While stock markets have broadly moved lower on the Iran conflict, commodities ranging from energy and metals to beans and livestock have been volatile. Here’s what’s happening in gold, oil, and other commodity markets.

Gold prices drop

Going into 2026, the momentum behind gold prices appeared to have no end in sight. But the yellow metal had its worst week in 15 years last week, losing nearly 10%, and is now down more than 20% since the January all-time high near $5,600 per ounce.

The drivers of trading action this year for gold and other metals have been multifaceted. Some investors view precious metals like gold and silver to be safe-haven assets: When market risks are rising, they think these real assets will hold their value better than financial assets like stocks. Gold initially moved higher at the outset of the Iran conflict, but fears of a broader economic downturn and a potential decline in demand for raw materials have hindered metal prices as well as metal mining stocks—the latter of which are also dealing with rising energy costs (mining is an energy-intensive process).

Additionally, dollar strength thus far this year has dulled the luster of some precious metals (when the dollar appreciates, gold tends to decline, and vice versa). The US Dollar Index is up 1% year to date.

Despite the recent haircut, it’s important to remember that gold—which is currently trading around $4,400—is still nearly 2% in the green for the year after gaining 64% in 2025. Silver—which is down sharply from its January 2026 all-time and recently turned red year to date—exploded by more than 125% in 2025.

As some precious metal prices have had their momentum stunted recently, other metals have firmed. Aluminum, which is the most abundant metal on earth and is a key input for things like electronics, buildings, and packaging, is trading near a 4-year high, as of late March. Even though most of the world’s aluminum supply comes from China, the tensions in the Middle East have led to supply chain disruptions for this base metal, thereby pushing the price higher.

Steel is another industrial metal that's been impacted by world events. It’s heated up going on 7 months, and that rally has accelerated in recent weeks on supply constraints. Hot-rolled coil steel recently crossed $1,000 per ton for the first time since January 2024.

Over the near term, metal prices may continue to be significantly impacted by geopolitical factors, in addition to currency rate changes, inflation, central bank moves, and global demand.

