For decades, $1 million has been the magic number for retirement. It feels like a milestone—a round figure that signals financial security. But expectations can be even higher: Americans in a recent Fidelity survey said they expect to have saved around $1.4 million to retire. Retirees, however, report having closer to $490,000.1 So is $1 million enough?

Why $1 million may not be the right number

Even though $1 million is a lot of money, it may not be enough to retire on—or it may be more than you need.

“That’s the challenge in financial planning: It all depends,” says Kenny Davin, CFP®, vice president and branch leader in Fort Lauderdale, Florida. “Some people absolutely can make a million dollars last. Others with $3–$5 million still struggle because they spend a lot or have significant obligations, like supporting family members. It’s all about the specifics.”

Key variables include:

- Lifestyle

- Retirement age

- Whether you enter retirement with a mortgage

- Your health and expected medical costs

Lifestyle helps determine annual spending. Someone with an above-average lifestyle might enjoy several trips each year and spend more than someone with a below-average lifestyle. Retirement age determines how long that spending must last. Those are 2 of the biggest factors—but far from the only ones.

But retirement timing is often more uncertain than people expect. Most Americans plan to retire around age 62, but nearly 1 in 4 say they aren’t sure when they’ll retire, and 6% say they may never stop working, according to Fidelity’s survey.1 That uncertainty affects how long your money needs to last—one of the biggest risks retirees face, but not the only one.

The 5 big risks that shape retirement

“You can’t assume anything based on account size alone. Instead of giving blanket answers, I try to ask the right questions,” Davin says. Those questions often fall into 5 essential categories.

1. Longevity: How long does your money need to last?

Living longer is a gift—but it stretches your finances. Depending on your health and family history, it may make sense to plan for a retirement that lasts well into your 90s.

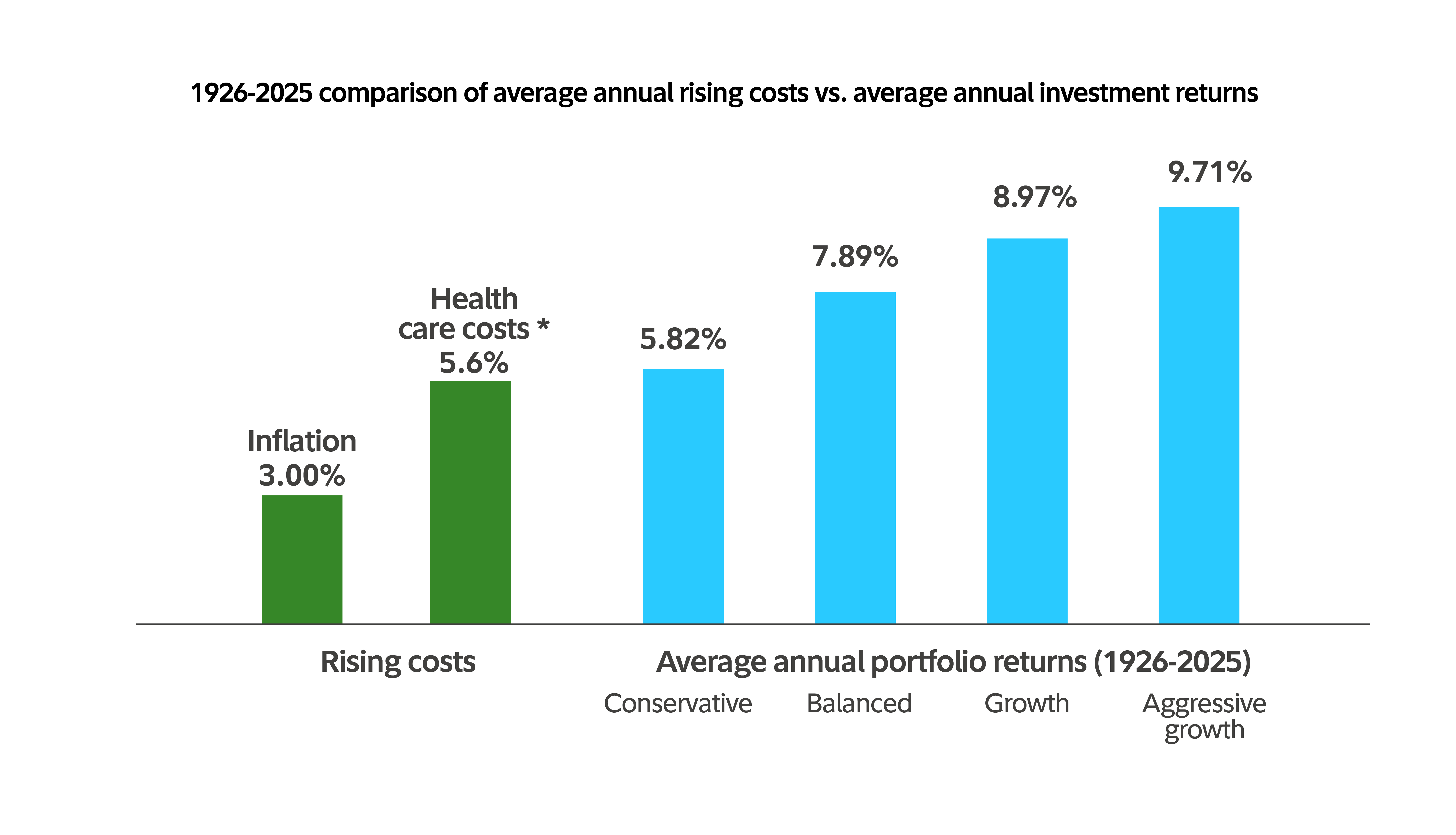

2. Inflation: Can your savings keep up with rising prices?

After several years of elevated inflation, more than a third of Americans (37%) say rising prices are one of the biggest challenges in preparing for retirement, according to Fidelity’s survey.1 That concern is well founded—higher prices can stretch budgets and increase the amount your savings must cover over time.

