Fidelity® Limited Duration Bond StrategyA separately managed account providing investment-grade bond exposure through a diversified mix of individual bonds and a Fidelity mutual fund, which seeks to deliver interest income while balancing risk and return. This actively managed strategy looks to maintain an average target duration1 of 2 to 3 years. |

Investment objective: Seeks to deliver interest income, while limiting risk to principal over a full market cycle

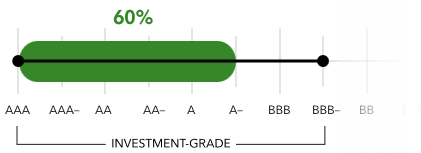

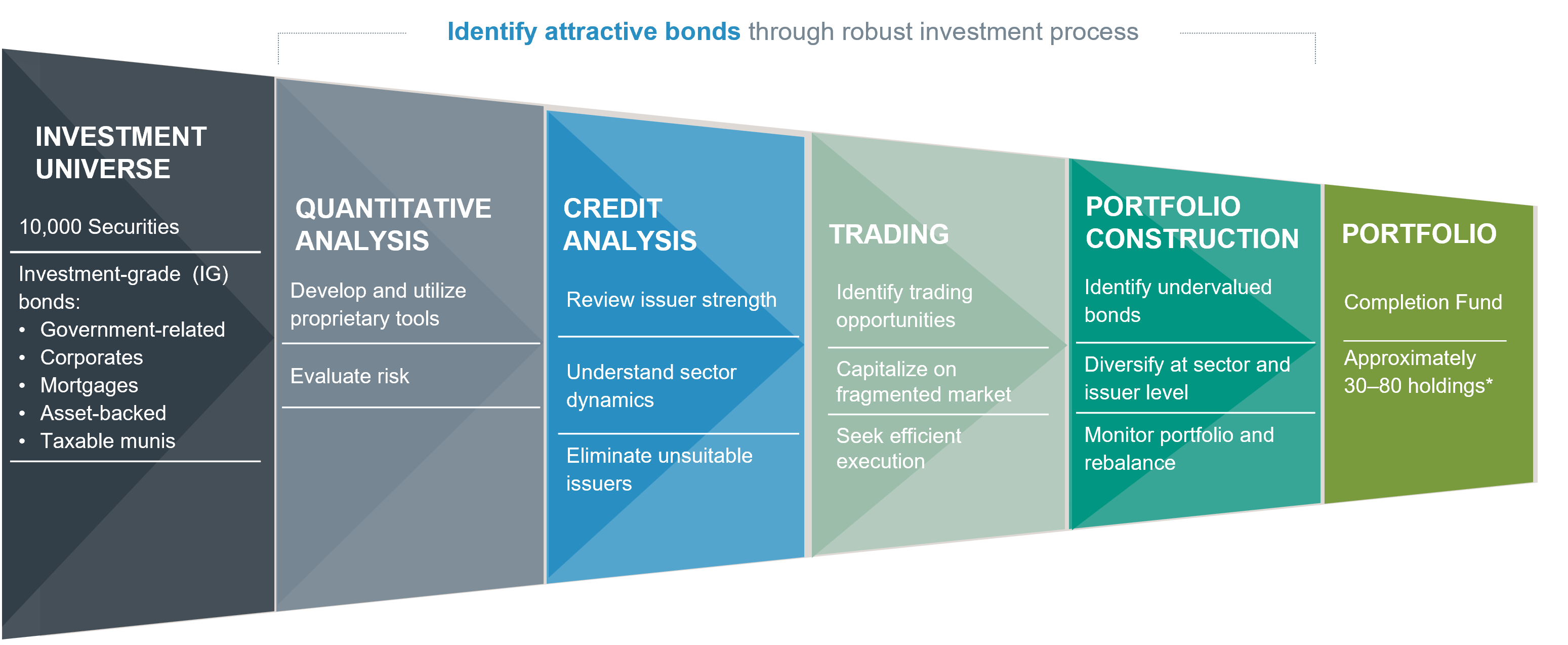

Types of investments: Primarily A- or higher investment-grade2 taxable bonds at time of purchase and a completion fund3

Investment minimum: $200,0004

Eligible Registration Types: Retirement & Taxable

Gross annual advisory fee: 0.35% – 0.40%5 (varies based on total assets invested)

Where Deep Research Meets Disciplined Active Bond Management

- Designed to help you pursue interest income with confidence

Built for investors seeking a professionally managed intermediate duration bond portfolio with a high-quality overall credit profile—targeting an average credit rating of A- or better and investing only in bonds rated BBB- or higher at the time of purchase—while aiming to pursue higher interest income. The Strategy also maintains a disciplined focus on diversification and risk awareness.

