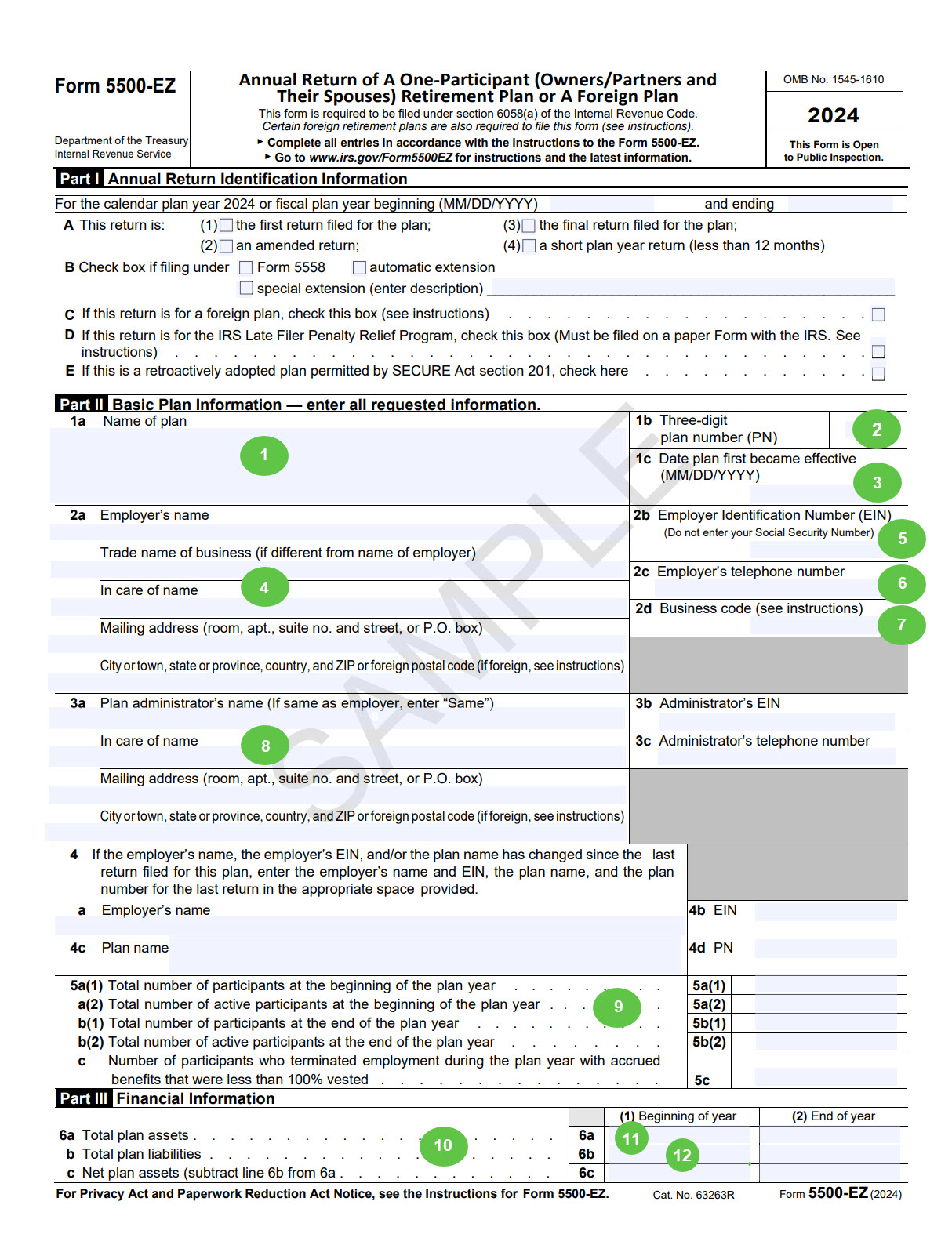

