Fidelity Go®

A robo advisor option for your retirement savings

Pick the Fidelity Go IRA that's right for you, and a human-backed robo advisor manages and rebalances the investments in your account for you.

Whether you prefer to choose your own individual investments, keep it simple with a single fund, or let us manage your investments for you—we offer you the flexibility to invest your IRA your way.

Discover investments and the information you need in order to understand how they may fit into your portfolio.

Discover investments and the information you need in order to understand how they may fit into your portfolio.

Get diversification and professional management in one fund according to your goals and comfort with risk.

Get diversification and professional management in one fund according to your goals and comfort with risk.

Fidelity can help build and manage a portfolio that fits your needs, depending on your IRA type.

Pick the Fidelity Go IRA that's right for you, and a human-backed robo advisor manages and rebalances the investments in your account for you.

With Fidelity Managed FidFolios, choose from 4 different investing strategies and let our team build and maintain a diversified stock portfolio for you.

Get 1-on-1, proactive, comprehensive planning for your full financial picture— retirement, health care, leaving a legacy and more. Partner with your advisor, and get additional support from a team of specialists.

Our step-by-step experience helps guide you through your choices to find an approach that fits your goals and investing style—whether you choose to invest on your own or with our help.

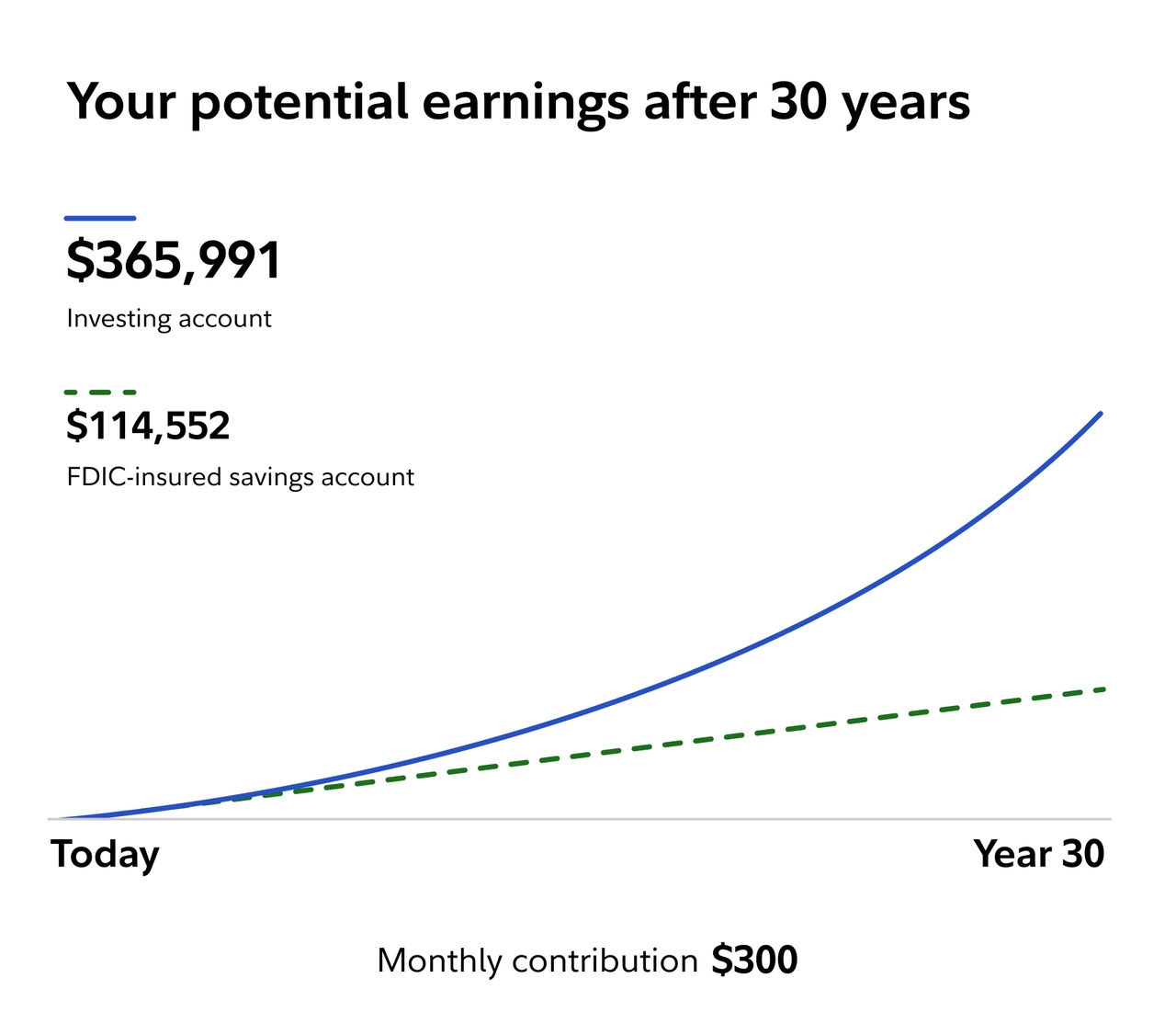

This chart is a hypothetical comparison. Investing involves risk of loss, and performance is not guaranteed. How we got these numbers

This chart shows an example of how investing $300 monthly for 30 years could result in $365,991, compared to $114,552 if left in a FDIC-insured savings account.