- Active oversight to help navigate evolving market conditions

Active management provides the investment team with the flexibility to make timely adjustments as market conditions change—including the ability to buy or sell bonds before maturity—seeking to identify opportunities and manage risk in support of the strategy’s objectives.

- Research depth that supports informed investment decisions

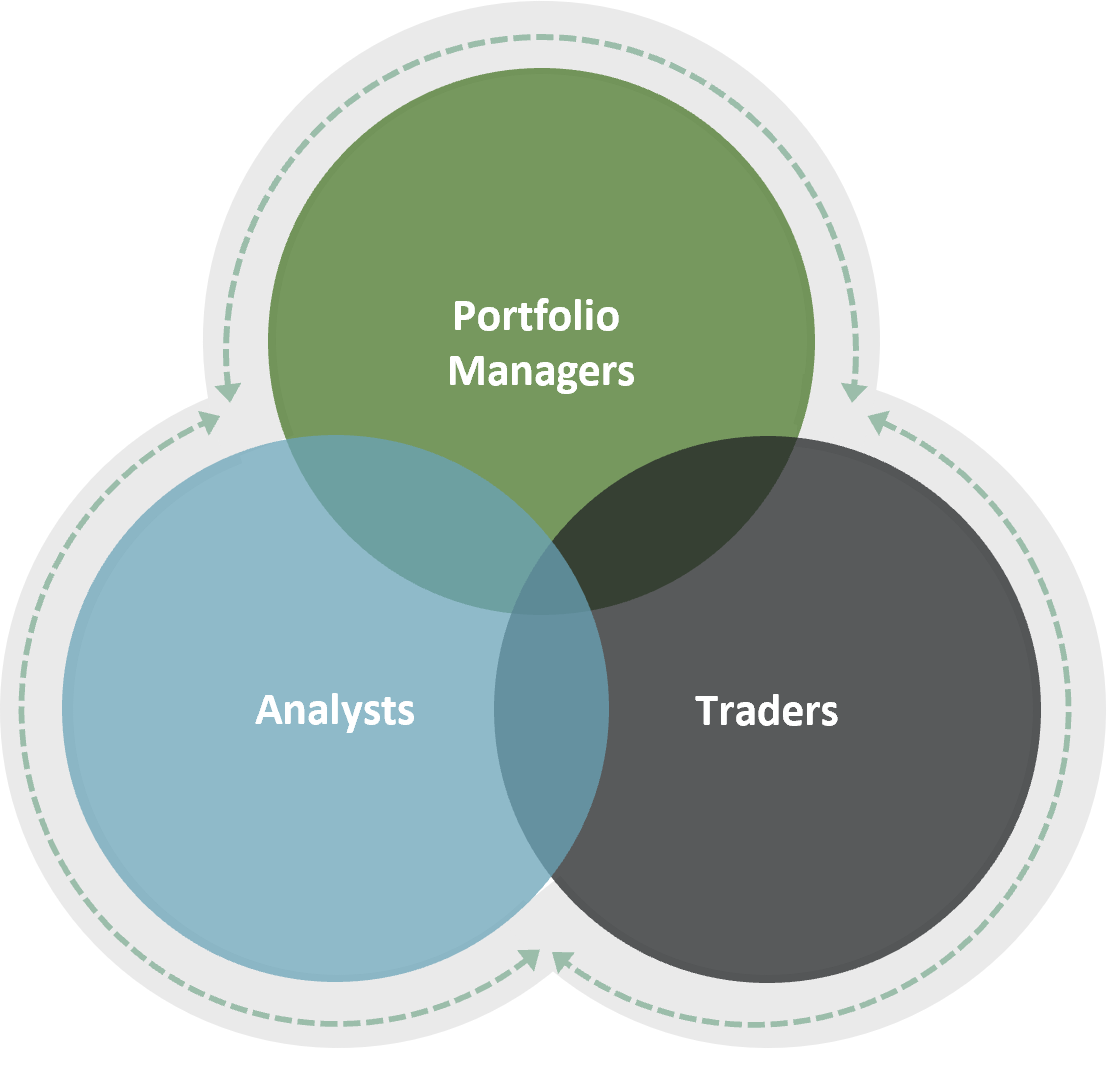

Every bond considered for the portfolio is evaluated through Fidelity’s extensive fixed income research platform, combining insights from analysts, portfolio managers, and credit specialists. This integrated approach helps identify opportunities and potential risks that may not be immediately evident to the broader market.