3. Health care costs: Medicare? Retiree benefits? Paying out of pocket?

Health care is one of the biggest unknowns in retirement.

A person retiring in 2025 may need $172,500, on average, in after-tax savings to cover health care in retirement.2 That excludes long-term care, which can dramatically increase costs if not insured. Watch or listen to Money Unscripted: What is long-term care insurance?

Most Americans become eligible for Medicare at age 65, but retirees still face premiums, cost-sharing, prescription costs, and potential long-term care needs. Read Fidelity Viewpoints: How to plan for rising health care costs

4. Withdrawal rate: Is it sustainable?

A sustainable withdrawal rate is often estimated at 4% to 5%, with annual inflation adjustments—assuming a typical 30-year retirement.

“If you withdraw 4% from $1 million, that’s $40,000 a year,” Davin explains. “Is that enough? Maybe—if you have a pension or other income. But if you need more than that, you may shorten the sustainability of your savings.”

Fidelity suggests that people planning very long retirements—such as early retirees—consider lower withdrawal rates, around 3%. Read Fidelity Viewpoints: How to retire early in 8 steps

5. Investments: Are you positioned for growth potential?

Guaranteed income sources—pensions, Social Security, annuities—can provide a stable foundation. Fidelity generally suggests covering essential expenses with guaranteed income and using portfolio withdrawals for discretionary spending. Read Fidelity Viewpoints: Understanding annuities

“Sometimes you take part of that million and put it toward something guaranteed that covers essential expenses, so you’re not relying on the market for necessities,” Davin says. “The rest can stay invested for long-term growth or discretionary spending.”

This balance can provide confidence and reduce the risk of outliving your money.

Behavior matters too. “Some of our best savers become our most hesitant spenders because they’re afraid to draw down their accounts,” Davin adds. “Having a plan—automated withdrawals, professional management—helps a lot.”

The difference a plan can make

A good retirement plan pulls together everything that influences your financial life: how you spend, how you save, how you invest, the risks you face, and the timeline you’re working with. All of it helps define what “enough” means for you.

A financial plan—created on your own or with a professional—can help you see what it may take to reach the lifestyle you want, whether retirement is near or still years away.

“Personal finance is more personal than financial. It’s both an art and a science,” Davin says. “The science shows where you are; the art is what you’re willing to do.”

And sometimes the numbers can be discouraging. Planning tools may show a shortfall even when you’re doing everything right—that can be useful feedback, not a moral judgment. “It’s better to know you have a shortfall and do something about it than be surprised later,” Davin says. “Scenario planning gives you the chance to adjust spending, work longer, invest smarter.”

Planning can also reduce the stress that comes with uncertainty. Among retirees who worry about running out of money, 69% say they cut spending, 32% look for work, and 18% lean on home equity, according to Fidelity’s survey.1 Having a plan in place can help you evaluate strategies proactively rather than reactively.

Getting on track

If your plan points to a potential gap, focus on the levers you can control.

Adjust spending to prioritize essentials and trim what matters less.

Work longer or add part-time income to reduce the years your savings must cover.

Invest appropriately so your portfolio balances near-term needs with long-term growth.

Add guaranteed income (from sources like Social Security, pensions, or annuities) to help cover essentials with more certainty.

Read Fidelity Viewpoints: Test-drive your investment strategy

Make $1 million—or whatever you have—work for you

Once you understand where you stand, the next step is shaping a plan that helps your savings go further. You don’t need a perfect number to move forward—you just need a framework that supports the lifestyle you want and adapts as life changes. Here are a few ways to help strengthen any retirement plan:

1. Map your must haves vs. nice to haves

Cover essential expenses—housing, food, utilities, health care—with guaranteed income where possible. Use your investments for discretionary or flexible spending.

2. Segment your savings by purpose: emergency, protection, and growth

- Emergency savings for unexpected expenses.

- Protection strategies, including insurance or income protection strategies to help safeguard what you’ve built. Learn more about Retirement income strategies

- Growth potential to help your money keep up with inflation over time. The key is to strike a comfortable balance between the level of stock market risk you can live with and the long-term growth potential you may need to keep your plan on track.

3. Right size your withdrawal strategy

Start conservatively and adjust as needed. The right withdrawal rate depends on your timeline, market conditions, and other income sources.

4. Plan explicitly for health care

Health care is often one of the largest and most unpredictable expenses in retirement. Pricing out Medicare options, estimating out-of-pocket costs, and considering long-term care coverage ahead of time can help avoid surprise strain on your budget.

5. Rehearse “what ifs” regularly

Running scenarios, for instance, cutting spending, delaying retirement, adding part-time income, or planning for higher inflation, can help your plan stay nimble.

The goal isn’t to predict the future perfectly—it’s to be prepared for a range of possibilities.

$1 million can be enough—with a plan

So is $1 million enough to retire? It depends—on your lifestyle, goals, and willingness to plan. Reaching $1 million is an incredible milestone worth celebrating, but the number alone doesn’t guarantee retirement success. What matters more is how you structure your spending and income, manage risks, and stay flexible as life unfolds.

The good news: Many of the biggest drivers of retirement readiness are within your control. Tools, guidance, and scenario planning can help you make the most of whatever you’ve saved—and adjust early if something needs to change.

“$1 million is just a number,” Davin says. “It all comes back to lifestyle. You can technically retire anytime as long as you can pay your bills.”

A thoughtful plan can help get you there—whether your number is $1 million or something very different.