Recharacterization calculation

How to calculate earnings

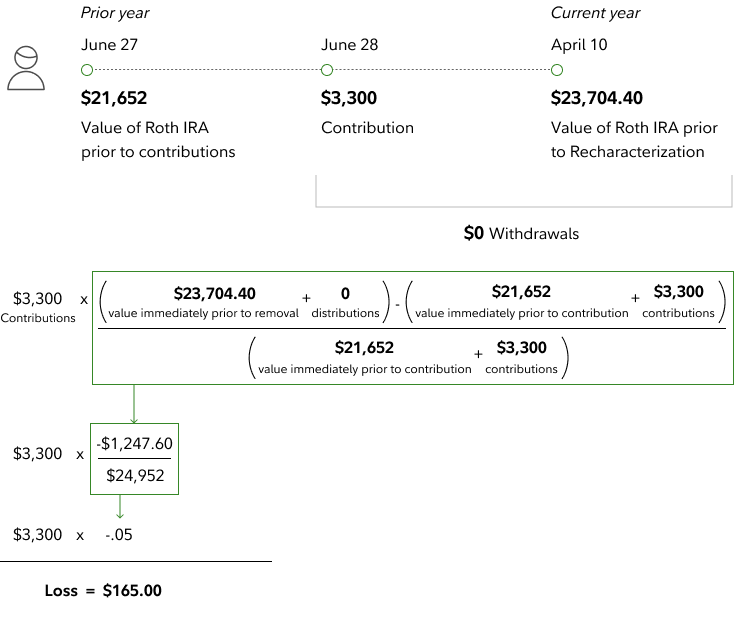

Example

Owen has a Roth IRA that was valued at $21,652 at the end of the day on June 27. On June 28, he made a $3,300.00 contribution to his account.

After completing his taxes for the prior year on April 10, he realized his income was too high to make a Roth IRA contribution, and on April 11 he requested to recharacterize his $3,300 contribution to his Traditional IRA. The market value of his Roth IRA at the end of the day on April 10 was $23,704.40.

Owen did not make any distributions- which includes transfers or return of excess withdrawals- from his Roth IRA while his contributions remained in his account.

Because Owen's Roth IRA decreased in value while his contribution remained in his account, he will recharacterize $3,135 to his Traditional IRA