- Diversified drivers of potential return

The strategy seeks to generate returns from both ongoing income and the potential for price movement, emphasizing bonds that offer what the team views as a balanced combination of opportunity and risk. This approach supports the broader objective of helping investors stay aligned with their long-term goals.

- Tax management through direct ownership

For taxable accounts only, direct ownership of individual taxable bonds enables the strategy to use tax-smart techniques6—such as tax-loss harvesting when appropriate—to help support after-tax efficiency.

About the strategy

Pursue interest income through high-quality limited-term bonds

- Target average rating7: Primarily A- or higher

- Minimum credit quality: Bonds rated BBB- or better at purchase. No more than 40% of the account may be invested in bonds rated below A- at purchase.

- Average target duration: 2 to 3 years

- Maturities: Bonds generally maturing within 10 years

- Number of holdings: Typically, 30—80 individual bonds‡ complemented by Fidelity® Limited Term Securitized Completion Fund

‡ Number of portfolio holdings dependent on overall portfolio size.

Expected range of credit quality of the bonds in your SMA

Access to multiple bond sectors in one strategy

The Strategy invests in a diverse mix of investment-grade bonds across a range of sectors and varying maturities.

A decline in one sector could hopefully be offset by a gain in another, which may help smooth out portfolio volatility.

Specialized bond-market exposure, delivered through a mutual fund

To gain exposure to the securitized segment of the bond market—an area traditionally dominated by institutional investors—the Strategy utilizes the Fidelity® Limited Term Securitized Completion Fund (FLTGX). This zero-fee mutual fund offers access to a professionally managed portfolio of shorter-duration securitized fixed income instruments, such as asset-backed securities (ABS), commercial mortgage-backed securities (CMBS), and mortgage-backed securities (MBS).

The Strategy will typically maintain approximately 10%8 of the portfolio in FLTGX, though allocations may vary over time based on market conditions and portfolio positioning. The mutual fund structure offers daily liquidity and operational efficiency, making it a flexible and effective way to access this specialized sector.

Benefits of using FLTGX within the Strategy

- Broader income potential: Securitized bonds may offer higher yields than government bonds.

- Greater access for individual investors: Many securitized bonds are typically available only to large institutions or require high minimum investments. FLTGX offers a way for individual investors to access this segment of the market without those traditional barriers.

- Expanded diversification: Securitized bonds are backed by assets consumer loans, commercial real estate, and home mortgages—areas not typically represented in government or corporate bonds. Including them in a portfolio through FLTGX can help diversify sources of return and risk while maintaining the strategy’s short maturity profile.

Tapping Fidelity's Fixed Income expertise

Strategic Advisers LLC (Strategic Advisers), has engaged Fidelity Management & Research Company LLC (FMR), a registered investment adviser and a Fidelity Investments company, to provide the day-to-day discretionary portfolio management of Fidelity Limited Duration Bond Strategy accounts, including investment selection and trade execution, subject to Strategic Advisers’ oversight.

FMR brings investors a rich history of managing fixed income investments for over 50 years.

Using proprietary research, models, and tools, FMR can analyze thousands of securities across the investment-grade taxable bond universe.

This capability allows them to:

- Build a diversified taxable bond strategy

- Support income generation

- Balance risk and return potential

- Help keep your account aligned with your preferences

- Apply a disciplined tax-loss harvesting process (for taxable accounts only)6, when appropriate, to help enhance after-tax efficiency while maintaining the strategy’s objectives.

*Fidelity Investments, as of 12/31/25. Data is unaudited. Fidelity fixed income assets include investment-grade and high-income products, and money market cash management vehicles.

†Fidelity Investments, as of 12/31/25. Data is unaudited. Investment team members include portfolio managers, traders, and research analysts and associates.

Strives to balance income and price appreciation vs. risk

Fidelity Limited Duration Bond Strategy considers both income and price appreciation as potential sources of return and seeks bonds with a favorable risk/reward trade-off. Using a research-based approach, the investment management team strives to avoid bonds that will not compensate bond holders for their investment risk.

To also help manage risk, the strategy will seek to maintain an average duration similar to that of the Bloomberg US 1-5 Year Credit/Government Bond Blend Index.9

In general, portfolios with shorter durations are less sensitive to changes in interest rates than portfolios with longer durations.

