If you’ve inherited an IRA recently, here’s something important to consider: The financial goals of the person who owned the account prior to you may have been very different from your own goals.

This is especially important now because new rules that went into effect in 2025 require many non-spouse beneficiaries to empty their inherited IRAs within 10 years. The combination of the 10-year window and the potentially different financial objectives of the original IRA owner mean it’s likely you may need to reconsider how to invest the money once it’s in an inherited IRA for you. Further, while married spouses who inherit an IRA are not subject to the 10-year rule and have several options for dealing with inherited funds, they may also have different financial needs than the original account owner.

Here’s something else to keep in mind. Inheriting money from a loved one—whether a grandparent, parent, or spouse—can be emotional, which might make you feel hesitant to make changes to the account. But once the assets are yours, it’s important to consider how the focus shifts to ensuring the account serves your own financial circumstances. This may mean reassessing the portfolio through the lens of your specific time horizon, tax situation, spending needs, and long-term financial goals.

How to invest an inherited IRA

Before you decide what to do with the inherited account, here are some general investing guidelines as well as several scenarios that might help guide your strategy for handling an inherited IRA.

Consider diversification and target asset mixes

Whether you’re investing the funds in your inherited IRA or in any other type of account, you’ll face a range of considerations and decisions along the way. A key part of successful investing is finding the right balance between your comfort with risk and your time horizon.

As you weigh these factors, it’s also important to think about diversification—the practice of spreading your investments across different types of assets so that no single holding carries too much weight. Diversification is designed to help reduce volatility in your portfolio over time and can support an investment approach that aligns with both your risk tolerance and your long-term goals. Remember, however, diversification and asset allocation do not ensure a profit or guarantee against loss.

