Required minimum distributions (RMDs)

Once you reach age 73, the IRS requires you to take annual withdrawals from your tax-deferred IRAs. Find out how RMD rules work and the potential penalties for missing a withdrawal.

Your IRA savings is yours when you need it—whether for retirement income or emergency funds. We’ll help you understand how your age and other factors affect the way the IRS treats your withdrawal.

The IRS considers withdrawals taken at age 59½ or older as normal, while those taken before 59½ are considered early. Depending on your age and the type of IRA you own, taxes and penalties may apply.

A Roth IRA allows you to withdraw your contributions at any time—for any reason—without penalty or taxes. Better yet, if you’re age 59 ½ or older, and you made your first contribution to a Roth IRA at least 5 years ago, you may be able to take a tax free withdrawal of both contributions and earnings from your account.

A Roth IRA allows you to withdraw your contributions at any time—for any reason—without penalty or taxes. Better yet, if you’re age 59 ½ or older, and you made your first contribution to a Roth IRA at least 5 years ago, you may be able to take a tax free withdrawal of both contributions and earnings from your account.

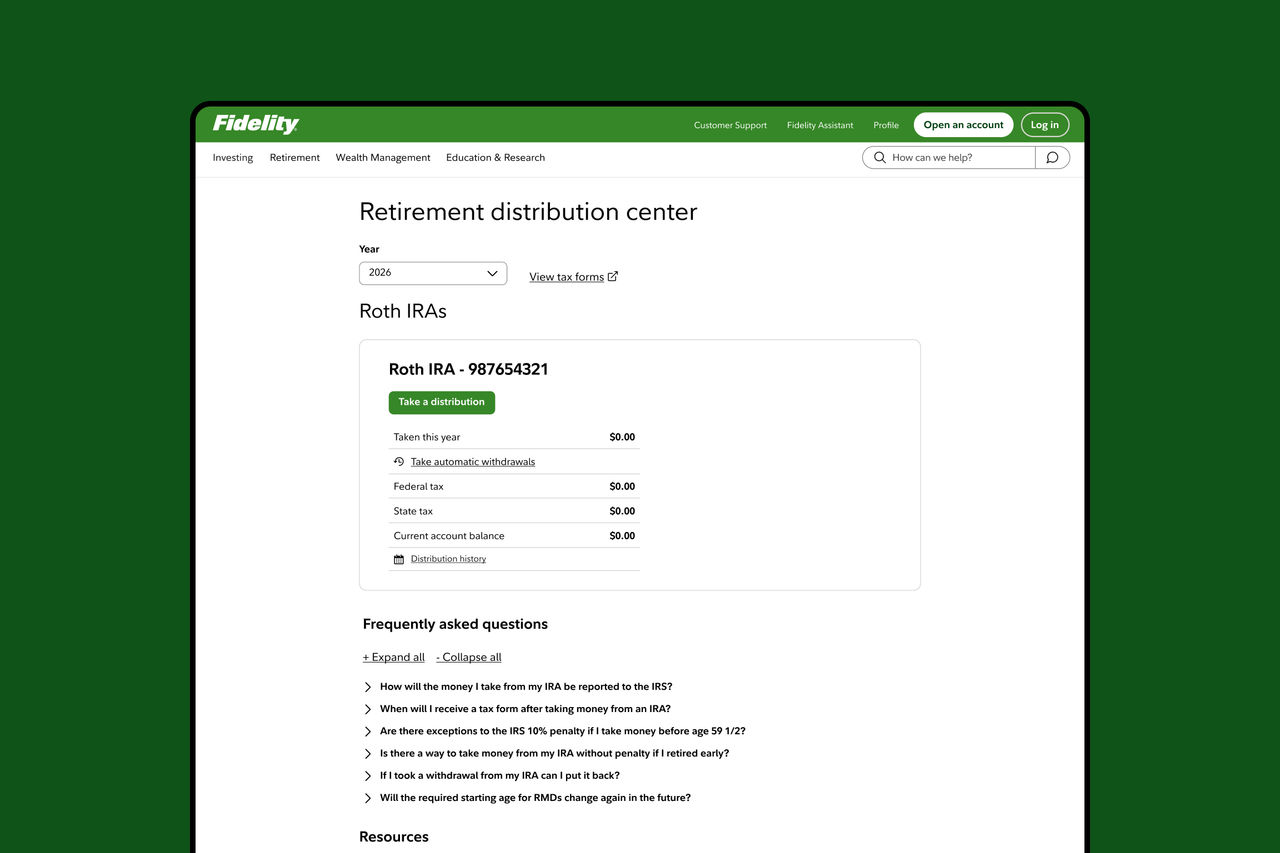

To initiate a withdrawal, you’ll need to fill out and submit a form or call us for assistance at 800-343-3548.

IRAs are subject to IRS rules for required withdrawals, but the rules can differ if the account is inherited. Get clarity on how the requirements work and how much you may need to take.

Once you reach age 73, the IRS requires you to take annual withdrawals from your tax-deferred IRAs. Find out how RMD rules work and the potential penalties for missing a withdrawal.

Inheriting retirement savings can come with IRS withdrawal requirements that vary by your relationship to the original account owner. We can help you understand what may apply to your situation.

Facing a sudden cash emergency? Consider tapping these sources first.

Consider a simple strategy to help reduce taxes on retirement income.

We can help you find the answers.

Investing involves risk, including risk of loss.

Screenshots are for illustrative purposes only.

Fidelity does not provide legal or tax advice. The information herein is general in nature and should not be considered legal or tax advice. Consult an attorney or tax professional regarding your specific situation.

For a distribution to be considered qualified, the 5-year aging requirement has to be satisfied, and you must be age 59½ or older or meet one of several exemptions (disability, qualified first-time home purchase, or death among them).

A distribution from a Traditional IRA is penalty-free provided certain conditions or circumstances are applicable: age 59 1/2; qualified first-time homebuyer (up to $10,000); birth or adoption expense (up to $5,000 per child); emergency expense (up to $1000 per calendar year); qualified higher education expenses; death, terminal illness or disability; health insurance premiums (if you are unemployed); some unreimbursed medical expenses; domestic abuse (up to $10,000); substantially equal period payments; Qualified Federally Declared Disaster Distributions or tax levy.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

1262828.1.0