What is sustainable investing?

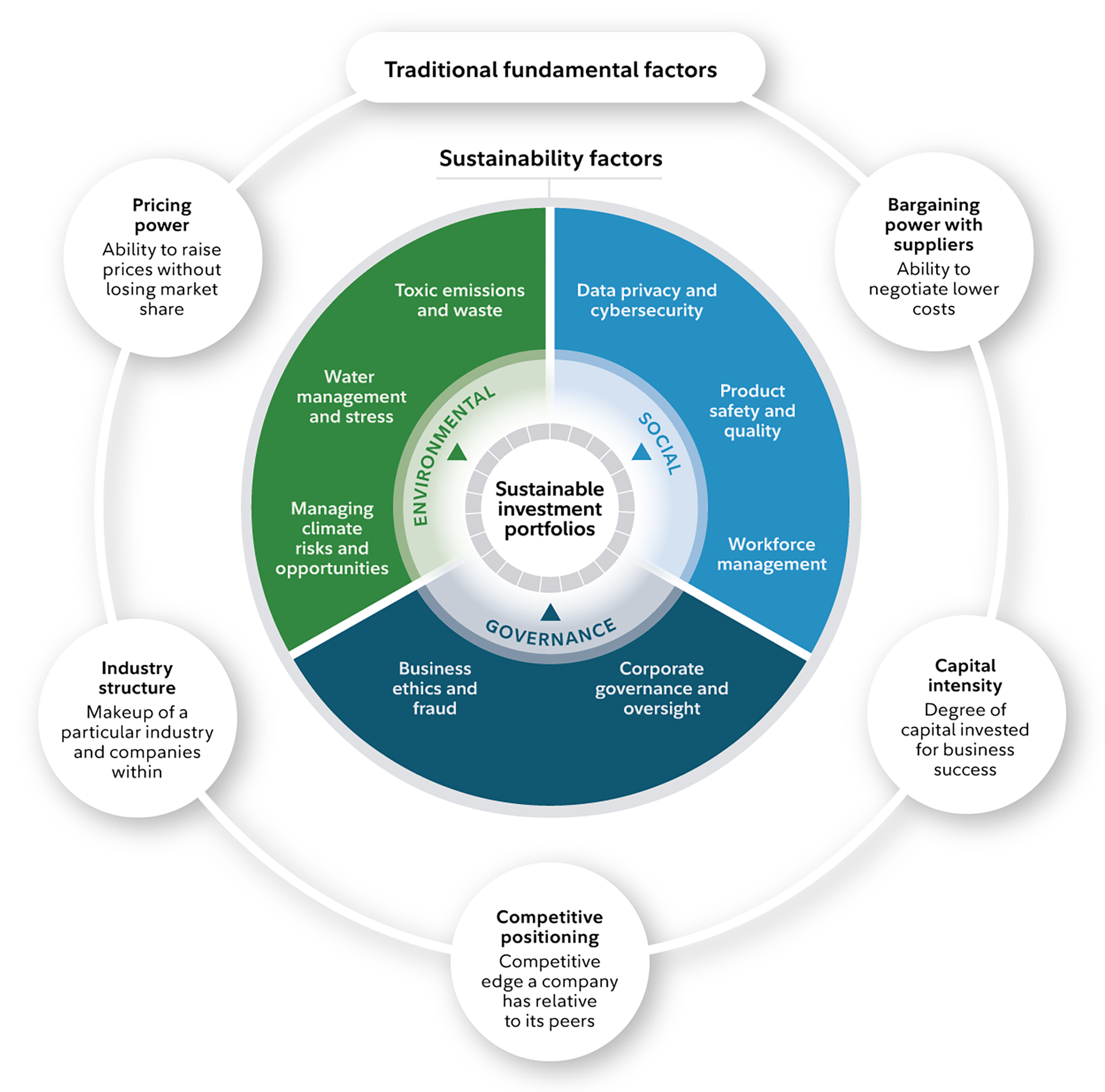

Sustainable investing offers another way to evaluate companies. Our active sustainable investment portfolios focus on key factors that our research shows drive financial results. This includes assessing financially-material environmental, social, and governance factors.

Environmental

Evaluate how efficiently companies manage their environmental resources and the potential risks and opportunities this poses for long-term success.

Social

Assess how companies prioritize the well-being of their employees, suppliers, customers, and the communities in which they operate.

Governance

Examine how effectively companies manage their oversight structure, strategy, operations, and internal processes over the long term.

2024—2025 sustainable investing and stewardship update

Fidelity is committed to building our expertise in sustainable investment research and stewardship. We're excited to share our latest progress and priorities.

Learn more about sustainable investing

Water stocks: Time to take the plunge?

Learn how big dollars are flowing into water sustainability.

2023—2024 sustainable investing report

Discover how our core principles guided our 2023—24 sustainable investing and stewardship efforts.

Investing in ideas

Want to invest according to your personal beliefs and values? Thematic investing helps investors put their money where their beliefs are.

Fidelity offers multiple ways for you to invest sustainably

For sustainability-focused customers, Fidelity offers diverse funds backed by decades of research and investment expertise. Our active, broad-based sustainable investments seek out companies, issuers, or securities with strong environmental, social, and governance (ESG) profiles, while our thematic offering provides access to sustainability-linked investment trends.