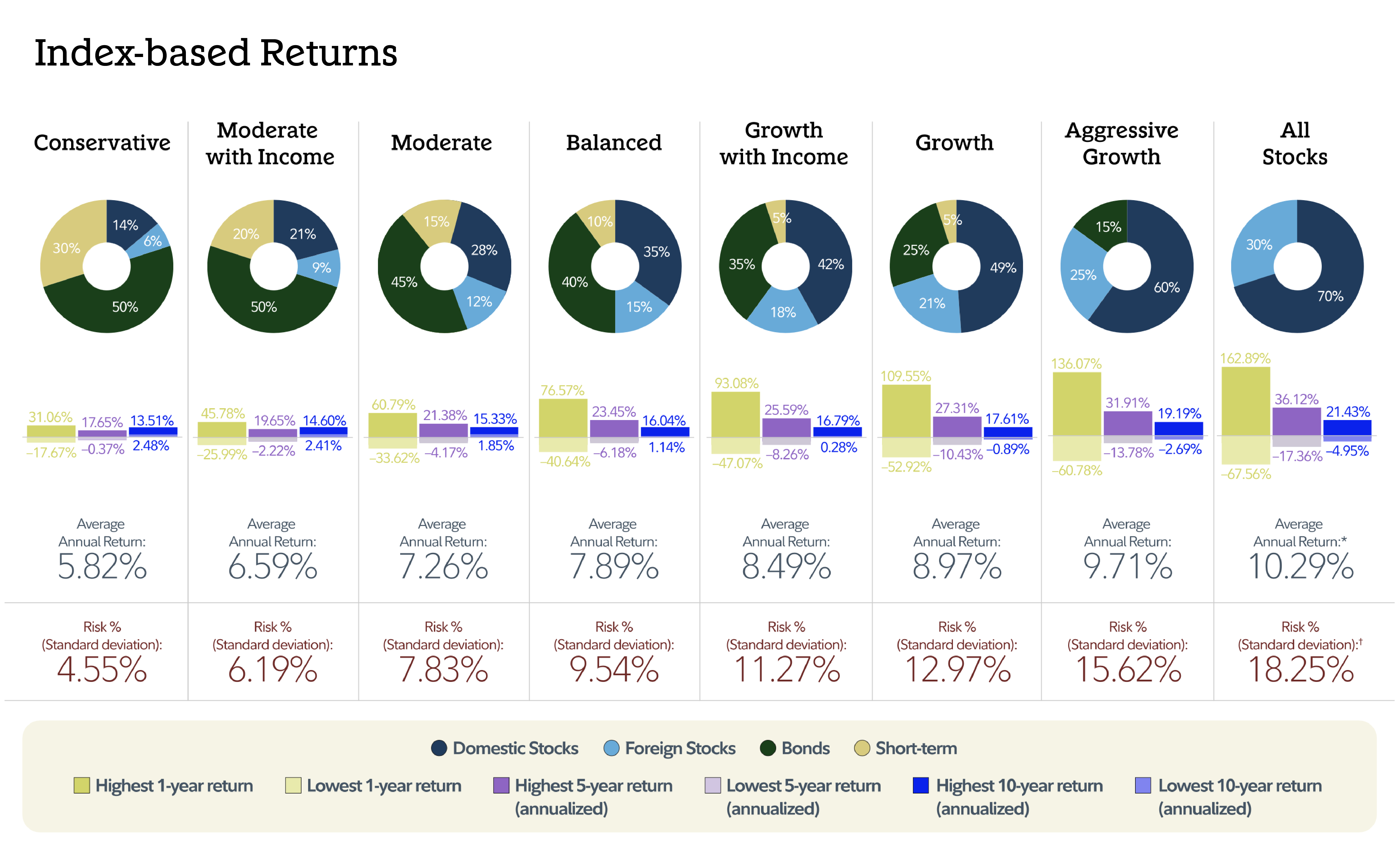

While there are numerous potential target asset mixes (TAMs) that might help you achieve your goals, for the purposes of this story we’ll consider 4 general ones of the 8 described in the chart below. These exist on a scale ranging from Conservative to Aggressive Growth. As you move along the scale, the percentage of stocks to bonds and short-term investments increases, which may be suitable for the different time horizons we discuss related to inherited IRA withdrawals, as well as how you plan to withdraw from the accounts. Increasing the percentage of stocks increases the potential return, but it also may increase the potential for loss and price fluctuations of your investments, especially over the short term

Data source: Fidelity Investments and Morningstar Inc, 2025 (1926-2024). Past performance is no guarantee of future results. Returns include the reinvestment of dividends and other earnings. This chart is for illustrative purposes only. It is not possible to invest directly in an index. Time periods for best and worst returns are based on calendar year. Standard deviation is a statistical measure of how much a return varies over an extended period of time. The more variable the returns, the larger the standard deviation. Investors may examine historical standard deviation in conjunction with historical returns to decide whether an investment's volatility would have been acceptable given the returns it would have produced. A higher standard deviation indicates a wider dispersion of past returns and thus greater historical volatility. Standard deviation does not indicate how an investment actually performed, but does indicate the volatility of its returns over time. Standard deviation is annualized. The returns used for this calculation are not load adjusted. For information on the indexes used to construct this table, see Data Source in the notes below.1

Keep your individual financial circumstances in focus

Your asset allocation should always take into consideration your financial situation and risk tolerance. In the event of a potential major event like inheriting assets, consider the impact this has on your capacity and willingness to bear risk. For example, if you have a low risk tolerance or are less financially secure—or both—you may want to invest more conservatively to ensure access to funds when you may need them. Similarly, if you plan to take withdrawals immediately and over an extended period of years, especially if you have high withdrawal needs, your financial situation may not support an aggressive, or growth, investment approach because you might need to withdraw funds sooner than you expect.

| Hypothetical inherited IRA withdrawals and sample target asset mixes | ||

|---|---|---|

| Planned inherited IRA withdrawal time frame | Risk-averse investor | Investor comfortable with taking risk |

| A lump-sum withdrawal in year 10 to be spent on expense needs | 50% stocks– Balanced TAM | 70% stocks– Growth TAM |

| Regular required minimum distributions (RMDs) years 1–9 and a full withdrawal in year 10 to be spent on expense needs | 30% stocks– Moderate with Income TAM | 60% stocks– Growth with income TAM |

| Larger withdrawal need / lump sum withdrawal within 3 years to be spent on expense needs | 0% stocks– Short-term (cash and short duration fixed income) | 0% stocks– Short-term (cash and short duration fixed income) |

| Withdrawals taken over an inheritor's lifetime with withdrawals reinvested into a taxable account for retirement rather than spent | 50% stocks– Balanced TAM | 85% stocks– Aggressive Growth |

Source: Fidelity. The purpose of the target asset mixes is to show how target asset mixes may be created with different risk and return characteristics to help meet an investor’s goals. You should choose your own investments based on your particular objectives and situation. Be sure to review your decisions periodically to make sure they are still consistent with your goals.2

When thinking about your time horizon, consider how you plan to use the money after it is withdrawn from the IRA. The first 3 examples below assume you plan to use the RMD for spending such as living expenses or some other short-term need. If you plan to reinvest the money and put it toward one of your longer-term financial goals, the time horizon for achieving that goal would help determine the appropriate asset allocation. For example, if you have a longer time frame such as for retirement, you could consider a more Aggressive Growth strategy.

It’s also a good idea to consider consulting with a financial or tax professional for guidance.

Examples of how to invest an inherited IRA

1. A lump-sum withdrawal in year 10

If you don’t have an immediate need for the money and don’t plan to take required minimum distributions (RMDs) in years 1 through 9, your risk tolerance can help guide how you invest in the account. If you are more risk averse you could consider a lower-risk asset allocation, such as a Conservative, Moderate, or Balanced mix. If you are more comfortable with risk, a more growth-oriented allocation, such as a Growth or even Aggressive Growth mix may make sense. Keep in mind as time passes and you get closer to year 10, you may want to consider reducing the risk of your portfolio’s asset allocation, particularly if your intention is to use the funds for spending and expenses rather than reinvesting it for the long term. Remember also that you will need to take a lump-sum distribution in year 10, which could have important tax implications.

