If you think federally tax-free retirement income seems like something that's too good to be true, you might want to learn about Roth IRAs. With a Roth IRA, you contribute after-tax dollars, your investments can potentially grow tax-free, and you can withdraw any earnings tax-free and penalty-free when you reach age 59½ and the account has been funded at least 5 years from the beginning of the tax year of your first contribution.1

Here's what you need to know about what Roth IRAs are, how they work, what benefits they can offer, and how to open one if you qualify.

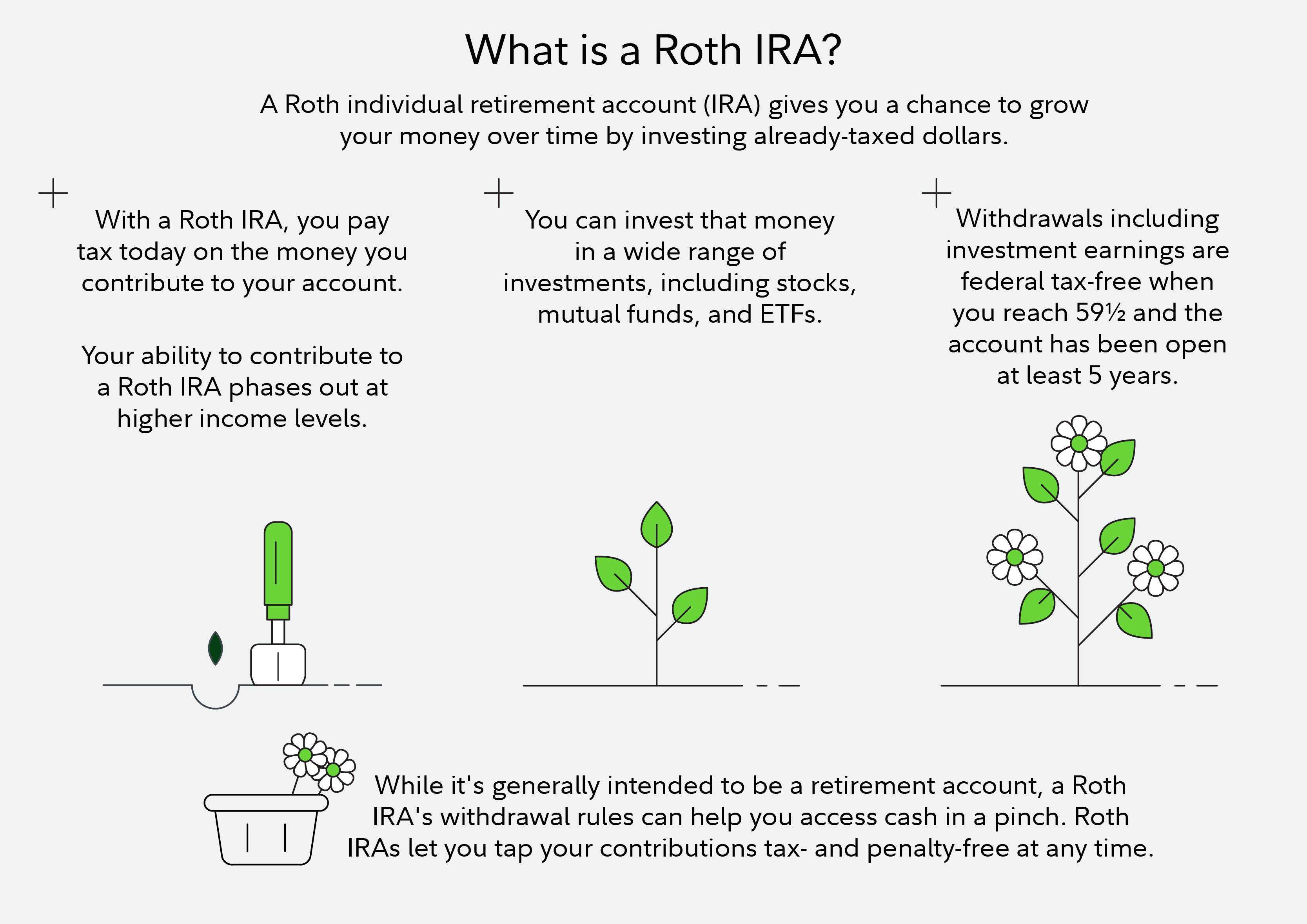

What is a Roth IRA?

A Roth IRA is an account that gives you a chance to grow your money over time by investing already-taxed dollars in a range of different securities—from stocks and bonds, to mutual funds, to exchange-traded funds (ETFs). The exact investment mix available will depend on your investing style and preference and what investment options are available through the financial institution where you opened the Roth IRA.

How does a Roth IRA work?

The tax-free retirement income from a Roth IRA comes with a few strings attached. Before you invest, you'll need to know about 3 main topics: contribution limits, income limits, and withdrawal rules.

Roth IRA contribution limits

The annual contribution limit for IRAs, including Roth and traditional IRAs, is $7,500 for 2026. If you're age 50 or older, you can contribute an additional $1,100 for 2026.

Roth IRA income limits

Your ability to contribute to a Roth IRA depends both on having earned income and your overall amount of income, as shown by your modified adjusted gross income, or MAGI. MAGI is your adjusted gross income from you annual tax return (aka your total income minus tax credits, adjustments, and deductions), with some of those credits, adjustments, and deductions added back in. Your MAGI and tax-filing status work together to determine whether you can make a full, partial, or no contribution to a Roth IRA for the tax year.