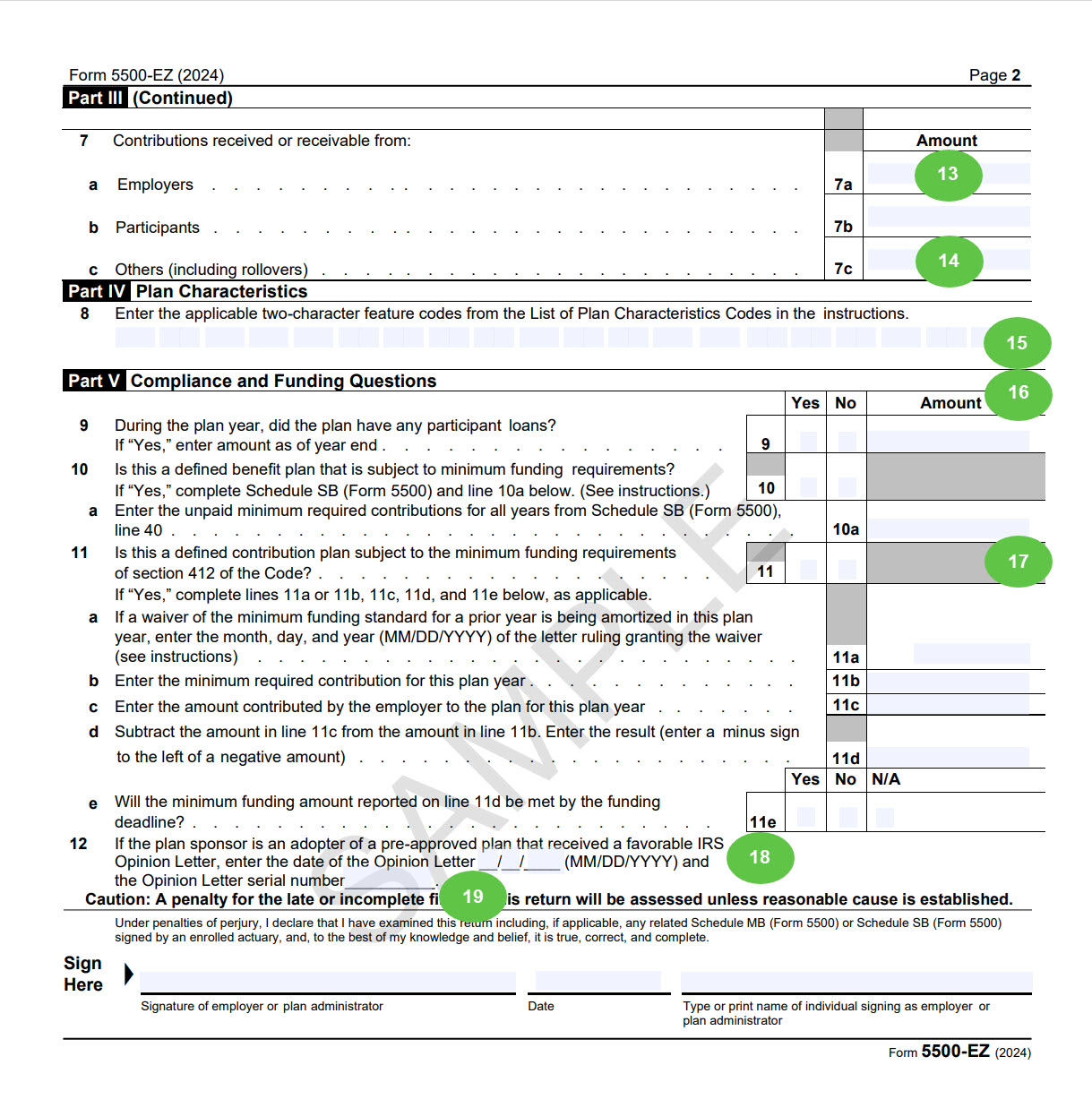