Apply the below single-select filters to narrow down sustainable investment options

Fidelity® Sustainable Target Date Funds

Invests primarily in a diversified mix of sustainable assets that adjust over time based on an investor's target retirement date, providing a lifetime investment option in a single fund.

FAPHX

Fidelity® Healthy Future Fund

Fidelity® Healthy Future Fund

Invests in companies working to improve life expectancy, enhance people's lives, and decrease negative environmental impacts.

FCAEX

Fidelity® Climate Action Fund

Fidelity® Climate Action Fund

Invests in companies that are working to remove, reduce or mitigate the effects of climate change.

FFEBX

Fidelity® Environmental Bond Fund

Fidelity® Environmental Bond Fund

Invests in the debt of companies and projects that are recognizing, disclosing, and reducing environmental risk.

FWOMX

Fidelity® Women's Leadership Fund

Fidelity® Women's Leadership Fund

Invests in companies that prioritize and advance women’s leadership and development.

FLOWX

Fidelity® Water Sustainability Fund

Fidelity® Water Sustainability Fund

Invests in companies helping to deliver safe, reliable, and easily accessible water.

FSLEX

Fidelity® Environment & Alternative Energy Fund

Fidelity® Environment & Alternative Energy Fund

Focuses on alternative and renewable energy, energy efficiency, pollution control, water infrastructure, waste and recycling technologies, or other environmental support services.

FRNW

Fidelity® Clean Energy ETF

Fidelity® Clean Energy ETF

Invests in companies that distribute, produce or provide technology or equipment to support the production of energy from solar, wind, hydrogen, and other renewable resources.

FIAEX

Fidelity® Sustainable Core Plus Bond Fund

Fidelity® Sustainable Core Plus Bond Fund

Provides exposure to debt securities of all types believed to have positive ESG benefits.

FAPGX

Fidelity® Sustainable Low Duration Bond Fund

Fidelity® Sustainable Low Duration Bond Fund

Provides exposure to shorter maturity investment-grade debt securities believed to have positive ESG benefits.

FSIKX

Fidelity® Sustainable Intermediate Municipal Income Fund

Fidelity® Sustainable Intermediate Municipal Income Fund

Provides exposure to investment-grade municipal debt securities believed to have positive ESG benefits.

FSYRX

Fidelity® Sustainable International Equity Fund

Fidelity® Sustainable International Equity Fund

Provides exposure to developed market companies focused on robust ESG practices while seeking to maintain long-term growth.

FSYJX

Fidelity® Sustainable Emerging Markets Equity Fund

Fidelity® Sustainable Emerging Markets Equity Fund

Provides exposure to emerging market companies with an attractive ESG profile to provide value while minimizing risk.

FYMRX

Fidelity® Sustainable Multi-Asset Fund

Fidelity® Sustainable Multi-Asset Fund

Combines Fidelity’s expertise in asset allocation, stock selection and ESG integration to deliver an all-in-one diversified portfolio focused on long-term growth through exposure to sustainable securities.

FSEBX

Fidelity® Sustainable U.S. Equity Fund

Fidelity® Sustainable U.S. Equity Fund

Provides insight to current and future sustainable leaders through evaluating a company's ESG profile.

FITLX

Fidelity® U.S. Sustainability Index Fund

Fidelity® U.S. Sustainability Index Fund

Tracks a domestic stock benchmark that targets companies with high ESG ratings, while seeking to maintain broad market exposure.

FNDSX

Fidelity® Sustainability Bond Index Fund

Fidelity® Sustainability Bond Index Fund

Tracks a benchmark of investment-grade government, corporate, and asset-backed securities from issuers with strong sustainability profiles.

FNIDX

Fidelity® International Sustainability Index Fund

Fidelity® International Sustainability Index Fund

Tracks an international stock benchmark that targets companies with high ESG ratings, while seeking to maintain broad market exposure.

FSYD

Fidelity® Sustainable High Yield ETF

Fidelity® Sustainable High Yield ETF

An actively managed fixed income ETF that seeks to provide a high level of income through core exposure to high yield bonds with high ESG ratings.

Work with a Fidelity advisor

As a Fidelity® Wealth Management client, you can work with an advisor2 who can help to build a personalized plan around your full financial picture, and help to choose an investment solution designed to support your vision for the future.

Sustainable Personalized Portfolios account

Professionally managed multi-asset class portfolios with built-in, tax-smart strategies,3 seeking to maximize returns for a given level of risk while prioritizing sustainable investments.4

- Environmental

- Social

- Governance

Fidelity® Strategic Disciplines Environmental Focus Strategy

A separately managed account (SMA) that seeks to build a portfolio with reduced exposure to companies that have less favorable environmental ratings while approximating the risk characteristics and pre-tax returns of the Fidelity® U.S. Large Cap Index, while looking to boost after tax returns in taxable accounts.5

- Environmental

Digital investment management and advice

Once you work with Fidelity online to choose an investment strategy, you can explore our online planning resources to get clear next steps and track your progress.

Fidelity Managed FidFolios® Environmental Focus Strategy

A diversified portfolio of stocks that invests in some of the largest US companies while seeking to reduce environmental footprint and enhance after-tax returns through the use of tax-smart investing techniques.3, 5

- Environmental

No results match your selection. Try choosing fewer options.

How to get started investing sustainably

Open and fund your brokerage account

Research our sustainable funds

Choose a fund and select buy