Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Fidelity does not provide legal or tax advice. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results. Fidelity cannot guarantee that the information herein is accurate, complete, or timely. Fidelity makes no warranties with regard to such information or results obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Consult an attorney or tax professional regarding your specific situation.

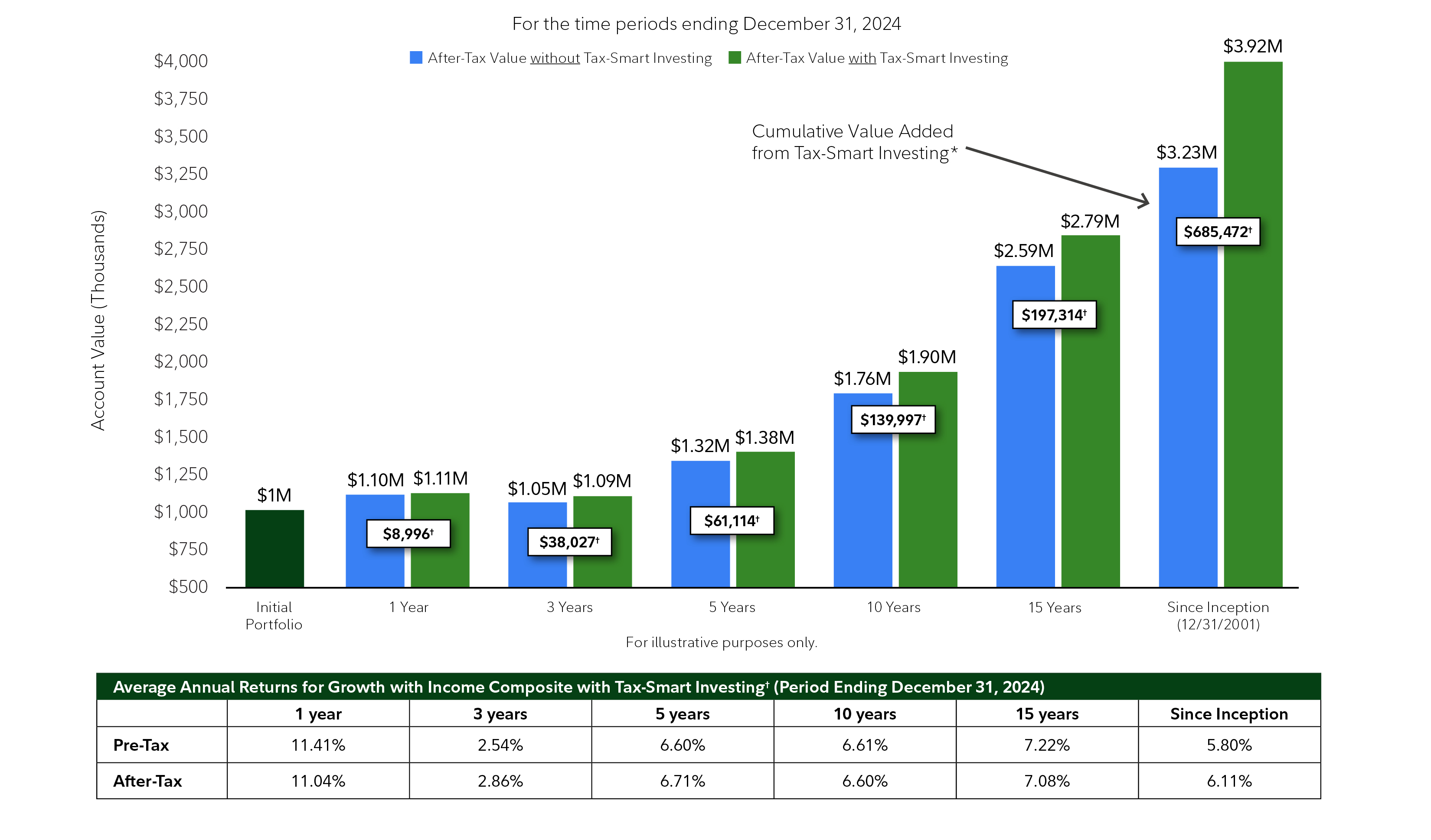

1. Tax-smart investing techniques, including tax-loss harvesting, are applied in managing certain taxable accounts on a limited basis, at the discretion of the portfolio manager, Strategic Advisers LLC (Strategic Advisers), primarily with respect to determining when assets in a client's account should be bought or sold. Assets contributed may be sold for a taxable gain or loss at any time. There are no guarantees as to the effectiveness of the tax-smart investing techniques applied in serving to reduce or minimize a client's overall tax liabilities, or as to the tax results that may be generated by a given transaction.