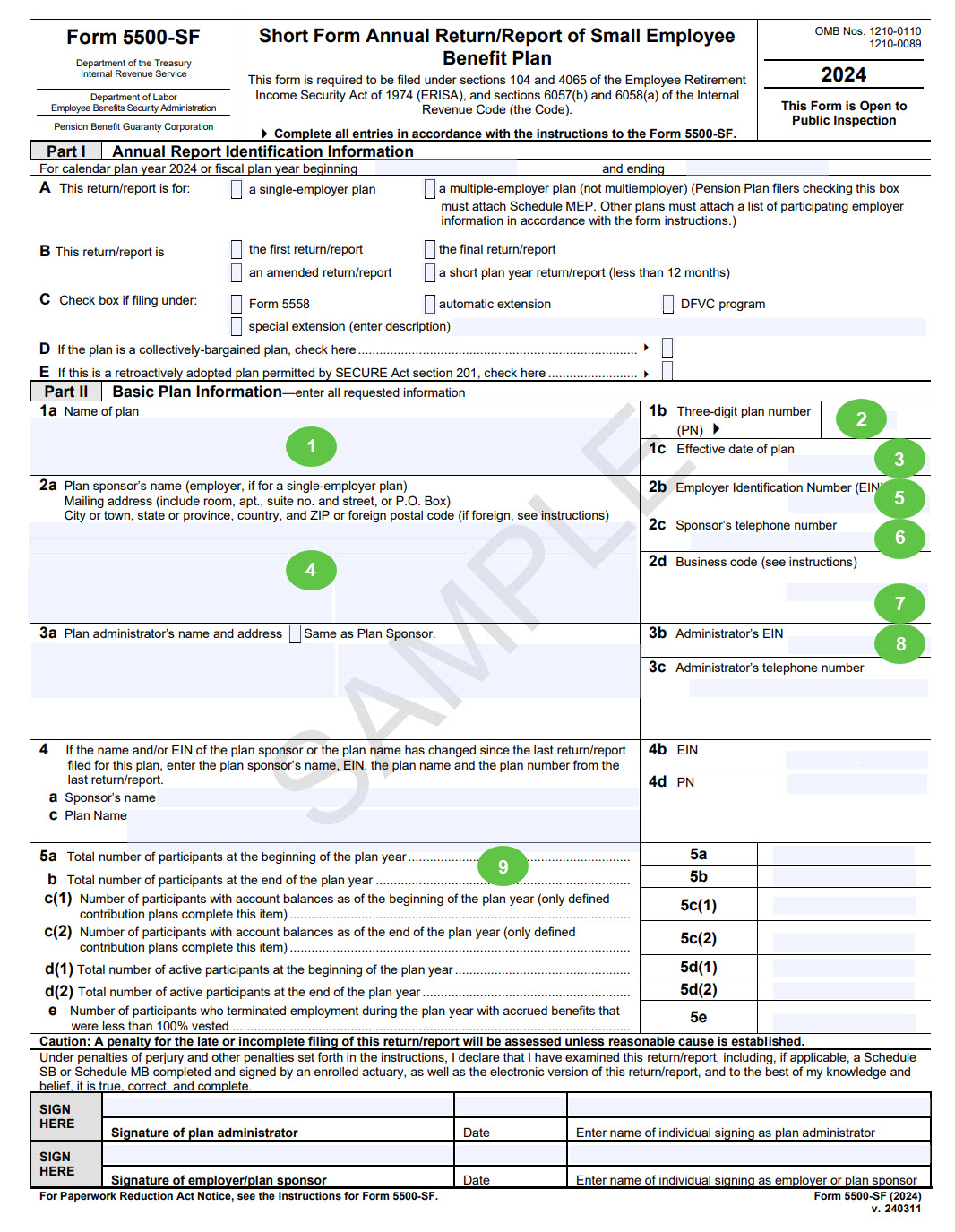

Who needs to file the form?

