Management effectiveness has many dimensions and without standardized points of reference, it can be difficult to evaluate. These ratios can be used to compare management performance against peers and competitors. They can also be used to benchmark company performance over time and in different economic environments.

Return on assets

Return on assets (ROA) is a financial ratio that shows the percentage of profit a company earns in relation to its overall resources. It is calculated by dividing net income by total assets. Net income is a company's profit after taxes. Total assets include cash and cash-equivalent items such as receivables, inventories, land, equipment (less depreciation), and patents. ROA is a key profitability ratio that measures the amount of profit made by a company per dollar of its assets. Generally, the higher the ROA, the better the management. ROA gives an indication of the capital intensity of the company, which will depend on the industry. That's why when using ROA as a comparative measure, it is best to compare it against a company's previous ROA figures or the ROA of a similar company.

Return on equity

Return on equity (ROE) is an important measure of the profitability of a company. It is the ratio of net income of a business during a year to its stockholders' equity during that year. It is calculated by taking a year's worth of earnings and dividing them by the average shareholder equity for that year. Higher values are generally favorable, meaning that the company is efficient in generating income on new investment. But note that a higher ROE does not necessarily mean better financial performance of the company.

Gross profit margin

Gross profit margin is a profitability ratio that measures how much of every dollar of revenue is left over after paying cost of goods sold. It is calculated by subtracting cost of goods sold from total revenue and dividing that number by total revenue. It is a key measure of profitability by which investors and analysts compare similar companies with each other and companies with their overall industry. The metric is an indication of the financial success and viability of a particular product or service. The higher the percentage, the more the company retains on each dollar of sales to service its other costs and obligations.

Inventory turnover

Inventory turnover is the amount of sales that occur in a period divided by the amount of inventory held in that period. The analysis may use actual sales as reported under revenue, or it may use the cost of goods sold under expenses. The former focuses the analysis on the amount of money: The same physical volume of inventory movement could produce different ratios at different times if the selling prices and market conditions are different. The latter more closely approximates physical movement since costs for inventory are normally not changed once recorded. In addition, inventory turnover analysis may use values fixed at the end of the accounting period, or it may use a period average. Averaging can smooth out seasonal or periodic variations.

Selling, general, and administrative expenses to net sales

Selling, general, and administrative expenses (SG&A) is an essential measure of the efficiency of a sales organization, and it should be viewed in the context of industry and peer group norms as well as the individual company's sales management and production strategy. SG&A expenses such as sales commissions and incentives tend to vary directly with overall sales volume, while expenses such as call centers and customer service tend to be relatively fixed. A company with generally variable costs that shows a sudden change in its SG&A might have changed its management strategy, might have incurred some unusual but significant cost, or might have realized a new efficiency. A company with a high level of fixed SG&A expenses should see its ratio decline as sales increase, and vice versa. A track of ratios calculated at different points in time can help suggest whether costs might be moving into or out of line with sales.

Return on investment

Return on investment (ROI) conceptually is the net amount of money one earns from an investment, expressed as a percentage of the total cost of making that investment. For an individual looking at a single transaction (such as the purchase and sale of a block of stock), ROI could be a straightforward calculation. However, in the context of enterprise accounting, the calculation may involve overlapping uses and returns, so at aggregated levels it is sometimes called return on invested capital (ROIC). ROI (or ROIC) can be used to benchmark the effectiveness of competing management teams and business strategies. It can be used to supplement a performance comparison of two companies: Companies with roughly equal revenues and expenses can have significantly different ROICs, suggesting that the one with the higher ROIC is managed noticeably more efficiently. And it can be used to help evaluate the integrity of revenue and expense forecasts.

Operating margin

Operating margin is the percentage that results when operating profit is divided by sales revenue. Operating profit reflects only that portion of earnings that results from primary business activities. It does not reflect gains or losses on any incidental investment securities or comparable assets that might also be owned by the company, so the total may not always be synchronized with net income. Operating margin can be useful when used to analyze a company's performance and efficiency over time. It is also useful when comparing a company with an industry or competitor peer group. Keep in mind that the absolute levels of operating margin vary widely across industries. Operating margin is one of two measures that can be used to judge the efficiency of a company's sales volume at generating profits. (See also Return on Sales.)

Return on sales

Return on sales is the percentage that results when the reported net income before interest and taxes is divided by sales revenue. It can be useful when used to analyze a company's performance and efficiency over time. It is also useful when comparing a company with an industry or competitor peer group. Absolute levels of return on sales vary widely across industries. A typical level for a supermarket or similar retailing operation might be 5% or less, while some professional services firms might show ratios of 20% or more. Return on sales is one of two measures that can be used to judge the efficiency of a company's sales volume at generating profits. (See also Operating Margin.)

Free cash flow from operations

Free cash flow from operations represents the amount of actual cash that a company takes in over and above the money it needs to cover all of its operating expenses and new capital expenditures. Some analysts calculate this amount by taking cash flow as reported from the company's financial statement, then deducting capital expenditures. Others start with a company's earnings before interest and taxes, then add depreciation and amortization expenses, and then subtract changes in net working capital and capital expenditures. The intent in either case is to create a more concrete, cash-defined picture of company performance than can be produced by the generally accepted accounting principles used in annual reports. Free cash flow analysis minimizes the potential effects of accounting choices about depreciation, the accounting recognition (as opposed to actual collection) of revenue, and other factors.