2. Important information about the methodology and assumptions and their related risks and limitations used in calculating this figure. Tax-loss harvesting is one of several tax-smart investing techniques we apply in managed portfolios. Tax savings will vary from client to client. In any given year it may offer significant benefits during volatile markets. Past performance is no guarantee of future results. Factors that could impact the value of our tax-smart investing techniques include market conditions, the tax characteristics of securities used to fund an account, client-imposed investment restrictions, client tax rate, asset allocation, investment approach, investment universe, the prevalence of SMA sleeves and any tax law changes. This analysis is based on the performance of all accounts in good order within investment strategies (offered through Fidelity® Wealth Services) within taxable account registrations from 1/1/2015 for the Total Return Blended strategy, and from 1/28/2019 for Total Return Fidelity-Focused and Index-Focused strategies and the Defensive approach (when tax-smart investment management capabilities were introduced), and from 06/30/2022 for Total Return Sustainable investment strategies through 12/31/2024. The analysis includes calculating the average of each year's average account’s capital gains tax savings over the past ten years. We estimate potential capital gains tax savings by multiplying each harvested tax loss by the applicable short- or long-term capital gains tax rate for each client account at the end of each year. The average account balance is $687,877, which is the average of each year's average account balance over the past ten years. The average balance has decreased over the course of the past ten years as we have seen a growth in the number of accounts after lowering minimums in recent years.

Our after-tax performance calculation methodology uses the full value of harvested tax losses without regard to any future taxes that would be owed on a subsequent sale of any new investment purchased following the harvesting of a tax loss. That assumption may not be appropriate in all client situations but is appropriate where (1) the new investment is donated (and not sold) by the client as part of a charitable gift, (2) the client passes away and leaves the investment to heirs, (3) the client's long-term capital gains rate is 0% when they start withdrawing assets and realizing gains, (4) harvested losses exceed the amount of gains for the life of the account, or (5) where the proceeds from the sale of the original investment sold to harvest the loss are not reinvested. Our analysis assumes that any losses realized are able to be offset against gains realized inside or outside of the client account during the year realized; however, all capital losses harvested in a single tax year may not result in a tax benefit for that year. Remaining unused capital losses may be carried forward to offset realized capital gains in subsequent years and up to $3,000 of ordinary income per year. It is important to understand that the value of tax-loss harvesting for any particular client can only be determined by fully examining a client's investment and tax decisions for the life the account and the client, which our methodology does not attempt to do. Clients and potential clients should speak with their tax advisors for more information about how our tax-loss harvesting approach could provide value under their specific circumstances.

3. For a list of eligible investments, see our Program Fundamentals or contact a Fidelity representative. Clients may elect to transfer noneligible securities into their accounts. Should they do so, Strategic Advisers or its designee will liquidate those securities as soon as reasonably practicable, and clients acknowledge that transferring such securities into their accounts acts as a direction to Strategic Advisers to sell any such securities. Clients may realize a taxable gain or loss when these shares are sold, which may affect the after-tax performance/return within their accounts, and Strategic Advisers does not consider the potential tax consequences of these sales when following a client's deemed direction to see such securities. Strategic Advisers reserves the right not to accept otherwise eligible securities, at its sole discretion.

4. While Strategic Advisers does consider the potential tax consequences of the sale of eligible securities used to fund an account managed with tax-smart investing techniques, Strategic Advisers believes that appropriate asset allocation and diversification are of primary importance and applies tax-smart investing techniques as a secondary consideration in managing such accounts. Accordingly, clients who fund an account managed with tax-smart investing techniques with appreciated securities should understand that Strategic Advisers could sell such securities notwithstanding that the sale could trigger significant tax consequences.

5. Information about how we calculate the value of tax-smart strategies. We use a proprietary methodology to calculate an average annual net excess return to help measure the value of the tax-smart investing techniques. Our calculation uses asset-weighted composite pre-tax and after-tax performance information for Fidelity Wealth Services accounts managed using the strategy characteristics listed above. We compare this composite performance information to a reference basket of mutual funds and ETFs that we use to construct a tax-smart account's after-tax benchmark. Each fund represents a primary asset class, and is weighted in the same proportion as the primary asset class in the account’s long-term asset allocation.

Average annual net excess return is calculated by subtracting pre-tax excess return from after-tax excess return. After-tax excess return is the amount by which the annualized after-tax investment return for the composite portfolio is either above or below the annualized after-tax benchmark return. Pre-tax excess return is the amount by which the annualized pre-tax investment return for the composite portfolio is either above or below the annualized pre-tax return of the reference basket of mutual funds and ETFs.