Form 5500 generally needs to be filed each year by plan administrators for:

- Keoghs (e.g., money purchase, profit sharing)

- Company pension (i.e. defined benefit) and company profit-sharing plans

- Certain 403(b) plans

- 401(k) plans

When statements and forms arrive

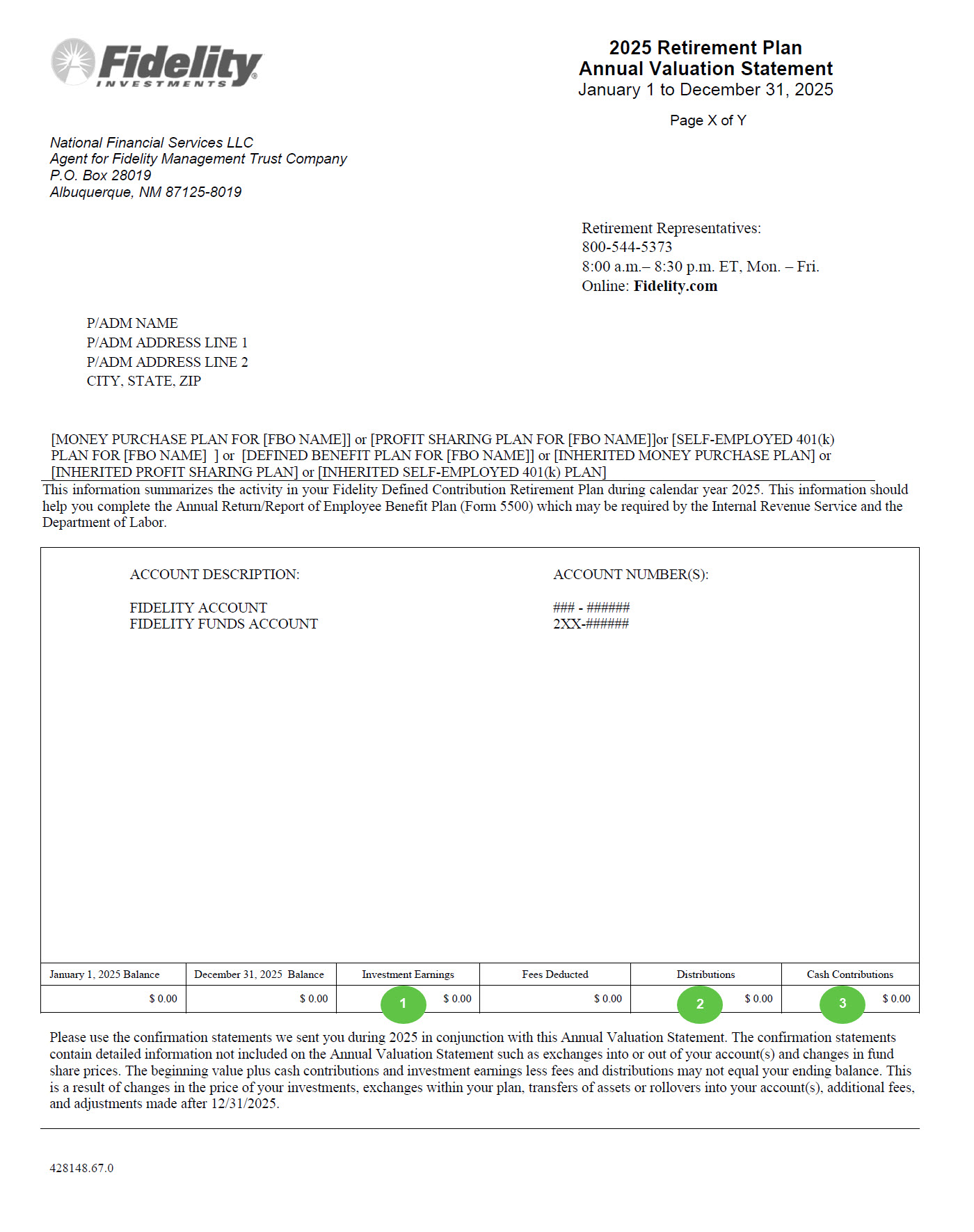

By April 30 every year, Fidelity mails and publishes online your Annual Valuation Statement (AVS), which provides the comprehensive plan information you need to complete your Form 5500. It's important to complete your form carefully; the federal government may impose penalties for non-compliance with filing regulations. Consult your tax advisor, the IRS, or the Employee Benefits Security Administration (EBSA) of the DOL with any questions.