Fidelity® Limited Duration Municipal StrategyA separately managed account investing in investment-grade municipal bonds, which seeks to deliver interest income exempt from federal income taxes while balancing risk and return. This actively managed strategy looks to maintain an average target duration1 of 2 to 3 years. |

Investment objective: Seeks to generate federally tax-exempt interest income, while working to limit risk to principal over a full market cycle.

Types of investments: Primarily A- or higher investment-grade2 municipal bonds at time of purchase.

Investment minimum: $250,0003

Eligible Registration Types: Taxable only

Gross annual advisory fee: 0.35% – 0.40%4 (varies based on total assets invested)

Actively managed municipal bond strategy backed by deep research

- Designed to help you pursue tax-efficient interest income with confidence

Built for investors seeking a professionally managed limited duration municipal bond portfolio with a high overall credit profile—targeting an average credit rating of A- or better and investing only in bonds rated BBB- or higher at the time of purchase—while aiming to deliver federally tax-exempt interest income. The Strategy also maintains a disciplined focus on diversification and risk awareness.

- Active oversight to help navigate evolving market conditions

Active management provides the investment team with the flexibility to make timely adjustments as market conditions change—including the ability to buy or sell bonds before maturity—seeking to identify opportunities and manage risk in support of the strategy’s objectives.

- Research depth that powers informed investment decisions

Every bond added to the portfolio is evaluated through Fidelity’s robust fixed income research platform— bringing together analysts, portfolio managers, and credit specialists to help uncover opportunities others may miss.

- Tax management through direct ownership

By owning individual municipal bonds directly, the strategy can employ tax-smart techniques5—such as tax-loss harvesting when appropriate—to help support after-tax efficiency.

- Opportunity for returns from both income and price movement

The strategy looks to both consistent income and potential price appreciation as drivers of return, focusing on bonds that the investment team believes offer a favorable balance of opportunity and risk.

About the strategy

Pursue federally tax-exempt interest income through high-quality limited-term municipal bonds

- Target average rating: Primarily A- or higher

- Minimum credit quality: Bonds rated BBB- or better at purchase. No more than 20% of the account may be invested in bonds rated below A- at purchase.

- Average target duration: 2 to 3 years

- Maturities: Bonds generally maturing within 10 years

- Number of holdings: Typically, 30—80 individual bonds‡

‡ Number of portfolio holdings dependent on overall portfolio size.

Expected range of credit quality of the bonds in your SMA

Investment-grade municipal bonds typically offer relatively low default rates†

10-year average cumulative default rates (1970-2023)

| Moody's rating category6 | Municipal bonds | Global corporate bonds | |

|---|---|---|---|

| Investment

Grade |

Aaa | 0.00% | 0.36% |

| Aa | 0.02% | 0.77% | |

| A | 0.10% | 2.03% | |

| Baa | 1.09% | 3.61% | |

| Non-Investment

Grade |

Ba | 3.49% | 15.25% |

| B | 17.07% | 34.31% | |

| Caa-C | 25.59% | 51.44% |

†Source: Moody’s Investor Service “US Municipal Bond Defaults and Recoveries, 1970-2023, October 24,2024

Broad diversification across the municipal market

The strategy invests in a diversified mix of municipal bonds issued by U.S. states, cities, counties, and public and nonprofit organizations. This broad opportunity set allows the portfolio to access a wide range of credit profiles, projects, and local economies. By incorporating multiple sectors and varying maturities, the strategy seeks to reduce reliance on any single issuer type or region.

Flexibility to invest nationally or prioritize potential state tax benefits

National portfolio option

The national portfolio can hold bonds issued within any of the 50 states or U.S. territories, offering broad diversification and income potential.

State-preference option

If you reside in California, Massachusetts, or New York, you may choose the state-preference option. With this approach, the investment team will seek to emphasize in-state municipal bonds to help pursue state-specific tax-exempt interest income. Target exposure levels include:

- California: seeks to achieve at least 70% in-state municipal bond exposure

- New York: seeks to achieve at least 70% in-state municipal bond exposure

- Massachusetts: seeks to achieve at least 60% in-state municipal bond exposure

This option places less emphasis on national diversification

Actual in-state allocations will vary over time based on market conditions, bond availability, and broader economic factors, and cannot be guaranteed (and may fall significantly below the stated targets). When appropriate, the investment team may include or increase exposure to national municipal bonds to support prudent portfolio construction and maintain diversification.

Tapping Fidelity's Fixed Income expertise

Strategic Advisers LLC (Strategic Advisers), has engaged Fidelity Management & Research Company LLC (FMR), a registered investment adviser and a Fidelity Investments company, to provide the day-to-day discretionary portfolio management of Fidelity Limited Duration Municipal Strategy accounts, including investment selection and trade execution, subject to Strategic Advisers’ oversight.

