Commitment to execution quality

We work hard to get you a better price for your equity, ETF, and options orders—every time you buy or sell. It's called price improvement, and we saved our investors over $3.2 billion on trades in 2025.3 Along with transparent pricing, it's part of the industry-leading value you can expect from Fidelity.

Unmatched value with Fidelity's price improvement

![]()

Saves you money

Our price improvement1 can save investors $26.69 on average for a 1,000-share equity order.

![]()

Shows your savings

Easily see your savings for an individual order, as well as over multiple time periods, on our pricing summary.

![]()

Shares for industry comparison

How it works

Price improvement occurs when a trade is executed at a better price than the best quote market price or National Best Bid and Offer (NBBO).

Get the full white paper

The benefits of enhanced execution quality for investors

Rated #1 for Order Execution by StockBrokers.com in 2023.

See how the savings can add up

Average price improvement1

For a 1,000-share equity order

Whether you trade a lot or a little, Fidelity's price improvement can help you save.

The proof is in the numbers

| Price improvement

Percentage of shares that are price-improved: |

|

| 95.37%

How it's measured |

| Execution price

Percentage of shares that fall within the NBBO: |

|

| 98.88%

How it's measured |

| Execution speed

Average execution speed: |

|

| 0.03 seconds

How it's measured |

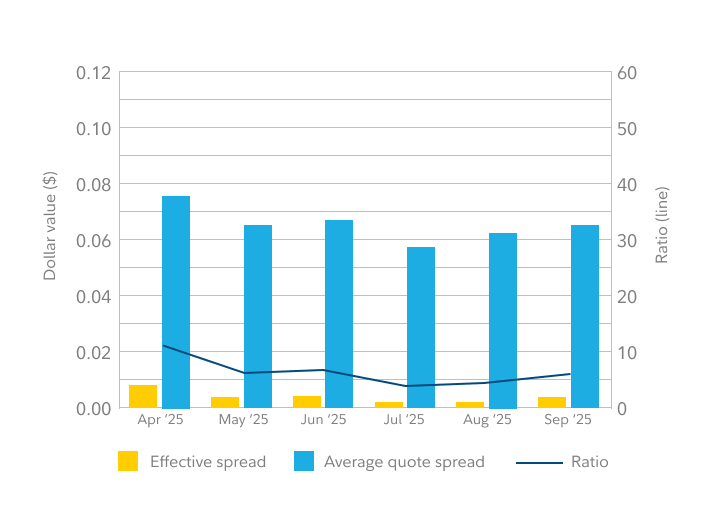

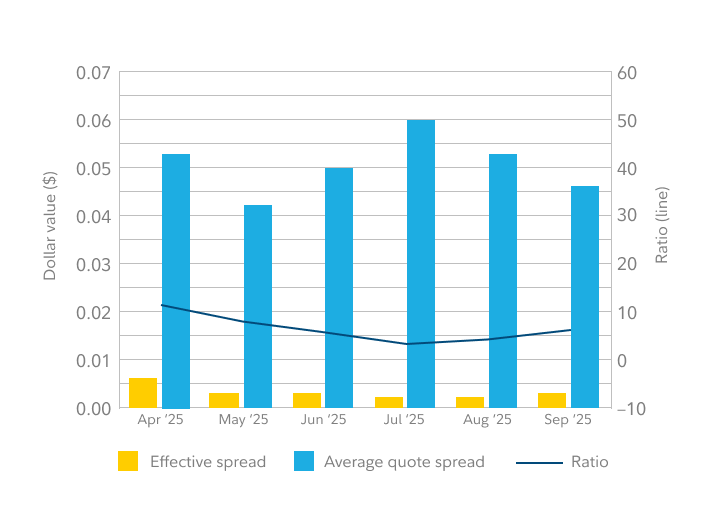

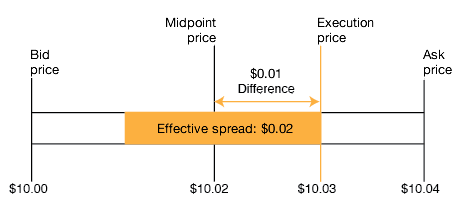

| Effective spread

Average effective spread: |

|

| $0.0056

How it's measured |

Source: Fidelity Q1 2026 statistics.

Applying high standards on every trade

Our Order Flow Management Team ensures that your order goes to the top-performing market centers, seeking the best execution price.