Most children, whether they are teenagers or younger, don't spend a lot of time worrying about retirement. After all, when you're juggling schoolwork, extracurricular activities, and all the other challenges of adolescence, saving for retirement may not even register on your radar screen.

However, that doesn't mean that savvy parents, grandparents, and other family members can't step in to help jumpstart their children's retirement savings. One way to do that is to establish a custodial account Roth IRA, or what is known at Fidelity as a Roth IRA for Kids, and more generally as a Roth IRA for minors.

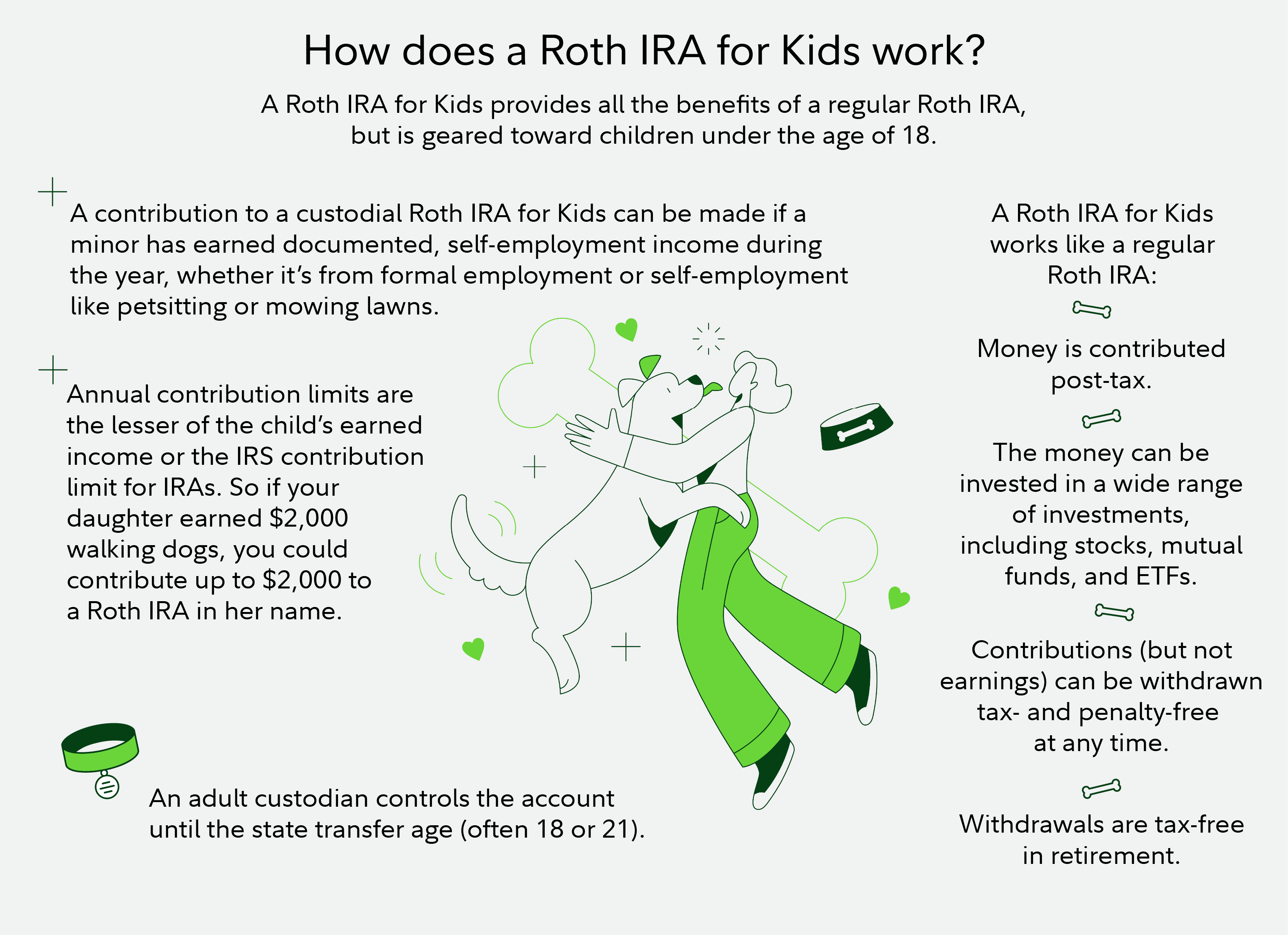

A Roth IRA for Kids provides all the benefits of a regular Roth IRA, but is geared toward children under the age of 18 and requires an adult to serve as custodian.

