guarantee against a loss in declining markets.

Calculate your numbers

Want to create an example like the ones shown above to find out what difference even a 1% increase can make for you? Use our interactive tool. See how a small change can make a BIG DIFFERENCE.

Consider small steps

As shown in our examples—and probably in your own too—small weekly amounts like $12, $14, and $16 can make a noticeable difference in your savings. So how do you find the money? We won’t say to skip buying something if you really need it, but there are probably places in your spending that may be easy to cut. Even bringing your lunch or using coupons could save you $16 or more. And the beauty of 401(k) contributions is that they come right out of your paycheck, so you may not even miss the spending money.

If a one-time bump-up isn’t ideal now, consider aiming to increase contributions each year. For instance, if your 401(k) lets you set automatic increases every year, consider signing up. (Effective 2025, barring an exemption, 401(k) and 403(b) plans established on or after December 29, 2022 are required under SECURE 2.0 to include automatic enrollment and automatic contribution escalation features.) If you usually get a raise each year, you may be able to time the increase to happen when you get a bump in pay so you won’t feel the impact in your paycheck.

Consider saving 15%

We ran the numbers and determined that aiming to save 15% of income toward retirement annually—which includes any matching contributions or profit sharing an employer may make to a workplace retirement account like a 401(k) or 403(b)—can help ensure that you can maintain your lifestyle in retirement. According to Q1 2026 Fidelity data, more Americans are moving closer to this goal: the total 401(k) savings rate—which combines average employer and employee contribution rates—reached a record 14.4%, bolstered by automatic annual contribution increases.1

Read Viewpoints on Fidelity.com: How much should I save for retirement?

Not saving that much? Don’t fret. Few people get there overnight. Think of planning for retirement as a journey. The key is to save as much as you can now and try to increase savings over time. If possible, save at least enough to capture the full amount of any match from your employer. If you're not doing that, you're leaving free money on the table.

“Starting early, saving regularly, and increasing the amount you save as your income increases will help you to achieve the retirement you envision,” says Dowd.

Don’t have a 401(k)?

You may be self-employed or maybe your employer doesn’t offer a 401(k). But you can save in a tax-advantaged account like an IRA. There are several types of IRAs.

The annual contribution limit for IRAs, including Roth and traditional IRAs, is $7,500 for 2026. If you're age 50 or older, you can contribute an additional $1,100 for 2026.

Find out how you’re doing

We made it easy to begin measuring how you are doing when it comes to saving for retirement. Answer 6 simple questions to get The Fidelity Retirement ScoreSM. A retirement score is a tool that can help you understand your financial readiness for retirement. Whatever your score, you can take some simple, clear steps to stay on track or improve it.

Go for it

Challenge yourself to save a little more. Whether it’s a 1%, 3%, or even 5% increase, the extra money saved today could make a big difference in helping achieve the retirement you envision. Think about it this way: Do you want to be worrying about money in retirement?