Important information about performance returns. Performance cited represents past performance. Past performance, before and after taxes, does not guarantee future results and current performance may be lower or higher than the data quoted. Investment returns and principal will fluctuate with market and economic conditions, and you may have a gain or loss when you sell your assets. Your return may differ significantly from those reported. The underlying investments held in a client’s account may differ from those of the accounts included in the composite. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Before investing in any investment product, you should consider its investment objectives, risks, and expenses. This material has been prepared for informational purposes only and is not to be considered investment advice or a solicitation for investment. Information contained in this report is as of the period indicated and is subject to change. Please read the applicable advisory program’s Form ADV Program Fundamentals, available from a Fidelity advisor or at Fidelity.com/information.

Market indexes are included for informational purposes and for context with respect to market conditions. All indexes are unmanaged, and performance of the indexes includes reinvestment of dividends and interest income, unless otherwise noted. Review the definitions of indexes for more information. Please note an investor cannot invest directly into an index. Therefore, the performance of securities indexes do not incorporate or otherwise reflect the fees and expenses typically associated with managed accounts or investment funds.

Information about the calculation of account and composite returns. Returns for periods of one year or less in duration are reported cumulative. Returns for periods greater than one year may be reported on either a cumulative or average annual basis. Calendar year returns reflect the cumulative rates of return for the 12-month period from January 1 to December 31, inclusively, of the year indicated.

Reported rates of return utilize a time-weighted calculation, which vastly reduces the impact of cash flows. Returns shown assume reinvestment of interest, dividends, and capital gains distributions. Assets valued in U.S. dollars. Performance for accounts managed without tax-smart investing techniques begins when assets are available in the account. Performance for accounts managed with tax-smart investing techniques ("tax-smart accounts") begins after the Investment Manager reviews the account and deems it ready for investment in the chosen strategy.

Rates of return shown are net of the actual investment advisory fees paid for each account, and are net of any applicable fee credits, any underlying fund's own management fees and operating expenses, and for certain Fidelity Wealth Services accounts the fees attributable to separately managed account sleeves. Performance information presented for an investment advisory program offered by Fidelity Personal Workplace Advisors LLC ("FPWA") includes performance for accounts enrolled in legacy programs previously offered and managed by FPWA’s affiliate, Strategic Advisers LLC, for periods prior to July 2018. Fees for these legacy programs differ from current fee schedules for FPWA's programs, and fees for accounts enrolled in those legacy programs may have been higher or lower than FPWA's current fees. Fee structures and the services offered have changed over time. Please consult a Fidelity financial advisor or the applicable investment advisory program's current Program Fundamentals for current fee information. Additional information about our methodology for calculating pre- and after-tax performance return information is available at Fidelity.com/information in a document titled "About Performance."

Assumptions used in calculating after-tax returns.

After-tax rate of return measures the performance of an account, taking into consideration the impact of a client’s U.S. federal income taxes, based on the activity in the account. Strategic Advisers does not actively manage for alternative minimum taxes; state or local taxes; foreign taxes on non-U.S. investments; federal tax rules applicable to entities; or estate, gift, or generation-skipping transfer taxes. Strategic Advisers relies on information provided by clients in an effort to provide tax-sensitive investment management and does not offer tax advice. Any realized short-term or long-term capital gain or loss retains its short- or long-term characteristics in the after-tax calculation. The gain/loss for any account is applied in the month incurred and there is no carryforward.

We assume that taxes are paid from outside the account. Taxes are recognized in the month in which they are incurred. This may inflate the value of some short-term losses if they are offset by long-term gains in subsequent months. After-Tax Returns do not take into account the tax consequences associated with income accrual, deductions with respect to debt obligations held in client accounts, or federal income tax limitations on capital losses. Withdrawals from client accounts during the performance period result in adjustments to take into account unrealized capital gains across all securities in such account, as well as the actual capital gains realized on the securities. Adjustments for reclassification of dividends from non-qualified to qualified status that occur in January of the subsequent year, are reflected in the prior December monthly returns. We assume that a client reclaims in full any excess foreign tax withheld and is able to take a U.S. foreign tax credit in an amount equal to any foreign taxes paid, which increases an account’s after-tax performance; the amount of the increase will depend on the total mix of foreign securities held and their applicable foreign tax rates, as well as the amount of distributions from those securities.

We assume that losses are used to offset gains realized outside the account in the same month, and we add the imputed tax benefit of such a net loss to that month's return. This can inflate the value of the losses to the extent that there are no items outside the account against which they can be applied, and after-tax returns may exceed pre-tax returns as a result of an imputed tax benefit received upon realization of tax losses. Our after-tax performance calculation methodology uses the full value of harvested tax losses without regard to any future taxes that would be owed on a subsequent sale of any new investment purchased following the harvesting of a tax loss. That assumption may not be appropriate in all client situations but is appropriate where (1) the new investment is donated (and not sold) by the client as part of a charitable gift, (2) the client passes away and leaves the investment to heirs, (3) the client’s long-term capital gains rate is 0% when they start withdrawing assets and realizing gains, (4) harvested losses exceed the amount of gains for the life of the account, or (5) where the proceeds from the sale of the original investment sold to harvest the loss are not reinvested. It is important to understand that the value of tax-loss harvesting for any particular client can only be determined by fully examining a client’s investment and tax decisions for the life the account and the client, which our methodology does not attempt to do. Clients and potential clients should speak with their tax advisors for more information about how our tax-loss harvesting approach could provide value under their specific circumstances.