FMR brings investors a rich history of managing fixed income investments for over 50 years.

This capability allows them to:

- Build a diversified limited duration municipal bond strategy

- Support income generation

- Balance risk and return potential

- Help keep your account aligned with your preferences Fidelity

- Apply a disciplined tax-loss harvesting process, when appropriate, to help enhance after-tax efficiency while maintaining the strategy's objectives.

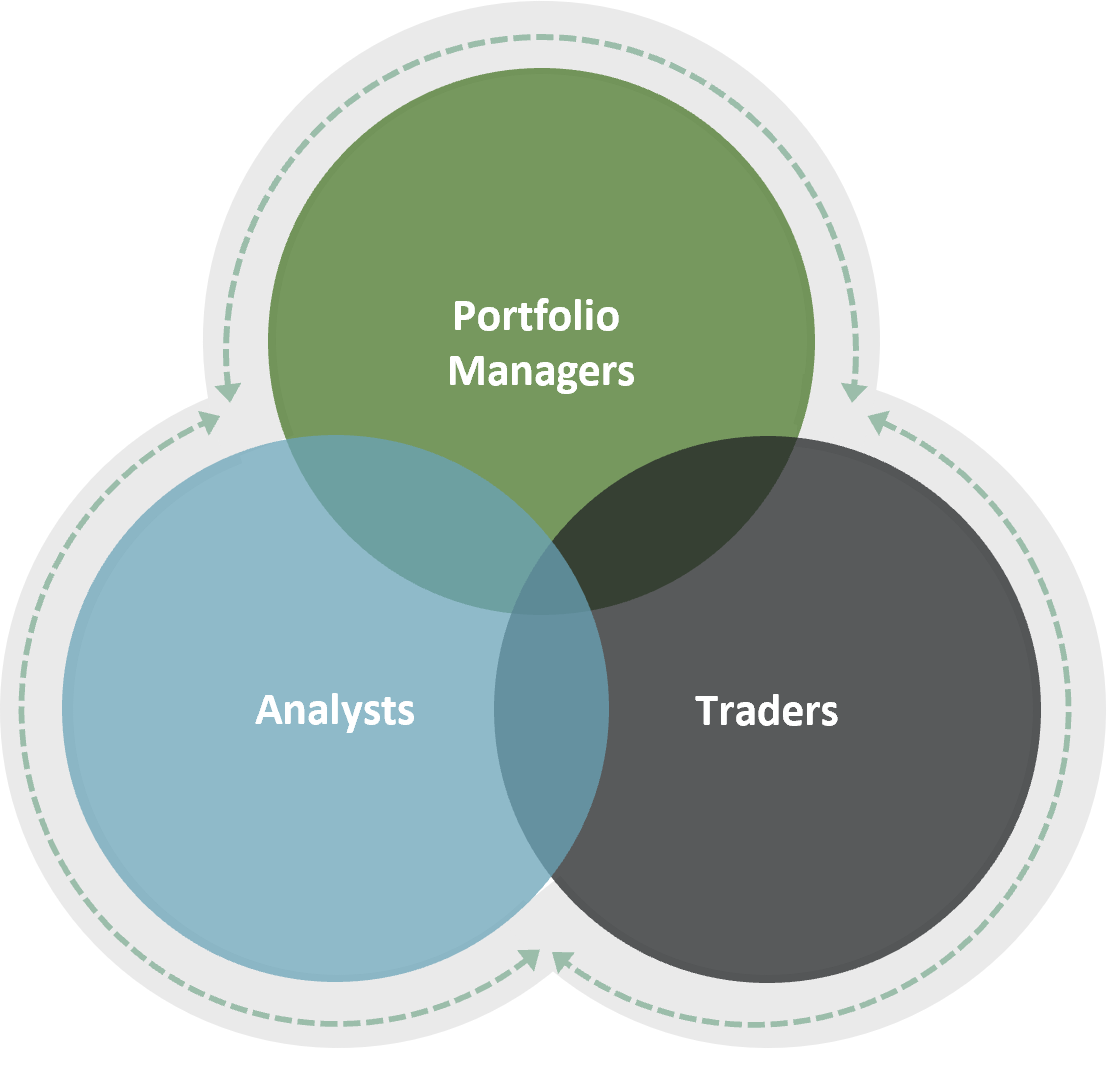

†Fidelity Investments, as of 12/31/25. Data is unaudited. Investment team members include portfolio managers, traders, and research analysts and associates.