The custodian maintains control of the child's Roth IRA, including decisions about contributions, investments, and distributions. In addition, statements are sent to the custodian. However, the minor remains the beneficial account owner and the funds in the account must be used for the benefit of the minor. When the minor reaches a certain required age, typically either 18 or 21 in most states, the assets must be transferred to a new account in their name.

Put your child's earnings to work

A contribution to a custodial Roth IRA for Kids can be made if a minor has earned income during the year. Eligible income can include formal employment income or self-employment income. Activities like babysitting, petsitting, or mowing lawns can qualify a minor for Roth IRA contributions. Note that in some cases, self-employment taxes (Medicare and Social Security) may apply, so it's advisable to consult with a tax professional. The 2026 maximum annual contribution is $7,500, or the total of a child’s earned income for the year—whichever is less. For example, if your daughter earned $2,000 during a summer job, you could help her by contributing up to $2,000 to a Roth IRA in her name. (Keep in mind, an adult cannot contribute more than the minor's earned income, so if the adult contributes $2,000, neither the minor nor another adult can contribute more that tax year.)

For a distribution to be considered qualified, the 5-year aging requirement has to be satisfied, and you must be age 59½ or older or meet one of several exemptions (disability, qualified first-time home purchase, or death among them).

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Fidelity does not provide legal or tax advice. The information herein is general in nature and should not be considered legal or tax advice. Consult an attorney or tax professional regarding your specific situation.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

1131600.3.0

If your child is not filing a tax form that reports his or her earned income, consider maintaining a written log of their earnings in case the IRS asks questions. Unlike traditional IRAs, contributions to Roth IRAs are made with after-tax dollars. This means your child cannot claim a tax deduction for contributions to his or her Roth IRA. However, since most kids have low annual earnings, their income tax rate is already quite low or even zero. Therefore, tax deductions may not be an important factor at this stage of their lives. Moreover, when it comes time to tap their savings at retirement age, certain qualified distributions from a Roth IRA will be tax-free, unlike distributions from a traditional IRA.

Making the case to the children in your life

Despite the potential to accumulate significant savings, tying up money in a Roth IRA may not appeal to a child who is more concerned about having cash to go to the movies or to buy video games. For older teens, concerns about paying for a car or pending college tuition bills may take priority.

Convincing a child to hand over his or her hard-earned cash to invest in a Roth IRA may be challenging, but remember that as long as the child has earned income to qualify for Roth IRA contributions, it doesn’t matter where the contributions come from. There are several possible approaches to funding the account: for example, you or another adult could make contributions as gifts to reward the child for working, or the child could contribute a portion of his or her earnings to the Roth IRA and you match that amount (assuming the total contributions—both the child's contribution and any of your own contribution on behalf of the child—don't exceed the lesser of the child's earned income for the year or the 2026 IRA contribution limit of $7,500). You may need to file a gift tax return (Form 709) if you simultaneously gave that child additional cash or assets outside the IRA that pushed the combined total past $18,000 for the year.

It's also helpful to know that with a Roth IRA, the rules do provide some flexibility to withdraw funds prior to retirement. For example, a Roth IRA allows the account owner to take out 100% of contributions at any time and for any reason, with no taxes or penalties. Generally, any withdrawals are considered to come from contributions first. Distributions from earnings—which may be taxable if certain conditions are not met—begin only when all contributions have been withdrawn.

Earnings from the investments in the account can be taken out without paying any federal taxes (and usually state and local taxes too) after the account owner reaches age 59½. The account owner must have had a Roth IRA open for at least 5 years, measured from the beginning of the first tax year a contribution was made to a Roth IRA. This is known as the 5-year rule.

If the account owner takes withdrawals of earnings prior to age 59½ and does not satisfy the 5-year rule, they will (unless an exception applies) be subject to a 10% early withdrawal penalty and ordinary income taxes. Exemptions to the 10% early withdrawal penalty and ordinary income taxes may apply.

Establishing a Roth IRA for Kids allows the children in your life to begin taking advantage of the opportunity for tax-free growth at a young age. While your children may not be overly excited about this idea now, they may thank you many years from now.