- Fully independent and proprietary research

- Leverage research across fixed income, high yield, and equity

- Analyze opportunities and risks using proprietary models and tools

- Invest in a broad range of investment-grade bonds at time of purchase

- Invest in a completion fund providing liquidity and diversified exposure to securitized bonds

- Exposure to BBB rated bonds limited to 40% or less at time of purchase

- Seek to provide an experience consistent with client expectations

- Employ a total return approach—consider both yield and risk

- Emphasize opportunities that offer income generation, capital preservation and liquidity

- Strive to avoid bonds whose yields may not offset their risks

Tax-smart investing as part of active management

For taxable accounts only, active management and direct ownership of individual bonds provide the portfolio team with flexibility to make tax-smart management decisions throughout the year. When appropriate, the team may identify and realize losses—an approach known as tax-loss harvesting—to help support after-tax efficiency.

How tax-loss harvesting works

If a bond in the portfolio declines in value, it can be sold at a loss. If a bond is sold at a loss, those losses may be used to offset realized gains elsewhere in a client's portfolio. This can help reduce, defer, or in some cases eliminate certain taxable gains, depending on the investor's individual tax situation. By keeping more of a client’s money invested, this strategy seeks to support long-term after-tax outcomes.

A year-round approach—not just at year-end

At Fidelity, tax-loss harvesting is viewed as an ongoing part of active management rather than a once-a-year activity. The investment team monitors markets and individual bonds throughout the year to look for tax-smart opportunities when they arise, always within the context of the strategy’s investment goals.

Important considerations

Tax-loss harvesting opportunities in bond portfolios may be more limited than in equity strategies, as bonds tend to be less volatile than equities with less potential for loss realization. Because of this, results can vary, and tax-loss harvesting may not always be available or beneficial. Investors should consult a tax professional regarding their specific situation. Please refer to the Fidelity Bond Strategies Form ADV, Part 2A Brochure and Supplemental Information for more information on tax management practices, including risks.

Fidelity's Fixed Income division believes investment success is a function of teamwork—involving portfolio managers, quantitative analysts, credit analysts and traders. Their investment team will actively manage your account, putting their knowledge, experience, and resources to work as they seek to uncover opportunities in all types of markets

Source: Fidelity Investments.

Why will my account hold a Fidelity mutual fund?

The Fidelity® Limited Term Securitized Completion Fund (FLTGX) offers access to a professionally managed portfolio of securitized fixed income instruments—including mortgage-backed securities (MBS), commercial mortgage-backed securities (CMBS), and asset-backed securities (ABS).

These types of securities can provide distinct risk and return characteristics compared to traditional corporate or government bonds. By incorporating FLTGX, your portfolio gains exposure to a segment of the bond market that is typically less accessible to individual investors. Additionally, the mutual fund structure provides benefits such as daily liquidity and operational efficiency.

This addition supports the ongoing effort to enhance diversification within your Limited Duration Bond SMA, helping to broaden exposure across different fixed income sectors.

How we select bonds for your account

The investment team looks at many factors when assessing risk for each proposed bond, including but not limited to, issuer specific credit risk, sector risk, interest rate risk, and liquidity risk.

The team assigns a proprietary credit rating to each bond they purchase, which is independent of the rating agencies. The team focuses on selecting investment-grade bonds that offer strong relative value in an effort to generate income while seeking to limit risk to the money invested.

Each account is diversified across a variety of sectors and maturities to help ensure it is not concentrated in any one area, can better handle changes in interest rates, and potentially helps reduce overall risk to principal over the long term.

Diversification does not ensure a profit or guarantee against loss.

Do we hold bonds to maturity?

Bonds can be sold prior to maturity when market opportunities or portfolio needs arise. One common reason is to help maintain the portfolio’s target duration. As bonds get closer to maturity, their duration naturally shortens, which can change how the portfolio behaves. By periodically replacing shorter-maturity bonds with longer-maturity bonds, we help keep the portfolio aligned with its stated duration objective.

While the investment team manages the portfolio with a focus on maintaining low turnover, trades may be made to enhance return potential and manage risk. These decisions are typically driven by factors such as changes in credit quality, relative value opportunities through security selection, strategic yield curve positioning, or evolving cash flow needs.

For taxable accounts only, in certain market environments, portfolio managers may also realize losses for tax purposes when appropriate. This practice—known as tax-loss harvesting—involves selling a bond at a loss to help offset taxable gains elsewhere in the portfolio, with the goal of improving after-tax efficiency. If realized losses exceed gains in a given tax year, up to $3,000 may be used to offset ordinary income. Any remaining losses can generally be carried forward to future tax years, subject to IRS rules.