People often talk about interest rates as though all rates behave in the same way. The reality, however, is much more complex, with rates on various bonds often behaving quite differently from one another, depending on their maturity. A yield curve is a way to easily visualize this difference; it's a graphical representation of the yields available for bonds of equal credit quality and different maturity dates.

A yield curve is a way to measure bond investors' feelings about risk, and can have a tremendous impact on the returns you receive on your investments. And if you understand how it works and how to interpret it, a yield curve can even be used to help gauge the direction of the economy.

Most often the universe of bonds represented by a particular yield curve is limited by bond type—the one you'll probably hear referred to most often as "the yield curve" reflects the short, intermediate, and long-term rates of US Treasury securities. The Treasury yield curve is often referred to as a proxy for investor sentiment on the direction of the economy. A yield curve can refer to other types of bonds, though, such as the AAA Municipal yield curve, or reflect the narrower universe of a particular issuer, such as the GE or IBM yield curve.

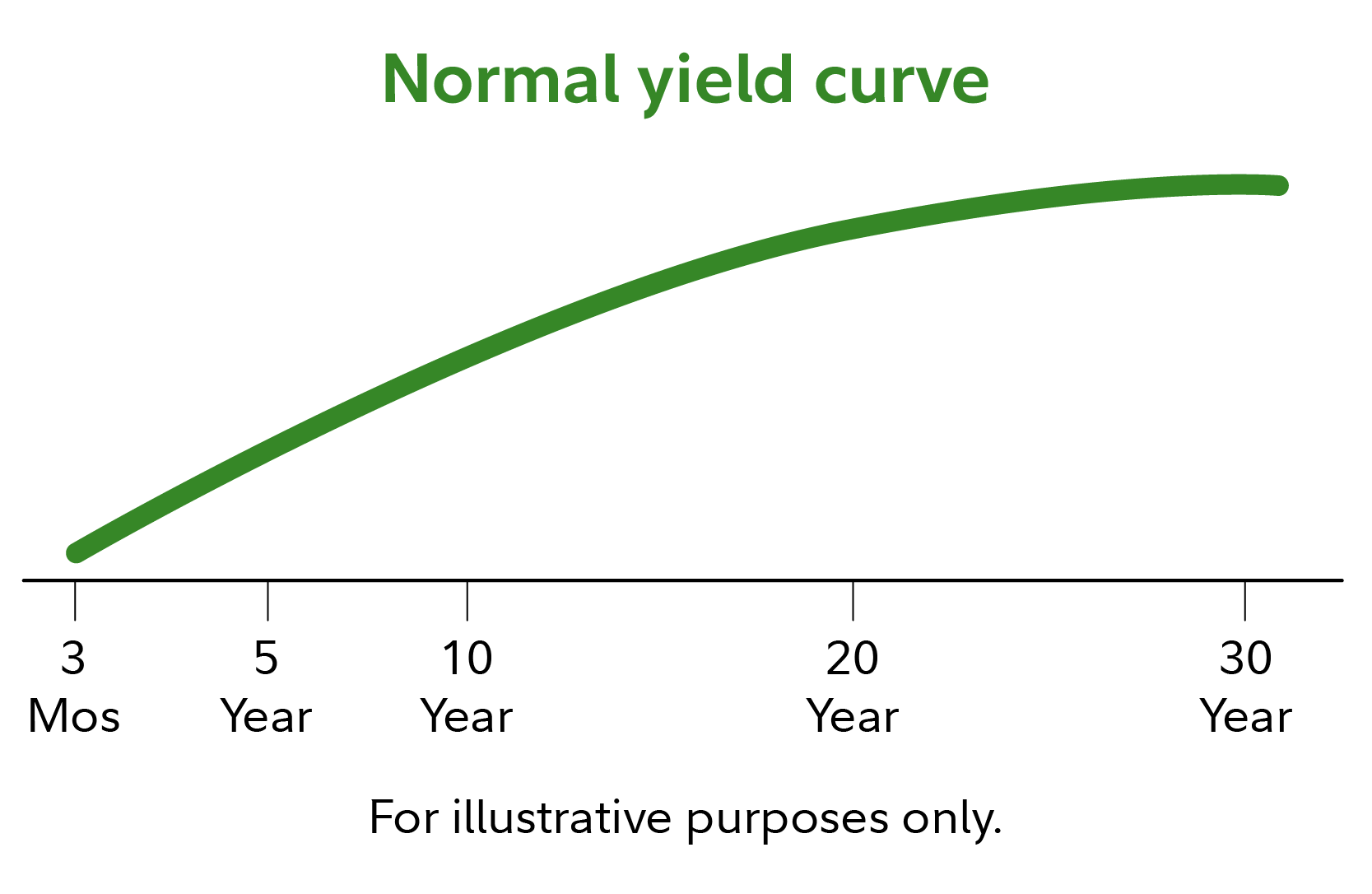

The normal yield curve

In general, short-term bonds carry lower yields to reflect the fact that an investor's money is at less risk. The thinking behind this is that the longer you commit funds, the more you should be rewarded for that commitment, or rewarded for the risk you take that the borrower may not pay you back. This is reflected in the normal yield curve, which slopes upward from left to right on the graph as maturities lengthen and yields rise. You'll generally see this type of yield curve when bond investors expect the economy to grow at a normal pace, without significant changes in the rate of inflation or major interruptions in available credit. There are times, however, when the curve's shape deviates, signaling potential turning points in the economy.