Fidelity Fixed Income Division

- $2.5T+ Assets Under Management*

- 50+ years of experience

- 200+ team members†

55+ portfolio managers

- Lead the investment team

- Uses deep market experience to manage portfolios

- Ensure each strategy is managed to its specific objective

- Select appropriate bonds for individual client portfolios

130+ research analysts

- Identify attractive bonds and monitor existing holdings

- Conduct up front and ongoing credit quality analyses

- Assess individual issuers' value and outlooks

- Employ specialized tools and models

30+ professional traders

- Seek to improve returns by using proprietary technology and timely market knowledge

- Pursue flawless trade execution

Strives to balance income and price appreciation vs. risk

Using a research-based approach, the investment management team strives to avoid bonds that will not compensate bond holders for their investment risk.

To also help manage risk, the strategy will seek to maintain an average duration similar to that of. Bloomberg Managed Money Short Term (1-5) Municipal Bond Index.7 This index is a 1–5 year municipal bond index which typically has an average duration of 2-3 years.

In general, portfolios with shorter durations are less sensitive to changes in interest rates than portfolios with longer durations.

- Fully independent and proprietary research

- Leverage research across fixed income, high yield, and equity

- Analyze opportunities and risks using proprietary models and tools

- Invest in a broad range of investment-grade municipal bonds*

- Exposure to BBB rated bonds limited to 20% or less at time of purchase

- Seek to provide an experience consistent with client expectations

- Employ a total return approach—consider both yield and risk

- Emphasize opportunities that have price upside potential

- Strive to avoid bonds whose yields may not offset their risks

*At time of purchase

Tax-smart investing as part of active management

Active management and direct ownership of individual municipal bonds provide the portfolio team with flexibility to make tax-smart management decisions throughout the year. When appropriate, the team may identify and realize losses—an approach known as tax-loss harvesting—to help support after-tax efficiency.

How tax-loss harvesting works

If a bond in the portfolio declines in value, it can be sold at a loss. If a bond is sold at a loss, those losses may be used to offset realized gains elsewhere in a client’s portfolio. This can help reduce, defer, or in some cases eliminate certain taxable gains, depending on the investor’s individual tax situation. By keeping more of a client’s money invested, this strategy seeks to support long-term after-tax outcomes.

A year-round approach—not just at year-end

At Fidelity, tax-loss harvesting is viewed as an ongoing part of active management rather than a once-a-year activity. The investment team monitors markets and individual bonds throughout the year to look for tax-smart opportunities when they arise, always within the context of the strategy’s investment goals.

Important considerations

Tax-loss harvesting opportunities in municipal bond portfolios may be more limited than in equity strategies, as municipal bonds tend to be less volatile than equities with less potential for loss realization. Because of this, results can vary, and tax-loss harvesting may not always be available or beneficial. Investors should consult a tax professional regarding their specific situation. Please refer to the Fidelity Bond Strategies Form ADV, Part 2A Brochure and Supplemental Information for more information on tax management practices, including risks.

Fidelity's Fixed Income division believes investment success is a function of teamwork—involving portfolio managers, quantitative analysts, credit analysts and traders. Their investment team will actively manage your account, putting their knowledge, experience, and resources to work as they seek to uncover opportunities in all types of markets.

Source: Fidelity Investments.

How we select bonds for your account

The investment team looks at many factors when assessing risk for each proposed bond, including but not limited to, issuer specific credit risk, sector risk, interest rate risk, and liquidity risk.

The team assigns a proprietary credit rating to each bond they purchase, which is independent of the rating agencies. The team focuses on selecting investment-grade bonds that offer strong relative value in an effort to generate income while seeking to limit risk to the money invested.

Each account is diversified across a variety of sectors and maturities to help ensure it is not concentrated in any one area, can better handle changes in interest rates, and potentially helps reduce overall risk to principal over the long term.

Diversification does not ensure a profit or guarantee against loss.

Do we hold bonds to maturity?

Bonds can be sold prior to maturity when market opportunities or portfolio needs arise. One common reason is to help maintain the portfolio’s target duration. As bonds get closer to maturity, their duration naturally shortens, which can change how the portfolio behaves. By periodically replacing shorter-maturity bonds with longer-maturity bonds, we help keep the portfolio aligned with its stated duration objective.

While the investment team manages the portfolio with a focus on maintaining low turnover, trades may be made to enhance return potential and manage risk. These decisions are typically driven by factors such as changes in credit quality, relative value opportunities through security selection, strategic yield curve positioning, or evolving cash flow needs.

In certain market environments, portfolio managers may also realize losses for tax purposes when appropriate. This practice—known as tax-loss harvesting—involves selling a bond at a loss to help offset taxable gains elsewhere in the portfolio, with the goal of improving after-tax efficiency. If realized losses exceed gains in a given tax year, up to $3,000 may be used to offset ordinary income. Any remaining losses can generally be carried forward to future tax years, subject to IRS rules.