Roth IRA

Save tax-free with access to your contributions

Once you contribute to your Roth, potential growth within the account is tax-free. Contributions you add to your account may be withdrawn at any time, penalty-free.

We have options to help you with your retirement savings, whether that’s through an IRA or small business account.

We have accounts to match how you'd like to invest for your retirement. And for most retirement accounts, there are no account fees or minimums.1

Once you contribute to your Roth, potential growth within the account is tax-free. Contributions you add to your account may be withdrawn at any time, penalty-free.

Reduce your taxable income by deducting your contributions, if eligible, and your potential earnings may grow tax-deferred.2

If you are looking to move your old 401(k) and workplace accounts into one IRA, you can do so without taxes or penalties.3

An account specifically designed for retirement plan beneficiaries—those who have inherited a traditional IRA or Roth IRA.

This is a way to help your child start saving for retirement. It’s opened on behalf of a child who has earned income and it’s managed by an adult.4

Save, invest, and pay for qualified medical expenses in a tax-advantaged way with a health savings account (HSA). The money is always yours (not use it or lose it) now through retirement.5

Offered by Fidelity Digital Assets®, a Fidelity Crypto® Roth IRA, traditional IRA, or rollover IRA allows you to directly invest in crypto like bitcoin and ethereum within a tax-advantaged retirement account.

Not sure which account makes the most sense for you? We’ve compared the two IRAs to help you make an informed choice.

Traditional IRAs and Roth IRAs offer different benefits—but having both can make sense.

Make sure you aren't overlooking some strategies and potential tax benefits.

Consider putting your money to work by investing for potential growth.

Whether you're looking for investment strategies or a more collaborative and customized approach, we offer a number of ways to work together.

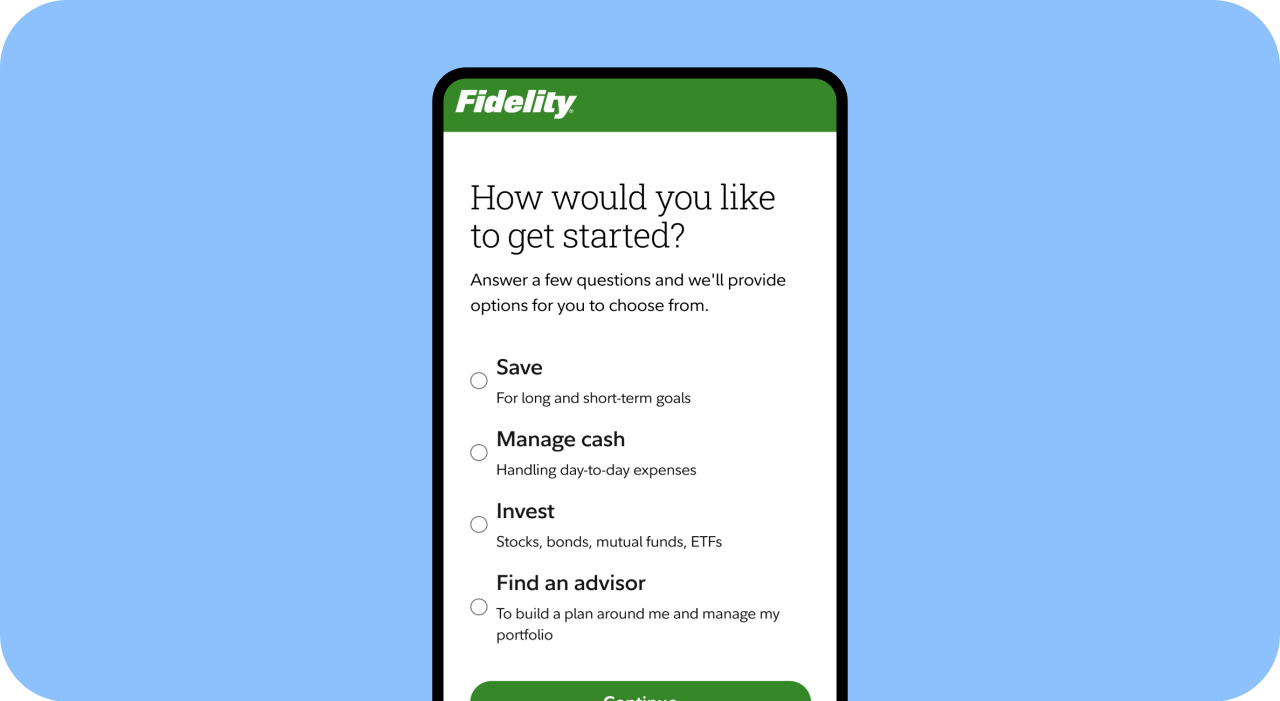

We’ll guide you through some basic questions to help you find accounts that may fit your goals.