You can open and contribute to your Roth IRA as long as you have a taxable income under the yearly IRS limits.

For 2026, you can make full contributions to your Roth IRA if your modified adjusted gross income (MAGI) is less than $153,000 for a single adult, partial contributions for MAGI between $153,000 and $168,000 and no contributions with a MAGI $168,000 or higher.

Married couples filing jointly for 2026 can make the maximum contribution if their MAGI is less than $242,000. They can make partial contributions if their 2026 MAGI is more than $242,000 but less than $252,000. Married couples filing jointly whose 2026 MAGI is $252,000 or higher can't contribute directly to a Roth IRA.

These annual MAGI limits only apply to new contributions to a Roth IRA. So if you opened a Roth IRA in the past, you can keep the account open and still invest the balance. You just won't be able to make any additional contributions in years when your MAGI exceeds the IRS limits.

Another important thing to keep in mind: IRA contribution limits apply across all IRA types, so if you have both a traditional and Roth IRA, you can only contribute up to the annual maximum across both accounts each year, not the annual maximum in each. Which means if your income limits you to a partial Roth IRA contribution, you could make up the difference using a traditional IRA up to the total IRA contribution limit for the year. Note: Spouses have independent contribution limits, and a non-working spouse can leverage the earned income from a working spouse to contribute.

What if I earn too much?

If you earn too much to save using a Roth IRA, you could have other ways to access the same tax-free growth potential. For instance, if your employer offers a Roth 401(k) option or you're self-employed and have a self-employed Roth 401(k), you can get all the benefits of a Roth IRA without the income restrictions. Or you could use a strategy called a backdoor Roth IRA, a technique that lets high earners convert nondeductible contributions made to a traditional IRA into a Roth IRA.Roth IRA withdrawal rules

Since you contribute after-tax money to a Roth IRA, you can withdraw your contributions at any time without taxes or penalties, even before retirement. For your investment gains, however, it's a different story.

With the Roth IRA 5-year rule for withdrawals, at least 5 years must elapse between the beginning of the tax year of your first contribution to a Roth account and the time when you withdraw earnings, even if you are 59½ or older. If fewer than 5 years have passed before you make a withdrawal of earnings, the withdrawal is considered a nonqualified distribution and may be subject to either taxes or penalties (or both).

Some exceptions to the 5-year rule may apply, allowing you to make withdrawals penalty-free (but not tax-free). These include withdrawals up to $10,000 made for a qualified first home purchase, for permanent and total disability, or for qualified educational expenses.

Roth IRA versus traditional IRA

The type of IRA you use to save for retirement often comes down to a question of whether you want to benefit from a tax break now (traditional IRAs) or later (Roth IRAs). To help you decide which one fits your retirement savings goals and tax situation, here are some of the benefits a Roth IRA can offer that may help you achieve those goals.

Tax-free retirement income

If your current income sets you up to be taxed at a lower rate than you expect you'll pay in retirement, or you simply value the certainty of knowing what you'll owe the government, it may make sense to lock in tax-free future qualified withdrawals now with a Roth IRA. While you won't get to deduct your contributions from your taxes today, like you would with a traditional IRA, you're eliminating the risk you have to pay more later on your contributions—plus any amount they've grown.

Flexible withdrawal rules

While it's generally intended to be a retirement account, a Roth IRA's withdrawal rules can help you access cash in a pinch. You're subject to taxes and penalties on traditional IRA withdrawals before age 59½. But Roth IRAs let you tap your contributions tax- and penalty-free at any time.

With traditional IRAs and other retirement accounts, the government forces you to begin withdrawals after you reach age 73—whether you need the money or not—through a mechanism called required minimum distributions (RMDs). If you don't take out the required amount, you could face a tax penalty. But Roth IRAs aren't subject to RMDs—provided you're the original account owner and not an inheritor—which means you can stay invested as long as you'd like and continue to potentially grow your savings.

Create a legacy

If you want to leave your retirement savings behind, Roth IRAs offer a powerful way to transfer wealth income tax-free. For instance, spousal beneficiaries receive the same beneficial tax treatment—tax-free growth and withdrawals—as the original account owner, as long as the Roth IRA is at least 5 years old when the spouse beneficiary begins withdrawals. Most non-spouse recipients will have to liquidate the account within 10 years and can also benefit from tax-free earnings and withdrawals as long as the Roth IRA is at least 5 years old when beginning withdrawals.

How to open a Roth IRA

If you're ready to start saving for retirement with a Roth account, opening a Roth IRA only takes a few simple steps.

1. Choose a broker-dealer or investment company

You can compare fees and available securities at a wide range of broker-dealers or financial institutions offering Roth IRAs. Many brokerage firms or financial institutions even offer the option to open a Roth IRA online.

2. Fund your Roth IRA

Funding your Roth IRA starts with contributing to it. But before contributing, it's important to ensure that you're eligible. Although the most common way to fund a Roth IRA is by contributing cash from your bank account, wire transfer, or ACH as an eligible yearly contribution, there are also ways to contribute via rollovers from other retirement accounts. These contributions may be treated as a conversion that is generally subject to immediate taxation. Financial maneuvers like these can be complicated, and it's best to consult a financial or tax professional if considering.

3. Invest the money

Once the funds in your new Roth IRA are available, you can invest the money into any securities available at your broker-dealer or investment company. But remember: you don't have to go it alone. From online guides that can help you pick investments and free online financial planning tools to working with a financial professional, there's help on hand to empower you each step of the way.