Current ratio

The current ratio is the company's current assets divided by its current liabilities. Current assets typically include cash, marketable securities (investments such as money market securities that are easily convertible to cash and have a relatively stable value), accounts receivable, and inventory available for sale. Current liabilities generally include all liabilities due for payment within one year. A current ratio greater than one is generally considered a sign of fiscal strength, while a value of less than one is sometimes considered a signal that a company may not be able to meet its bills. Keep in mind that a business with a particularly rapid inventory turnover may be less hampered by lack of current cash resources than one with a long cycle from initial sales discussion to receipt of cash.

Quick ratio

The quick ratio (also known as the "acid-test" ratio) is the sum of its cash on hand, marketable securities, and accounts receivable divided by its current liabilities. A ratio of one or more suggests that a company will be able to meet all of its liabilities with resources that it has on hand; the greater the number, the thicker the liquidity cushion that the company has. A ratio of less than one, on the other hand, signals a company that may not be able to pay its bills as they come due without liquidating inventory or assets. (Keep in mind that while industries such as retailing might generate cash quickly through immediate inventory sales, others have sales cycles that may stretch out over months, making stressed sales to raise cash less efficient.)

Net income per employee

Net income per employee is seen as an ultimate measure of a company's efficiency; specifically, it shows how much net profit can be attributed on average to each individual on the payroll. For any single company, the net income per employee can provide a meaningful yardstick for monitoring management effectiveness and judging strategic decision making. In theory, a stable and appropriately constructed workforce should become more proficient over time as it climbs the collective learning curve and thus becomes more profit-producing. This metric can also be used to compare a company with others in its peer group, but keep in mind that norms vary widely from industry to industry. An industry where employees might be leveraged by large capital investments, such as refining, should have a different profile than one that is labor intensive, such as food service.

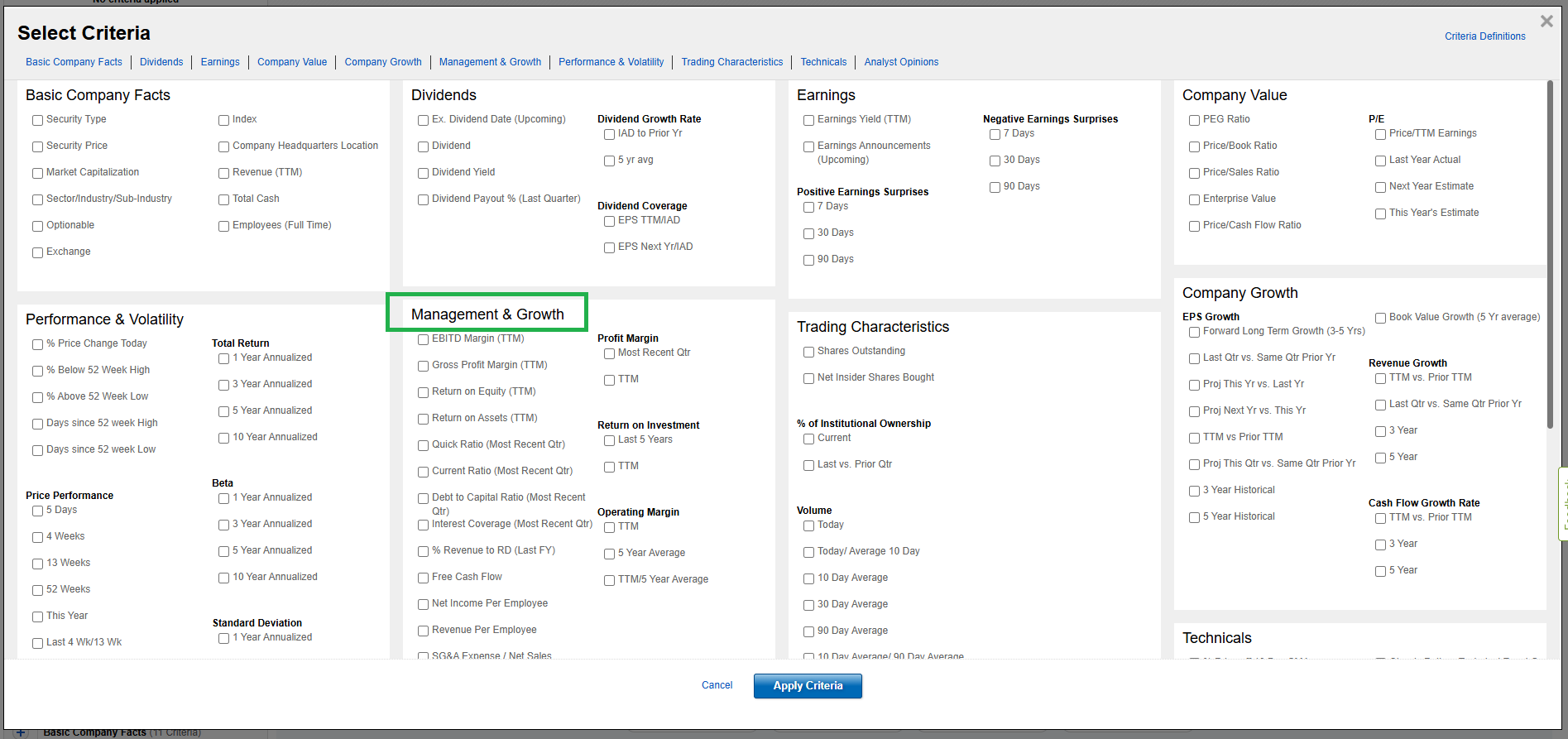

You can screen by the Management and Growth criteria discussed in this lesson when using the Fidelity.com Stock Screener.