We can help you find the answers.

No matter the size of your business, we’ve got options to help support your retirement goals and those of your employees.

A 401(k) plan for self-employed individuals with no employees other than a spouse.

This is an easy-to-maintain plan if you’re a self-employed individual or small-business owner with fewer than 5 employees.6

A low-complexity plan for businesses with fewer than 100 employees that are looking to offer tax-advantaged retirement plans.

A low-cost, simplified 401(k) for businesses with up to 1,000 employees offering a plan for the first time.

This is a brokerage account for those who have their own separate retirement plan document and would like to include offerings from Fidelity.

Need help figuring out which small business account is a good fit for you? Answer a few questions and our tool will help you choose an account.

Know your options to save for long-term goals.

SEP IRAs give small-business owners and the self-employed a powerful retirement savings vehicle.

A solo 401(k) often provides the highest savings potential for self-employed individuals.

Whether you're looking for investment strategies or a more collaborative and customized approach, we offer a number of ways to work together.

We’ll guide you through some basic questions to help you find accounts that may fit your goals.

We can help you find the answers.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Be sure to consider all your available options and the applicable fees and features of each before moving your retirement assets.

Screenshots are for illustrative purposes only.

Fidelity Crypto® for IRAs is offered by Fidelity Digital Assets® Investing involves risk, including risk of total loss. Crypto as an asset class is highly volatile, can become illiquid at any time, and is for investors with a high risk tolerance. Crypto may also be more susceptible to market manipulation than securities. Crypto is not insured by the Federal Deposit Insurance Corporation, the Securities Investor Protection Corporation, or any other government agency, and is not an obligation of any bank. Investors in crypto do not benefit from the same regulatory protections applicable to registered securities. Fidelity Crypto® accounts and custody and trading of crypto in such accounts are provided by Fidelity Digital Assets, National Association, which is a national trust bank. Brokerage services in support of securities trading are provided by Fidelity Brokerage Services LLC (“FBS”), and related custody services are provided by National Financial Services LLC (“NFS”), each a registered broker-dealer and member NYSE and SIPC. Neither FBS nor NFS offer crypto as a direct investment nor provide trading or custody services for such assets. Fidelity Crypto and Fidelity Digital Assets are registered service marks of FMR LLC.

Offerings and account features are subject to account eligibility.

1. No account fees or minimums to open Fidelity retail IRA accounts. Expenses charged by investments (e.g., funds, managed accounts, and certain HSAs), and commissions, interest charges, and other expenses for transactions, may still apply. See Fidelity.com/commissions for further details.

2. A distribution from a Traditional IRA is penalty-free provided certain conditions or circumstances are applicable: age 59 1/2; qualified first-time homebuyer, up to $10,000; birth or adoption expense (up to $5,000); qualified higher education expense; death or disability; health insurance premiums (if you are unemployed); some unreimbursed medical expenses; substantially equal periodic payments; or tax levy.

3. Generally, there are no tax implications if you complete a direct rollover and the assets go directly from your employer-sponsored plan into a Rollover, Traditional or Roth IRA (as applicable) via a trustee-to-trustee transfer.

4. Generally, compensation is what you earn from working. For a summary of what compensation does and does not include, see IRS Publication 590A Table 1-1.

5. With respect to federal taxation only. Contributions, investment earnings, and distributions may or may not be subject to state taxation.

6. Most SEPs require employers to contribute to each employee's plan at the same percentage of their salary/wages. For this reason, SEPs are rarely chosen by those with greater than 5 employees.

7. Investment-only account. This is not a plan but type of account. The account is established by the Trustee. The Plan must be a Trustee-directed pooled account. It cannot be a plan that allows for employee investment direction. Please consult your plan document to see if you qualify to open an account.

Fidelity advisors are licensed with Strategic Advisers LLC (Strategic Advisers), a registered investment adviser, and registered with Fidelity Brokerage Services LLC (FBS), a registered broker-dealer. Whether a Fidelity advisor provides advisory services through Strategic Advisers for a fee or brokerage services through FBS will depend on the products and services you choose.

Fidelity does not provide legal or tax advice. The information herein is general in nature and should not be considered legal or tax advice. Consult an attorney or tax professional regarding your specific situation.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

1223264.2.0