The years immediately leading to retirement are a critical time for accumulating assets and developing a plan for how you want to spend your life after work. But the final stretch before retirement—especially the last year of employment—can be an important time to make decisions about income, benefits, taxes, and withdrawals, which together may have a significant impact on your finances.

Across the board you’ll need to make choices regarding your 401(k), health care, pension, and tax strategy. These will be part of a financial blueprint that reflects your post-work needs as you shift from earning an income to drawing down your savings. This blueprint should outline your goals, income sources, and expenses in retirement, and it should also provide the basis for your investment portfolio and the investing decisions you’ll need to make.

What do your retirement savings need to cover?

Your retirement savings need to do more than fund daily living costs such as housing, food, and health care. They must also fund unexpected or emergency expenses. Just as important, they should fund your discretionary expenses, which can include hobbies, travel, entertainment, and other things that may help you enjoy your life once you stop working.

A traditional retirement plan is often described as a 3-legged stool:

- Short-term savings for immediate needs.

- Guaranteed income for core expenses, such as Social Security, pensions, or annuities.

- Investment accounts, including savings in tax-advantaged accounts such as IRAs and workplace plans like 401(k)s, as well as in brokerage accounts that are not tax-advantaged.

It’s this third leg—investments—that tends to be the most complex to manage. These assets need to support your current needs with ongoing and sometimes mandatory withdrawals (RMDs), as well as generate growth, typically for decades.

Fidelity estimates that retirees should try to replace up to 80% of pre-retirement income. But the reality is that many people don’t have pensions and Social Security may only replace about 35% of this income. That means retirement savings must often shoulder the rest, making your asset allocation plan particularly crucial.

Evaluate your income sources

Once you’ve defined how much money you’ll need to spend to sustain your lifestyle, that amount will become the foundation for your portfolio allocation and withdrawal planning.

A key step is to identify any gap between your sources of income and your expected expenses. Fidelity suggests that essential expenses—such as housing, food, and health care—should be paid for with predictable income such as Social Security benefits, income from pensions, and annuities. For investors who don’t have a traditional pension, one way to create additional guaranteed income may be to consider purchasing an annuity. Your investment portfolio can then be used to fund discretionary expenses and to provide longer-term growth.

Review your portfolio’s asset allocation

Three primary factors determine your asset allocation in retirement:

- Time horizon and goal length—when you plan to start withdrawing from your portfolio assets and how long you expect withdrawals from your portfolio assets to last in retirement. Fidelity assumes that someone retiring at age 65 should plan for a retirement lasting 30 years or more.

- Risk tolerance—your comfort level with market fluctuations.

- Personal circumstances—you may have different needs for income outside of your long-term plan.

A successful investing plan for retirement will find a balance between these 3 factors.

