Before investing, consider the investment objectives, risks, charges, and expenses of the annuity and its investment options. Contact Fidelity for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

Guarantees apply to certain insurance and annuity products and are subject to product terms, exclusions and limitations and the insurer's claims‐paying ability and financial strength. They do not protect the value of the variable investment options, which are subject to market risk. The value of the variable investment options will fluctuate so that shares, when redeemed, may be worth more or less than the original cost.

1. Annuity withdrawals and other distributions of taxable amounts, including death benefit payouts, will be subject to ordinary income tax. For nonqualified contracts, an additional 3.8% federal tax may apply on net investment income. If withdrawals and other distributions are taken prior to age 59½, an additional 10% federal tax may apply. A withdrawal charge also may apply. Withdrawals will reduce the contract value and also may reduce the value of any rider benefits.

2. A 2% surrender charge may apply during the first 5 contract years.

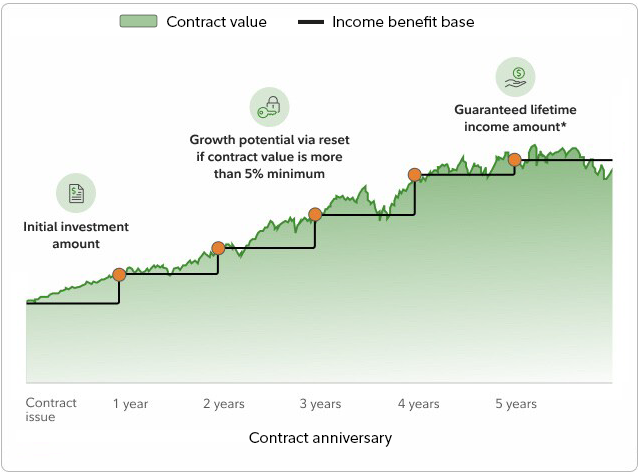

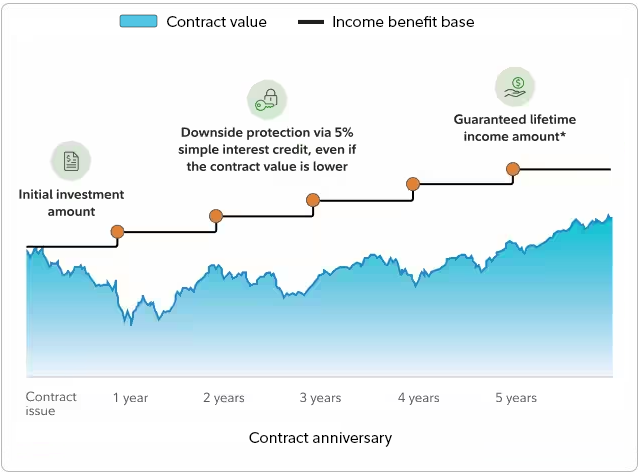

3. The Income Benefit Base has no cash value and is not available as a lump sum withdrawal.

4.

The performance of the Fidelity® VIP FundsManager® 60% portfolio depends on that of its underlying Fidelity and Fidelity VIP Funds. Fidelity VIP FundsManager 60% is subject to the volatility of the financial markets in the U.S. and abroad, and may by subject to the additional risks associated with investing in high-yield, commodity-linked, small-cap, and foreign securities. The portfolio is managed by FMR Co., Inc., an affiliate of FMR. Please see the fund prospectus for more information.

5. Net applicable fees.

6. Variable annuities are issued by Nationwide Life Insurance Company, Columbus, Ohio. The general distributor for variable products is Nationwide Investment Services Corporation, member FINRA, Columbus, Ohio.

Contract/Certificate: ICC22-VACC-0120AOCV, VACC-0120CACV, VACC-0120FLPP // VANN-0288FL, VACC-0120NDCV, VACC-0120AOCV, VACC-0120SCCV, ICC22-VARR-0139AO, VARR-0139CA, VARR-0139FL, VARR-0139AO

Fidelity Brokerage Services LLC, Member NYSE, SIPC, and Fidelity Insurance Agency, Inc., which are not affiliated or related to Nationwide and its affiliates, have agreed to act as distributors. The contract’s financial guarantees are solely the responsibility of the issuing company.

7. Pacific Life Retirement Growth and Income Annuity (Contract Form Series ICC22:10-1021, 10-2021) with the Guaranteed Lifetime Withdrawal Benefit (ICC22:20-1430, ICC22:20-1028, 20-2430, 10-2028) is issued by Pacific Life. State variations to contract form series and rider series may apply. The general distributor for Pacific Life variable products is Pacific Select Distributors, LLC (member FINRA & SIPC), a subsidiary of Pacific Life Insurance Company and an affiliate of Pacific Life & Annuity Company.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company or Pacific Life & Annuity Company. In New York, insurance products are only issued by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Fidelity Brokerage Services, Member NYSE, SIPC, and Fidelity Insurance Agency, Inc., are the distributors; they are not affiliated with any Pacific Life companies The contract's financial guarantees are solely the responsibility of the issuing company.

8. Please review product prospectus for charges associated with a specific contract.

Deferred variable annuities with guaranteed lifetime withdrawal benefits available at Fidelity are issued by third-party insurance companies, which are not affiliated with any Fidelity Investments company. These products are distributed by Fidelity Insurance Agency, Inc., and, Fidelity Brokerage Services, Member NYSE, SIPC. A contract's financial guarantees are solely the responsibility of and are subject to the claims-paying ability of the issuing insurance company.

Under current law, a nonqualified annuity that is owned by an individual is generally entitled to tax deferral. IRAs and qualified plans—such as 401(k)s and 403(b)s—are already tax‐deferred. Therefore, a deferred annuity should be used only to fund an IRA or qualified plan to benefit from the annuity' features other than tax deferral. These include lifetime income and death benefit options.

Fidelity does not provide legal or tax advice. The information herein is general in nature and should not be considered legal or tax advice. Consult an attorney or tax professional regarding your specific situation.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917