Fidelity traditional IRA

Make sure you have a Roth IRA to move your funds into—if you don't already have a Roth IRA, opening one is your first step.

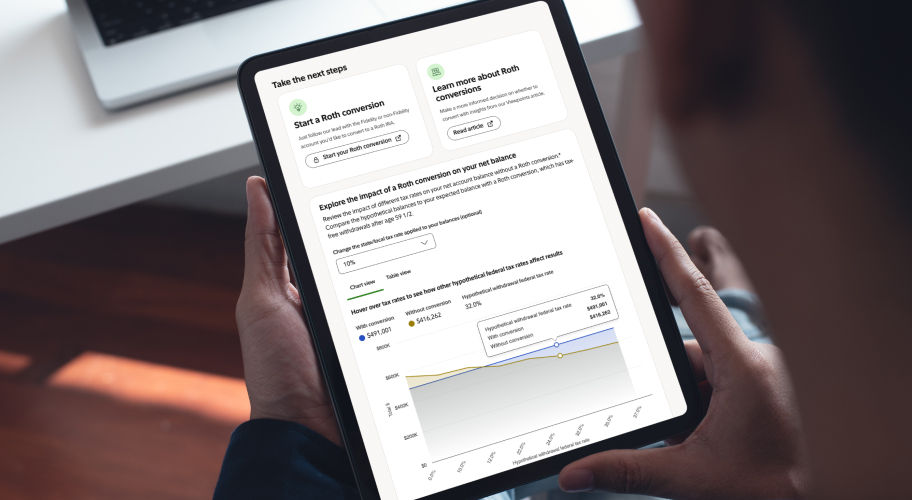

If you have a traditional IRA or an old workplace plan like a 401(k), you can convert those savings into a Roth IRA—we'll help you consider if a conversion may make sense for you.

Qualified withdrawals from a Roth IRA are tax-free1, helping you keep more of what you've set aside for retirement.

Since Roth IRAs don't require you to take withdrawals, your money can stay invested as long as you choose.

A Roth conversion can add a tax‑free income source to your mix, helping to give you more flexibility to manage taxes in retirement.

For many individuals, converting to a Roth IRA may make sense. However, you should consult with a tax advisor and consider these factors before making your decision.

For many individuals, converting to a Roth IRA may make sense. However, you should consult with a tax advisor and consider these factors before making your decision.

Use our Roth conversion calculator to help get an estimate of potential taxes you may owe on different conversion amounts today vs. potential savings down the road.

To begin, follow the steps for the type of retirement account you're converting.

Make sure you have a Roth IRA to move your funds into—if you don't already have a Roth IRA, opening one is your first step.

Start by opening and transferring assets to a Fidelity traditional IRA; then you can convert to a Roth IRA once your assets have arrived.

To convert an old workplace retirement account, like a 401(k), please call 800-343-3548.

Loading

Loading may take a few moments.

On this episode of Money Unscripted, host Ally Donnelly and Fidelity Market Leader Leanna Devinney explain the different conversion strategies and how taxes, timing, and your retirement plans can help you decide if one of these money moves is right for you.

Loading

Loading may take a few moments.

Learn if a conversion strategy may be a fit for you.

Consider this indirect strategy if you earn too much to contribute directly to a Roth IRA.

From investing to spending, a Fidelity advisor can help with every aspect of retirement planning.

We can help you find the answers.

Investing involves risk, including risk of loss.

Be sure to consider all your available options and the applicable fees and features of each before moving your retirement assets.

The images, graphs, tools, and videos are for illustrative purposes only.

1. For a distribution to be considered qualified, the 5-year aging requirement has to be satisfied, and you must be age 59½ or older or meet one of several exemptions (disability, qualified first-time home purchase, or death among them).

2. You are always able to take money from your SIMPLE IRA. Some withdrawals may be taxable, and some may be subject to a 10% early withdrawal penalty. SIMPLE IRA conversions before the age of 59½ are subject to a 10% early withdrawal penalty. If you are over 59½, you are not subject to a 10% early withdrawal penalty. Other exemptions may apply.

Fidelity does not provide legal or tax advice. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results. Fidelity cannot guarantee that the information herein is accurate, complete, or timely. Fidelity makes no warranties with regard to such information or results obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Consult an attorney or tax professional regarding your specific situation.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

1252880.2.0