Steep curve

A steep yield curve is generally found at the beginning of a period of economic expansion. At that point, economic stagnation will have depressed short-term interest rates, which were likely lowered by the Fed as a way to stimulate the economy. But as the economy begins to grow again, one of the first signs of recovery is an increased demand for capital, which many believe leads to inflation. At this point in the economic cycle long-term bond investors fear being locked into low rates, which could erode future buying power if inflation sets in. As a result, they demand greater compensation—in the form of higher rates—for their long-term commitment.

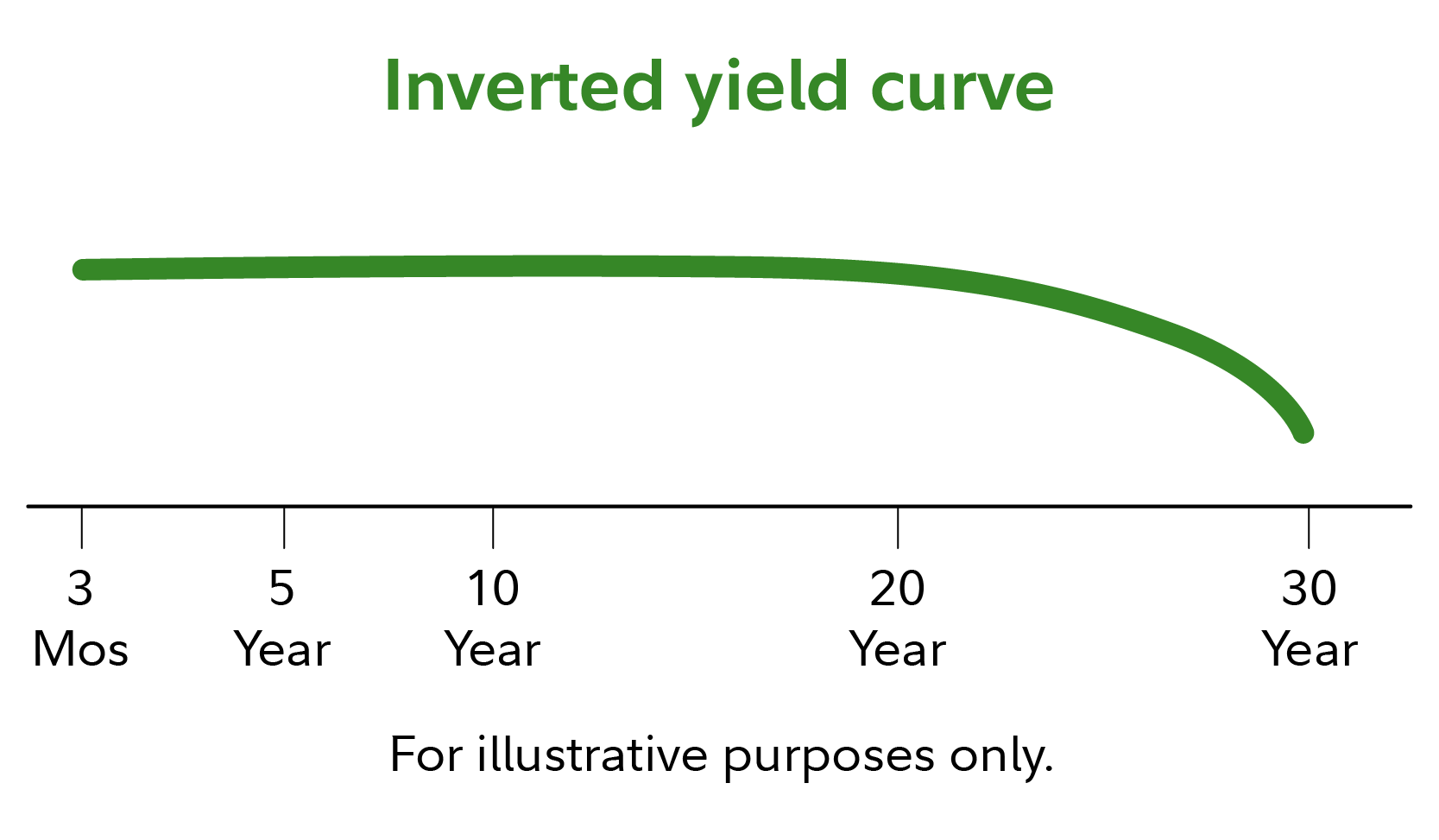

Inverted curve

At first glance, an inverted yield curve seems counterintuitive. Why would long-term investors settle for lower rewards than short-term investors, who are assuming less risk? The answer: When long-term investors believe that this is their last chance to lock in current rates before they fall even lower, they become slightly less demanding of lenders. As you might expect, since lower interest rates generally mean slower economic growth, an inverted yield curve is often taken as a sign that the economy may soon stagnate. While inverted yield curves are rare, investors should never ignore them. They are very often followed by economic slowdown—or an outright recession—as well as lower interest rates along all points of the yield curve.