Oil prices up

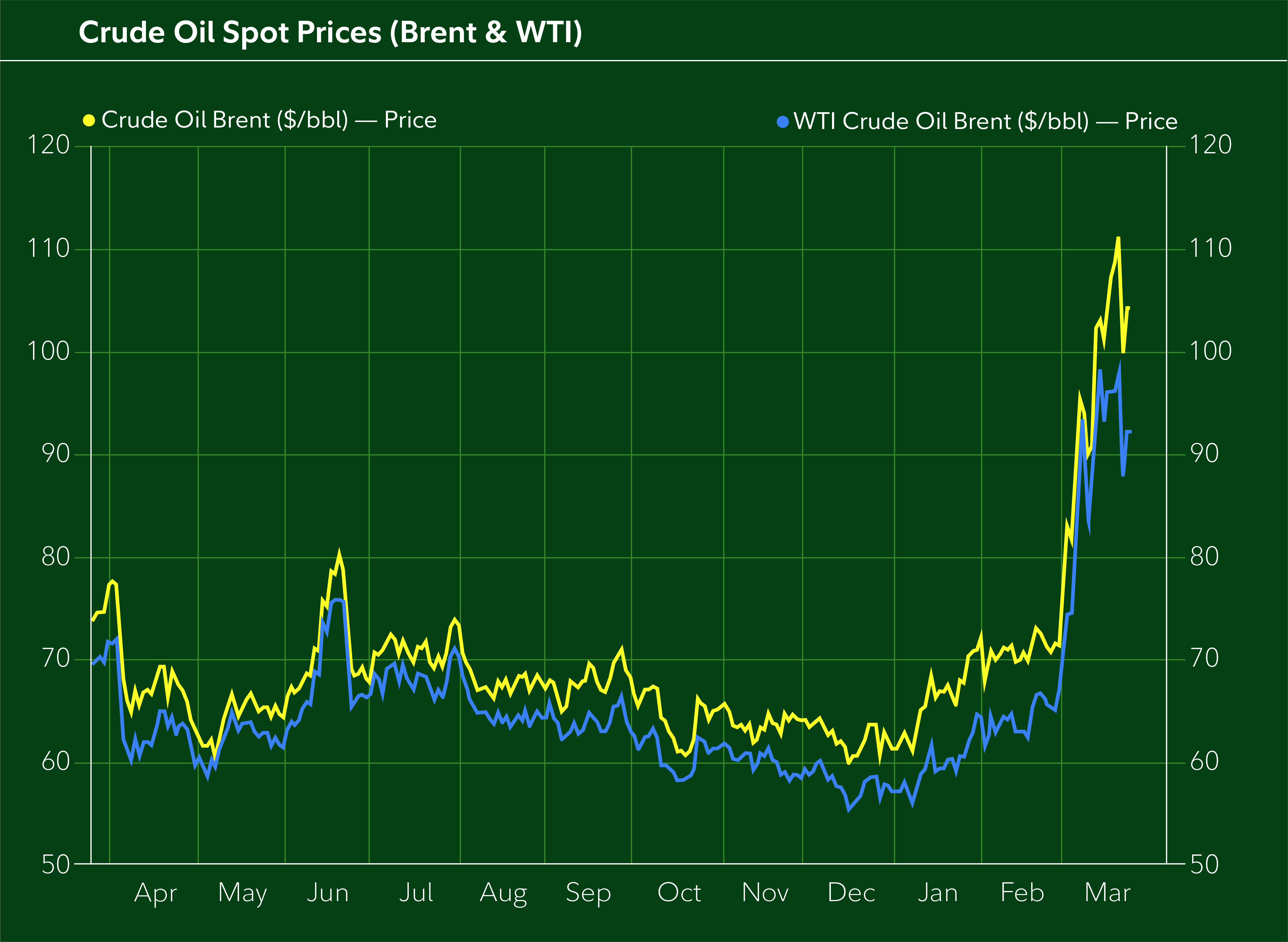

No part of the market has been more directly impacted by events in the Middle East than oil prices. At the start of 2026, West Texas Intermediate Crude—which is a light, sweet crude primarily produced in the United States and is used as the crude benchmark in the Americas—traded near $57 per barrel. It has since reached as high as over $98. Brent Crude, which is transported from the North Sea and is widely used as the global benchmark for oil pricing, surpassed $110 per barrel at its highest point this year.

Hopes that the conflict may come to a peaceful end soon—plus remediation efforts to address the bottleneck in the Strait of Hormuz, including the release of strategic reserves—have helped keep oil prices from exploding well above $100. On March 11, member nations of the International Energy Agency agreed to release a record 400 million barrels of oil from strategic reserves.

An end to the conflict might result in a rapid decline in oil prices, although even in such a scenario, it may take more time for energy costs for businesses and consumers to decrease. Of course, a prolonged or expanding conflict could continue to push prices higher.

Investors should prepare for the possibility of a new normal for this market. “I think we could continue to see volatility in oil markets in this new era of geopolitical risk,” notes Jake Weinstein, senior vice president in Fidelity’s Asset Allocation Research Team. And given the ubiquitous impact of energy prices on nearly all segments of the market, that could mean stocks may remain particularly sensitive to changes in oil prices over the near term.

Soybean, coffee bean, beef prices

Another part of the commodity space that is impacting markets is agriculture and livestock, as food costs are a key part of the inflation story.

This time last year, soybeans were under pressure amid tariff disputes between the US and China. Now, soybean prices are being driven higher in part by recent geopolitical events. The conflict in the Middle East has exacerbated tight conditions for soybean supply, pushing prices to year-to-date highs as production costs soar.

As with other commodities, a peaceful resolution could have a big impact on soybean prices going forward. The Hightower Report’s March 23 daily grain market commentary (available on Fidelity.com, login required) notes that, “…for now, the bulls retain the edge. However, if negotiations [result in an end to the conflict] and energy prices sink sharply, bean oil could see a significant pullback and pull beans lower in the near term as well.”

Of course, not all aspects of the commodity market are affected by current geopolitical conflicts. Coffee prices, for example, are near multi-month lows due to better-than-expected harvests, favorable growing conditions, and some demand destruction from all-time high prices set in 2025.

