Fidelity Youth®

The only brokerage account teens ages 13–17 can own independently1 for investing + learning—while parents stay connected.

Fidelity Youth® Account benefits

Helping the next generation grow their knowledge, build smart money habits, and plan for the future.

![]()

$0 fees to open

The Fidelity Youth® Account has no subscription fees, no account fees, and no minimum balances to open.2

![]()

Investing with as little as $1

Fractional shares make it easy to start small and build confidence, with investments starting at $1.

![]()

Debit card available

Teens can optionally request a debit card to make purchases directly from their Youth Account.

Safe and sound

Parents have full visibility into their teen’s account and can monitor their investments, review transactions, and get notifications to help guide and oversee account activity.

Plus, the Fidelity Youth® Account is covered by SIPC and secured with the Fidelity Customer Protection Guarantee.

Investing and education—together in the Fidelity Investments® app

Fidelity Youth is now part of the Fidelity Investments app, with powerful tools and approachable content all in one place.

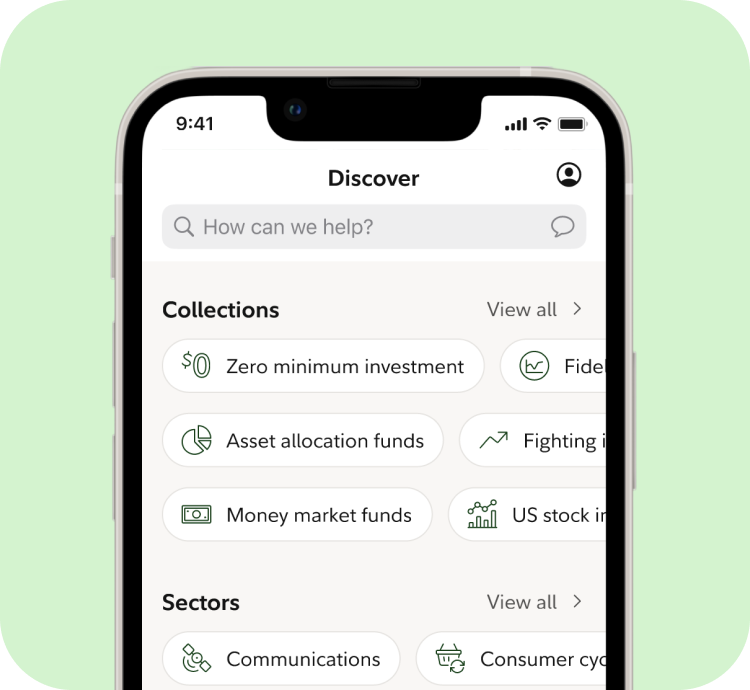

More ways to explore markets

Browse investments by sector, collection, or market movers. Use enhanced charts and watchlists to track opportunities and trends over time.

![]()

Seamless money transfers

Parents can quickly and easily transfer money from their Fidelity account to their teen’s Youth Account to support saving, investing, and other financial priorities.

Teen-friendly learning

Explore articles and videos designed to help make money topics clear and approachable, from saving and budgeting to investing basics.

1005788.30.0