This chart is a hypothetical comparison. Investing involves risk of loss, and performance is not guaranteed. How we got these numbers

Loading

Loading may take a few moments.

Smart investing starts with a plan. Here's how to create one that fits your goals.

Consider putting your money to work by investing for potential growth.

Help your retirement savings grow over time automatically with recurring investments. Select your investments and set your contributions for the amount, frequency, and day of your choosing.

Build your future on your terms with an interactive planning experience that lets you explore scenarios, track your progress, and get guidance—all in one place.

IMPORTANT: The projections or other information generated by the Planning & Guidance Center's Retirement Analysis regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Your results may vary with each use and over time.

ETFs are subject to market fluctuation and the risks of their underlying investments. ETFs are subject to management fees and other expenses.

Fidelity Freedom Funds are designed for investors who anticipate retiring in or within a few years of the fund's target retirement year at or around age 65 and plan to gradually withdraw the value of their account in the fund over time. Except for the Freedom Retirement Fund, the funds' asset allocation strategy becomes increasingly conservative as the funds approach the target date and beyond. Ultimately, the funds are expected to merge with the Freedom Retirement Fund. The investment risk of each Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocation decisions of the Investment Adviser. Pursuant to the Adviser's ability to use an active asset allocation strategy, investors may be subject to a different risk profile compared to the fund's neutral asset allocation strategy shown in its glide path. The funds are subject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad, and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities. Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target date fund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirement income at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds' target dates.

Screenshots are for illustrative purposes only.

** Applies to online U.S. equity trades and exchange-traded funds (ETFs). $0 commission does not apply to customers designated by Fidelity as a Professional Equity Trader who are subject to an equity commission charge of $0.001 per share rounded up to the nearest $0.01 on a per order basis. For complete details on pricing please see: Fidelity.com/commissions. A limited number of ETFs are subject to a transaction-based service fee of $100. See full list of ETFs subject to this service fee here. Other exclusions and conditions may apply. Employee equity compensation transactions and accounts managed by advisors or intermediaries through Fidelity Institutional are subject to different commission schedules.

Stock markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. Investing in stock involves risks, including the loss of principal.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa. This effect is usually more pronounced for longer-term securities.) Fixed income securities also carry inflation risk, liquidity risk, call risk, and credit and default risks for both issuers and counterparties. Unlike individual bonds, most bond funds do not have a maturity date, so holding them until maturity to avoid losses caused by price volatility is not possible. Any fixed income security sold or redeemed prior to maturity may be subject to loss.

Fidelity Go®, Fidelity® Wealth Services, and Fidelity Managed FidFolios® are advisory services offered by Strategic Advisers LLC (Strategic Advisers), a registered investment adviser, for a fee. Brokerage services provided by Fidelity Brokerage Services LLC (FBS), and custodial and related services provided by National Financial Services LLC (NFS), each a member NYSE and SIPC. Strategic Advisers, FBS and NFS are Fidelity Investments companies.

Fidelity Crypto® for IRAs is offered by Fidelity Digital Assets®

Crypto as an asset class is highly volatile, can become illiquid at any time, and is for investors with a high risk tolerance. Crypto may also be more susceptible to market manipulation than securities. Crypto is not insured by the Federal Deposit Insurance Corporation, the Securities Investor Protection Corporation, or any other government agency, and is not an obligation of any bank.

Investors in crypto do not benefit from the same regulatory protections applicable to registered securities. Fidelity Crypto® accounts and custody and trading of crypto in such accounts are provided by Fidelity Digital Assets, National Association, which is a national trust bank. Brokerage services in support of securities trading are provided by Fidelity Brokerage Services LLC (“FBS”), and related custody services are provided by National Financial Services LLC (“NFS”), each a registered broker-dealer and member NYSE and SIPC.

Neither FBS nor NFS offer crypto as a direct investment nor provide trading or custody services for such assets. Fidelity Crypto and Fidelity Digital Assets are registered service marks of FMR LLC.

Past performance is no guarantee of future results.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

Fidelity does not provide legal or tax advice. The information herein is general in nature and should not be considered legal or tax advice. Consult an attorney or tax professional regarding your specific situation.

Investing involves risk, including risk of loss.

Before investing in any mutual fund or exchange-traded fund, you should consider its investment objectives, risks, charges, and expenses. Contact Fidelity for a prospectus, an offering circular, or, if available, a summary prospectus containing this information. Read it carefully.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

1262852.1.0