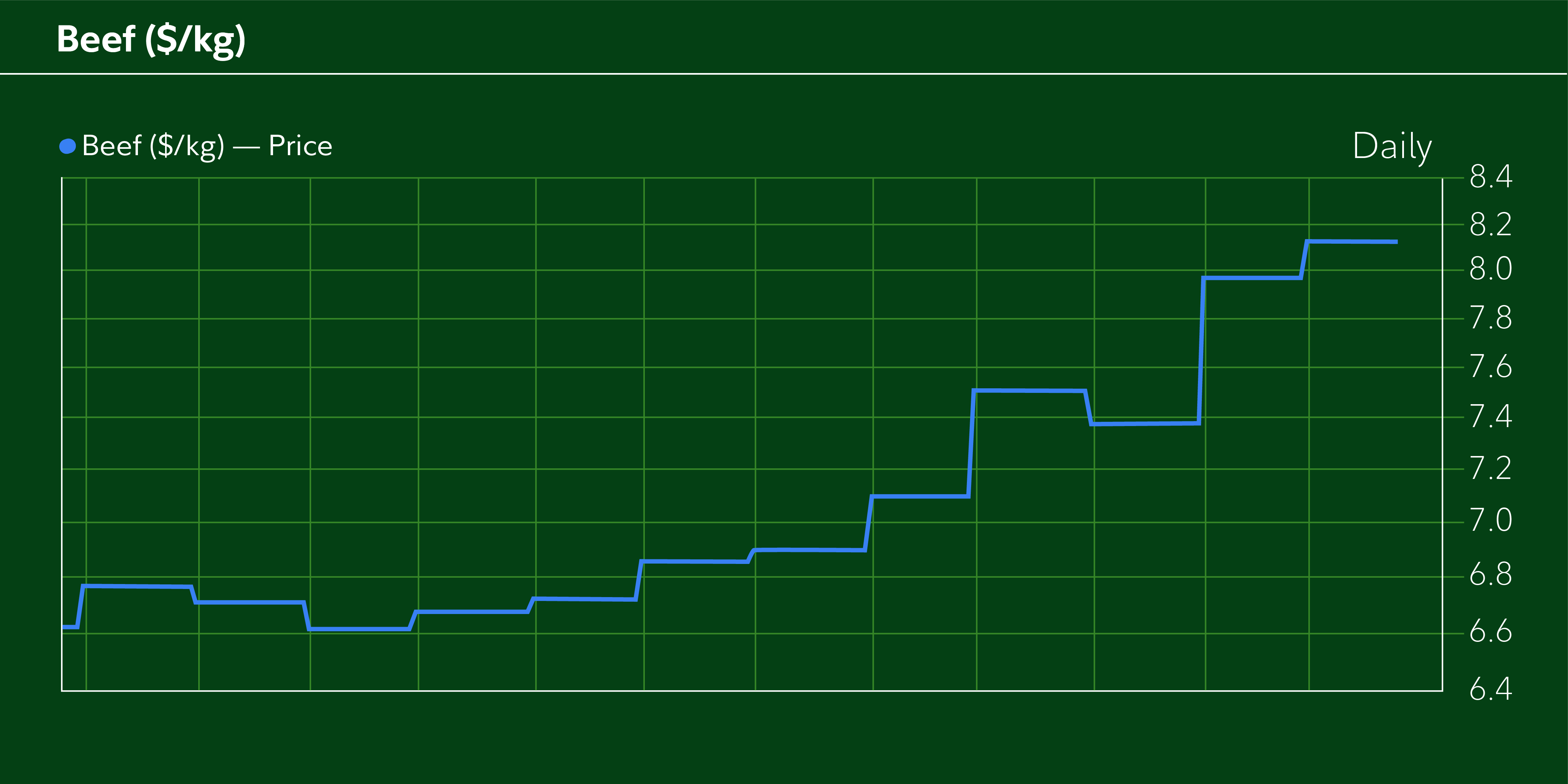

And beef prices continue to hover near all-time highs as global demand outstrips supply. The Hightower Report’s March 23 daily livestock commentary (which you can find on Fidelity.com, login required) noted that beef production last week was 455.3 million pounds, down from 484.6 million pounds a year ago. Smaller herd sizes (2025 saw the smallest national herd size since 1951), higher feed prices (the American Farm Bureau Federation reports that input costs are up more than 50% for American ranchers over the past 5 years), and growing global demand have led to sticker shock for many grocery shoppers.