2. Regular RMDs over the first 9 years and then a full withdrawal in year 10

If you’re required to take RMDs in years 1 through 9 or you will need to take a lump-sum distribution of the entire amount within a few years, you may have to balance short- and medium-term needs for cash. This might call for a more conservative portfolio allocation if you are risk averse, since you’ll be selling assets each year to meet withdrawal requirements. If there is a market downturn and you have a more aggressive allocation during a market downturn, your portfolio might not have enough time to recover before you sell assets at lower prices to cover your withdrawal needs. If you are more comfortable with risk, you could consider adding more stock exposure to offer a little more growth potential.

3. Larger RMDs or a lump-sum withdrawal within 3 years

If you plan to withdraw your account balance in a short time frame, for example 3 years or less, then preserving your principal and ensuring liquidity are likely to be top priorities. With a short time horizon, you may want to invest your assets more conservatively, focusing on short-term investments, which could be less volatile and not subject to the short-term risks of stocks.

4. RMDs over an inheritor’s lifetime

There are specific rules that determine when you may take RMDs over your own lifetime, rather than within a 10-year period. People who may be able to take these extended RMDs generally fall into 3 categories: spouses, designated eligible beneficiaries, or beneficiaries who inherited prior to 2020.

If you qualify to take withdrawals over your lifetime, you potentially have a longer period to make withdrawals and remain invested. With this longer investment horizon, you may prefer a Moderate or Balanced asset mix since it could help smooth out any market volatility. However, you may also decide the extra time could lend itself to an allocation containing more stocks, since you will have more time to ride out potential market volatility.

In either case, your asset allocation should also consider when you plan to start taking your withdrawals. For example, if you have an aggressive portfolio and you begin withdrawals during a market downturn, you may be selling more positions than when the market is up, and your balance might be depleted faster as more investments are sold to cover withdrawals. If, however, you plan to take your RMD and reinvest it toward a long-term goal with a longer time horizon, that may justify a more aggressive allocation if you’re comfortable with risk.

Aligning investments with RMDs

You’ll also want to look at what you’re invested in, because that can affect how easily you can access your money. Some investments such as mutual funds, stocks, and ETFs are generally liquid and easy to sell. Others, however, may be less liquid and difficult to sell quickly. For example, long-term maturity fixed income investments or products that have lockup periods, such as certain alternative investments, may pose challenges when you need cash to meet your RMD. That could mean you may need to sell other more liquid holdings instead, which could be a problem if you need to sell when market conditions are less favorable. It could also disrupt your planned asset allocation if you must sell more liquid assets first. Note: As an alternative, the position could also be moved in-kind, although this may pose some technical challenges and not all assets can be moved in this manner. Consider speaking with a financial professional for help.

Asset location

Once you’ve settled on the mix of investments you want to hold, it’s also important to think about where you hold them, since inheriting an IRA may mean you now have more assets than you did previously.

The process of determining the types of accounts to hold your funds is called asset location, which typically refers to putting certain types of investments in the accounts where they make the most sense from a tax perspective.

Generally speaking:

- Investments that create more taxable income each year might be better kept in a tax-advantaged account, such as a Roth IRA or a traditional IRA.

- Investments that are more tax-efficient can go into a taxable account, such as a brokerage account.

Because your portfolio likely already includes similar assets, the new holdings can typically be integrated into your existing asset‑location framework by placing them in the accounts that best align with their tax characteristics. However, when anyone attempts to allocate asset types across different account types to manage the effect of taxes on your portfolio, it's important you do not lose sight of your overall asset allocation across those accounts and make investment decisions accordingly. You should also understand that each of those accounts will likely perform differently over time.

Are inherited IRAs taxable?

Yes, distributions from a non-Roth inherited IRA are generally considered ordinary income and subject to federal and state tax for the year in which they occur. An exception would be for after-tax contributions to the inherited IRA. Once applicable taxes are paid, a distribution can be deposited into a checking or savings account and used at your discretion, or it can go into a brokerage account where you allocate funds into investments of your choosing.

The bottom line on investing inherited IRAs

Ultimately, the right investment mix for an inherited IRA depends on your financial goals and withdrawal time frame. A shorter time horizon may call for more conservative and liquid holdings, while a longer horizon may allow for more growth-focused investments, potentially including investments that may be less liquid. Since withdrawals from an inherited IRA can affect your taxes and both your short- and long-term financial goals, working with a financial and tax advisor can help ensure you make decisions aligned with your needs as well as IRS requirements.