"Smart beta" strategies have attracted attention—and investors' dollars—in recent years. Funds that follow smart beta strategies combine elements of active and passive investing. Some seek to outperform broad market indexes, some focus on generating income, and others seek to reduce volatility and risk.

While the emergence of smart beta funds is a recent phenomenon, the underlying investment philosophy has been around for decades. These funds rely on factors. A factor is simply an attribute—such as the quality or size of a company—that may help explain risk and returns.

To achieve their goals, smart beta funds track indexes that are constructed around one or more factors. For example, a fund that is based on the quality factor would track an index that is composed of companies that generate superior profits, strong balance sheets, and stable cash flows. A company’s size is another factor. Small-cap stocks have historically outperformed large-cap stocks, although leadership can shift over shorter periods.

The seeds of factor-based investing were sown with the introduction of the capital asset pricing model (CAPM) in the 1960s. This first and most basic factor model suggested that a single factor—market exposure—helped to explain a stock’s performance relative to its index. The remainder of a stock’s performance was attributed to company-specific factors, such as earnings, new product launches, management changes, etc.

Over the past few decades, academics and investment professionals have identified additional factors and exposures that have historically outperformed the market or reduced a portfolio's level of risk over time. Five of the most common factors employed by investment professionals include:

- Size: Small-cap stocks are typically more volatile and have a higher risk of bankruptcy than large-cap stocks. Investors expect to be compensated for tolerating this additional risk. As a result, small-cap stocks have outperformed large-cap stocks over longer periods of time.

- Value: Earnings drive stock valuations and, theoretically, inexpensive stocks should outperform stocks with higher valuations. For example, when cheaper stocks report higher-than-expected earnings, they often outperform due to improved optimism about a company’s future earnings potential. There are other ways to define value beyond earnings per share, including cash flows and earnings yield. Factor-based investors often rely on a multifactor approach to identifying value stocks.

- Momentum: Research has found that stocks that have outperformed in the medium term often continue to perform well, and vice versa. These trends are based on the argument that a stock will catch investors' attention only after it has outperformed for a while. Only then will more investors pile into a trade and propel it even higher. One common way to measure momentum is to classify stocks by 12-month price returns, which has proven to be an effective strategy for outperforming the broader market over time.*

- Quality: For a company to maintain higher profit margins than its competitors, it needs to have some type of a competitive advantage. This could be a superior product, better customer service, or a lower cost structure. Stocks of high-quality companies that generate superior return on equity, strong balance sheets, and stable cash flows have tended to outpace the market over time.*

- Low volatility: The primary objective of the low volatility factor is to achieve higher risk-adjusted returns. Research has shown that low-volatility portfolios may outperform the broader market over time and provide a smoother ride along the way.* Stocks with stable revenues and earnings are also less susceptible to recessions and other macroeconomic events. Low volatility stocks tend to hold up better when markets decline rapidly, but may lag during strong market rallies.

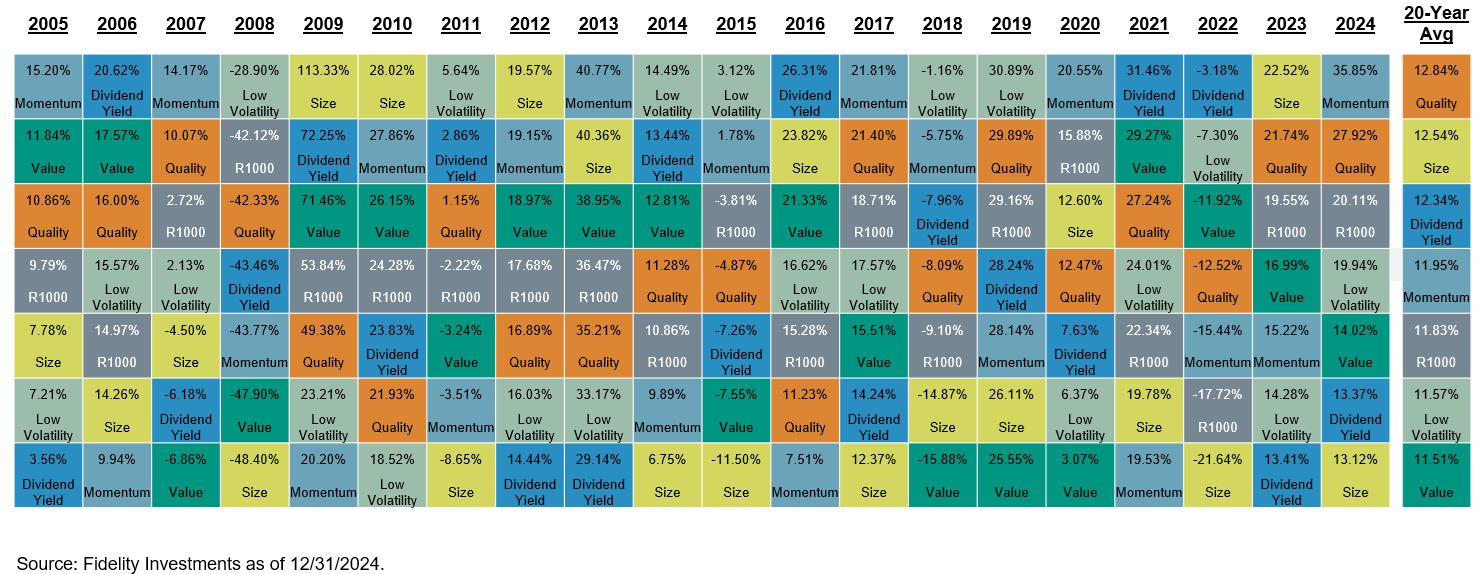

The cyclicality of factors

Understanding the factors that drive equity returns can help you choose the right mix of investments for your goals and risk tolerance. But it's important to note that no single factor works well all the time and that factor returns tend to be cyclical.

For example, small-cap stocks may underperform large-cap stocks for long periods of time. Swift changes in market direction—such as occurred in the wake of the 2008-2009 financial crisis—can have a negative impact on momentum strategies. In addition, high-quality value stocks may underperform growth stocks during the early stages of an economic cycle.

Most factors are not highly correlated with one another and different factors may perform well at different times. No single factor works all the time, and each experiences periods of out- and underperformance (see below).

Hypothetical annual returns of factor strategies versus the broader market - 2005-2024 (see Methodology below)

Trying to time these factors correctly can be challenging for individual investors. But that doesn't mean that smart beta strategies don't deserve consideration within your portfolio. Just as most investors diversify across asset classes, long-term investors may also want to consider professionally managed investments that focus on single factors or diversify across multiple factor strategies.