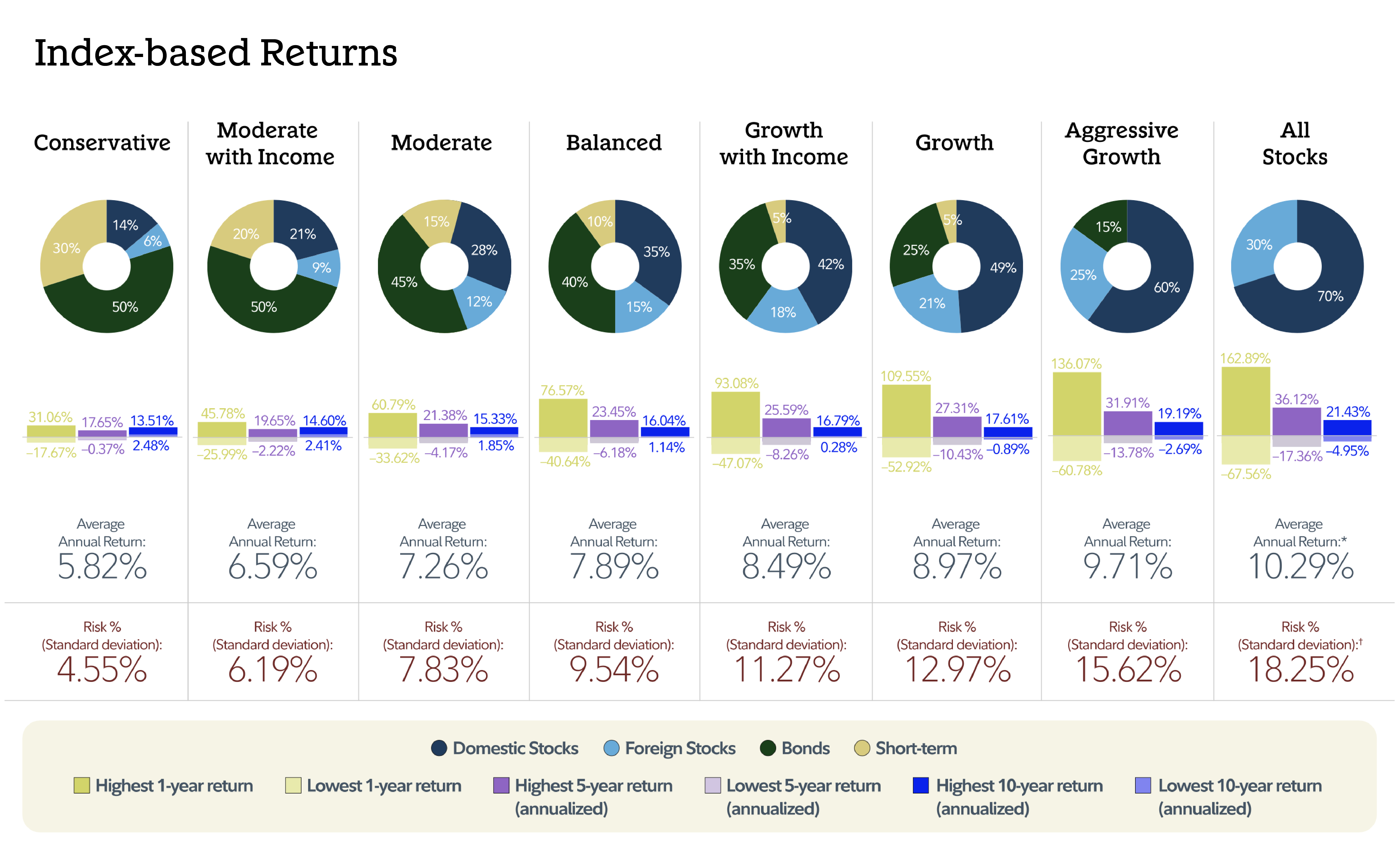

Many investors use target asset mixes (TAMs)—ranging from conservative to aggressive growth—to help them achieve their goals. Moving along this spectrum increases the percentage of stocks to bonds and short-term investments. A higher percentage of stocks may increase the potential for return, but it also may increase the potential for short-term losses and the volatility of your investments. In contrast, increasing the percentage of bonds and short-term cash could potentially decrease losses and swings in your portfolio’s value, but also limit growth. Over time, your asset mix will change due to market performance, and you’ll need to rebalance your portfolio to bring it back into alignment with your targeted mix.

If you’re a Fidelity customer, check out our Planning & Guidance Center to see your current asset mix plus suggestions for your mix.

Data source: Fidelity Investments and Morningstar Inc, 2025 (1926-2024). Past performance is no guarantee of future results. Returns include the reinvestment of dividends and other earnings. This chart is for illustrative purposes only. It is not possible to invest directly in an index. Time periods for best and worst returns are based on calendar year. Standard deviation is a statistical measure of how much a return varies over an extended period of time. The more variable the returns, the larger the standard deviation. Investors may examine historical standard deviation in conjunction with historical returns to decide whether an investment's volatility would have been acceptable given the returns it would have produced. A higher standard deviation indicates a wider dispersion of past returns and thus greater historical volatility. Standard deviation does not indicate how an investment actually performed, but does indicate the volatility of its returns over time. Standard deviation is annualized. The returns used for this calculation are not load adjusted. For information on the indexes used to construct this table, see Data Source in the notes below.1

Balance short-term needs with long-term growth

Once you’ve thought through your retirement goals, income needs, withdrawal needs from your portfolio, time horizon, and risk tolerance, the next step is deciding how to put these choices into practice through your investment choices.

Your asset allocation should support your goals, but these choices can evolve as your income needs, markets, or personal circumstances may change. For many retirees, this includes gradually shifting your portfolio to a more conservative asset allocation over time.

Concurrently, your portfolio should try to balance shorter-term needs with the need for growth over many decades. There is no one strategy to achieve your goals, and you may not be able to achieve all of your goals at once. Working with a financial professional may help you craft and adopt a plan.

Investment options that may support your strategy include:

Target date funds

Target date funds are built around a single retirement endpoint and adjust asset allocation over time, in many cases becoming more conservative over time. For example, they may be slanted more toward stocks when the targeted date is still decades away, and then gravitate more toward bonds or other potentially less volatile investments. These funds might be good for hands-off investors or people who want an approach where the level of risk decreases. Note that Fidelity’s target date funds are meant to be held throughout retirement, but not all target date funds are designed this way.