Information about composite returns.

The rates of return featured for accounts managed to a long-term asset allocation represent a composite of accounts managed with the same long-term asset allocation, investment approach and investment universe as applicable; rates of return featured for accounts managed with a single asset class strategy represent a composite of accounts managed to the applicable strategy. Accounts included in the composite utilize a time-weighted calculation, which vastly reduces the impact of cash flows. Composites are asset-weighted. An asset-weighted methodology takes into account the differing sizes of client accounts (i.e. considers accounts proportionately).

Larger accounts may, by percentage, pay lower investment advisory fees than smaller accounts, thereby decreasing the investment advisory fee applicable to the composite and increasing the composite’s net-of-fee performance. For tax-smart accounts in Fidelity Wealth Services, composite results are based on the returns of the managed portion of the accounts; assets in a liquidity sleeve are excluded from composite performance.

Composites set minimum eligibility criteria for inclusion. Accounts with less than one full calendar month of returns and accounts subject to significant investment restrictions are excluded from composites. Accounts with a do-not-trade restriction are removed from the composite once the restriction has been applied to the account for thirty days. For periods prior to October 1, 2022, composite inclusion required a minimum investment level that reflected product-relative investment requirements. Effective October 1, 2022, product composites will reflect all accounts for which we produce a rate of return and that meet the aforementioned criteria. Non-fee paying accounts, if included in composite, will increase the net-of-fee performance. Certain products, like Fidelity Go, offer investment services where accounts under a certain asset level do not incur investment advisory fees. Employees do not incur investment advisory fees for certain products.

Information about after-tax composite benchmarks. Return information for an after-tax benchmark represents an asset-weighted composite of clients' individual after-tax benchmark returns. Each client's personal after-tax benchmark is composed of mutual funds (index funds where available) and ETFs in the same asset class percentages as the client's investment strategy. The after-tax benchmark uses mutual funds and ETFs as investable alternatives to market indexes in order to provide a benchmark that takes into account the associated tax consequences of these investable alternatives. The after-tax benchmark returns implicitly take into account the net expense ratio of their component mutual funds because mutual funds report performance net of their expense. They assume reinvestment of dividends and capital gains, if applicable. The after-tax benchmark also takes into consideration the tax impact of rebalancing the benchmark portfolio, assuming the same tax rates as are applicable to each client's account, as well as an adjustment for the level of unrealized gains in each account. The after-tax composite benchmark return is calculated assuming the use of the "average cost-basis method" for calculating the tax basis of mutual fund shares.

Additional Information. Changes in laws and regulations may have a material impact on pre- and/or after-tax investment results. Strategic Advisers LLC relies on information provided by clients in an effort to provide tax-smart investing techniques. Strategic Advisers LLC can make no guarantees as to the effectiveness of the tax-smart investing techniques applied in serving to reduce or minimize a client's overall tax liabilities or as to the tax results that may be generated by a given transaction. Neither FPWA nor Strategic Advisers LLC provides tax or legal advice. Please consult your tax or legal professional for additional guidance. For more information about FPWA, Strategic Advisers LLC, or FPWA's advisory offerings, including information about fees and investment risks, please visit our website at Fidelity.com.

The information contained herein includes information obtained from sources believed to be reliable, but we do not warrant or guarantee the timeliness or accuracy of the information as it has not been independently verified. It is made available on an "as is" basis without warranty.

Stock markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments.

Fidelity® Wealth Services provides non-discretionary financial planning and discretionary investment management through one or more Personalized Portfolios accounts for a fee. Advisory services offered by Fidelity Personal and Workplace Advisors LLC (FPWA), a registered investment adviser. Discretionary portfolio management services provided by Strategic Advisers LLC (Strategic Advisers), a registered investment adviser. Brokerage services provided by Fidelity Brokerage Services LLC (FBS), and custodial and related services provided by National Financial Services LLC (NFS), each a member NYSE and SIPC. FPWA, Strategic Advisers, FBS, and NFS are Fidelity Investments companies.

Effective March 31, 2025, Fidelity Personal and Workplace Advisors LLC (FPWA) will merge into Strategic Advisers LLC (Strategic Advisers). Any services provided or benefits received by FPWA as described above will, as of March 31, 2025, be provided and/or received by Strategic Advisers. FPWA and Strategic Advisers are Fidelity Investments companies.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917