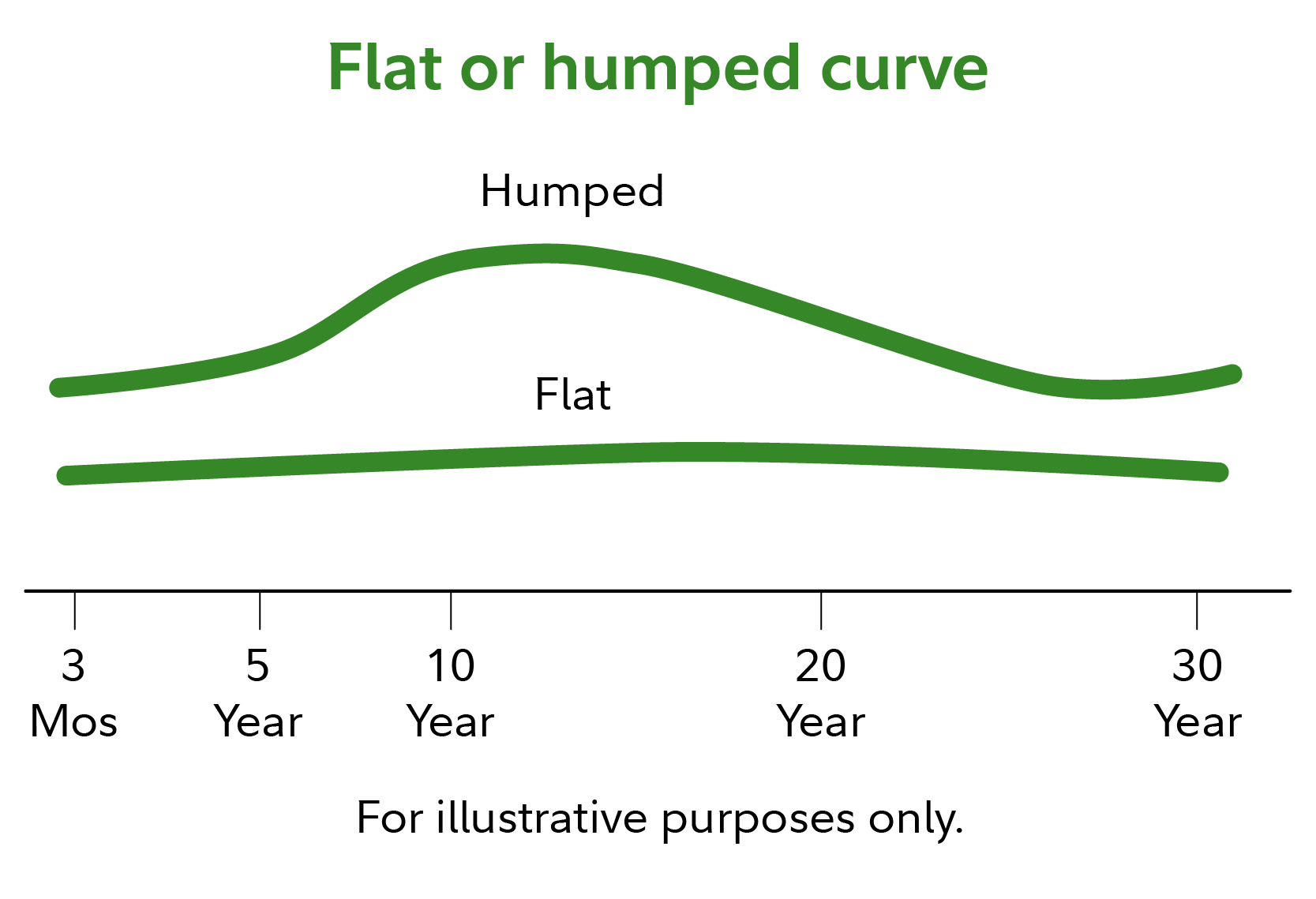

Flat or humped curve

Before a yield curve can become inverted, it must first pass through a period where short-term rates rise to the point they are closer to long-term rates. When this happens the shape of the curve will appear to be flat or, more commonly, slightly elevated in the middle.

While it's important to note that not all flat or humped curves turn into fully inverted curves, you shouldn't discount a flat or humped curve. Historically, economic slowdown and lower interest rates follow a period of flattening yields.

Using yield curves

In addition to using the shape of the Treasury yield curve to help determine the current and future strength of the economy, the Treasury yield curve occupies a special place compared to all other yield curves as it is generally regarded as the "benchmark curve." Yields on Treasury bonds and other securities are generally among the lowest because they’re backed by the full faith and credit of the US government. This allows bond investors to compare the Treasury yield curve with that of riskier assets such as the yield curve of Agency bonds or A-rated corporate bonds for example. The yield difference between the two is referred to as the "spread." The closer the yields are together the more confident investors are in taking the risk in a bond that is not government-backed. The spread generally widens during recessions and contracts during recoveries.