Target allocation funds

By contrast, target allocation funds invest regardless of age or investing time horizon. They are a mixture of stocks and bonds that could either maintain a neutral mix or adjust over time. For instance, a neutral mix could include 70% stocks, 25% bonds, and 5% of assets held in short-term or money market instruments. An adjusting allocation could achieve a similar mix by gradually shifting within ranges, such as between 50% and 100% stocks and 0% and 50% bonds or short-term money markets.

These funds might be appropriate for investors who want to assign a specific risk level to their investments. If you choose a target allocation fund as part of your retirement portfolio, you should periodically review whether the equity percentage aligns with your needs.

You can research Fidelity mutual fund investments, and find out more about target date and target allocation funds in Viewpoints: Diversification through a single fund.

Inflation-protected assets

Inflation-protected assets such as Treasury Inflation-Protected Securities (TIPS) and real assets such as property you own (or investments in things like real estate and commodities) can help preserve the value of your investments, as inflation is always a concern for retirees.

Fixed income and income-producing investments

Fixed income and income-producing investments such as bonds, bond ETFs, bond ladders, CDs and CD ladders, as well as dividend-paying stocks and income-producing mutual funds can help support discretionary spending and potential emergency needs in retirement.

These investments should not be used as a substitute for planning, but they can help you realize the financial blueprint you’ve already defined.

Create a withdrawal strategy

Determining a sustainable withdrawal rate—how much money you can withdraw from your retirement and other savings without risking the longevity of these funds—is a core element of retirement investment planning.

Generally, Fidelity recommends withdrawing no more than 4% to 5% from your portfolio in the first year of retirement and then adjusting for inflation in subsequent years. This withdrawal rate is likely to have a high degree of success in funding a 30-year retirement, according to Fidelity research.2

Keep in mind, however, that numerous things will affect your sustainable withdrawal rate, such as your own longevity, inflation, and market conditions.

Find out more about withdrawal rates in retirement in Viewpoints: How can I make my retirement savings last?

Manage sequence-of-return risk

Market conditions early in retirement can have an outsize impact on the long-term outcome of your portfolio.

For example, a market downturn early in retirement can significantly diminish your nest egg, especially if you don't reduce your withdrawals with the falling market. In contrast, a strong stock market early in retirement can provide a boost to your portfolio, potentially for decades.

A portfolio weighted more toward stocks may be more susceptible to sequence-of-return risk than a lower volatility portfolio, which may be weighted more toward bonds or other fixed income options. Sequence-of-return risk refers to potential portfolio exposure if the market hits a downturn in your initial years of retirement.

Fidelity generally recommends trying to increase expense flexibility prior to and in retirement to reduce sequence-of-return risk; for example, by adjusting withdrawals during market downturns. Cash, cash equivalents, short-term bond ladders, annuities, or securities that pay dividends can also produce cash flow and reduce the need to sell from your portfolio during market downturns.

Asset location

The process of determining the types of accounts to hold your retirement funds is called asset location, which typically refers to putting certain types of investments in the accounts where they make the most sense from a tax perspective.

Generally speaking:

- Investments that create more taxable income each year might be better kept in a tax-advantaged account, such as a Roth IRA or a traditional IRA.

- Investments that are more tax-efficient can go into a taxable account, such as a brokerage account.

As you approach retirement, it’s important to think about how asset location intersects with the timing of required minimum distributions (RMDs). For people born before 1960, RMDs must begin once you reach age 73. For people born in 1960 or later, RMDs must begin once you reach age 75. While RMDs shouldn’t drive your investment decisions, they do affect how and when assets are taxed, which consequently may affect which assets are held in which types of accounts.

Because RMDs are legally required withdrawals based on calculations by the Internal Revenue Service (IRS) based on your age and balances of your tax-deferred accounts, thought should be given to how the RMD will affect your individual tax situation as well as short- and long-term growth of your portfolio.

RMDs can also present planning opportunities. For example, if your portfolio has moved away from your target asset allocation, an RMD could help you rebalance your portfolio by selling assets that have become overweighted.

Find out more about asset location in Viewpoints: Are you invested in the right kind of accounts?

By coordinating asset location with RMD withdrawals you can help smooth out potential tax volatility while helping to provide more consistent after-tax income in retirement.

Stay the course

Finally, Fidelity advises against reacting to short-term market volatility with major portfolio changes. Instead, we suggest sticking to the financial plan you create prior to retirement. This is especially true if your financial situation, time horizon, and risk tolerance remain unchanged. Periodic reviews and smaller adjustments are preferable to frequent, large-scale changes.

A well-constructed investment plan that’s regularly reviewed and consistently applied can help give you confidence both in the period leading up to retirement and throughout retirement.