1. Fidelity® Strategic Disciplines (FSD) clients must generally qualify for support from a dedicated Fidelity advisor, which is based on a variety of factors (for example, a client with at least $500,000 invested in an eligible Fidelity account(s) would typically qualify). Account investment minimum is $100,000 for an FSD equity strategy, and $200,000 for taxable bond strategies and $250,000 for municipal bond strategies.

2. The advisory fee does not cover charges resulting from trades effected with or through broker-dealers other than Fidelity Investments affiliates, markups or markdowns by broker dealers, transfer taxes, exchange fees, regulatory fees, odd lot differentials, handling charges, electronic fund and wire transfer fees, or any other charges imposed by law or otherwise applicable to your account. You will also incur underlying expenses associated with the investment vehicles selected.

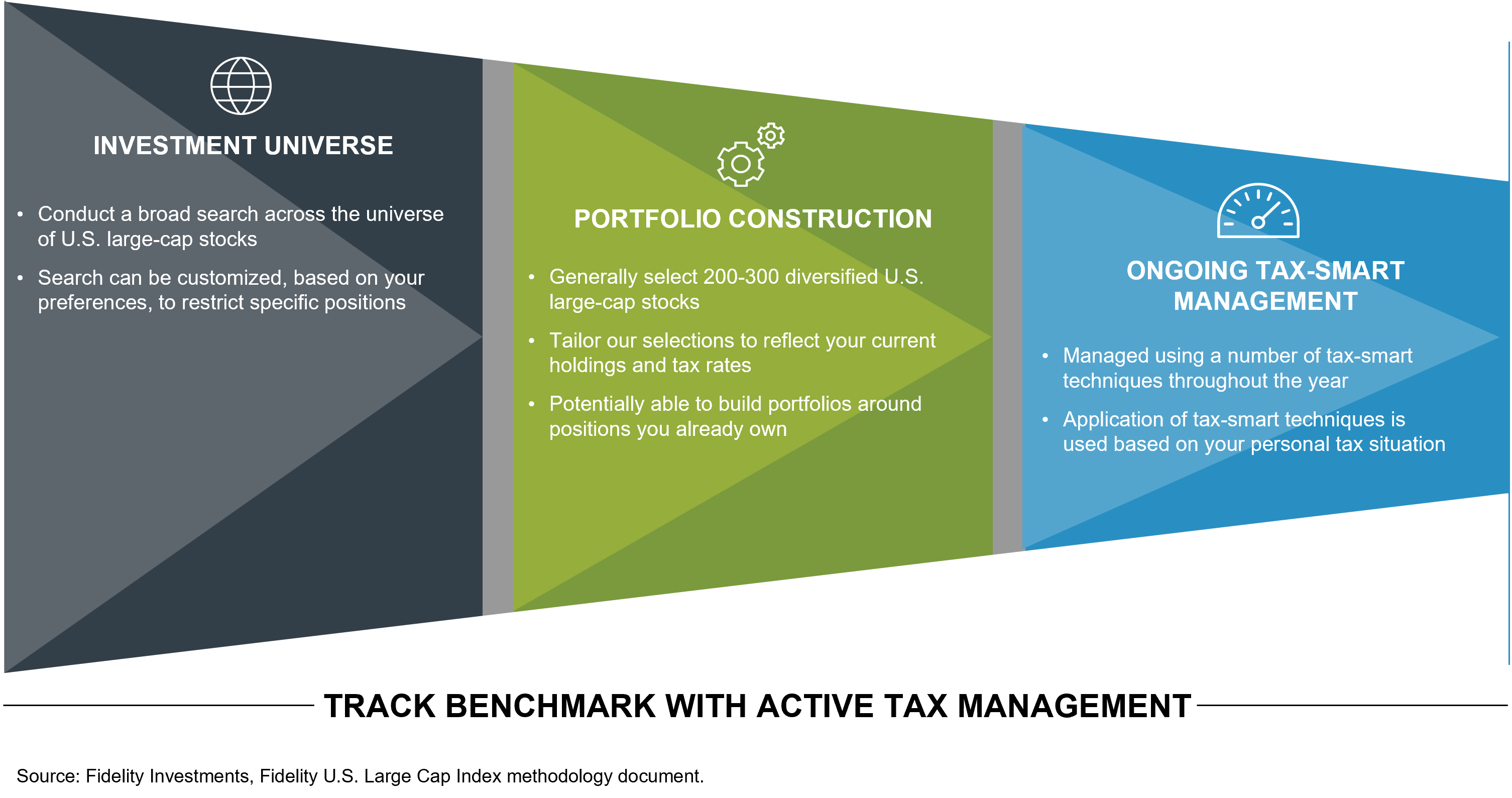

3. Tax-smart (i.e., tax-sensitive) investment management techniques (including tax-loss harvesting) are applied in managing certain taxable accounts on a limited basis, at the discretion of the portfolio manager primarily with respect to determining when assets in a client's account should be bought or sold. As the discretionary portfolio manager, Strategic Advisers LLC ("Strategic Advisers") may elect to sell assets in an account at any time. A client may have a gain or loss when assets are sold. There are no guarantees as to the effectiveness of the tax-sensitive investment techniques applied in serving to reduce or minimize a client's overall tax liabilities, or as to the tax results that may be generated by a given transaction. Strategic Advisers does not currently invest in tax-deferred products, such as variable insurance products, or in tax-managed funds, but may do so in the future if it deems such to be appropriate for a client. Strategic Advisers does not actively manage for alternative minimum taxes; state or local taxes; foreign taxes on non-U.S. investments; federal tax rules applicable to entities; or estate, gift, or generationskipping transfer taxes. Strategic Advisers relies on information provided by clients in an effort to provide tax-sensitive investment management, and does not offer tax advice. Except where Fidelity Personal Trust Company (FPTC) is serving as trustee, clients are responsible for all tax liabilities arising from transactions in their accounts, for the adequacy and accuracy of any positions taken on tax returns, for the actual filing of tax returns, and for the remittance of tax payments to taxing authorities.

4. Tax savings will vary from client to client and past performance is no guarantee of future results; there is no guarantee that tax savings will cover the net advisory fee now or in the future. Factors that could impact the value of our tax-smart investing strategies include market conditions, the purchase date, and cost basis of any securities used to fund an account, client-imposed investment restrictions, client tax rate, and any changes in tax regulation. This analysis is based on performance of all investment strategies offered in Fidelity Managed FidFolios® and substantially similar strategies offered through Fidelity® Strategic Disciplines from 08/01/2015 through 12/31/25. The analysis includes identifying the total amount of capital gains tax savings for each individual client account, and the total amount of net advisory fees paid for each individual client account (accounts that did not pay a fee were excluded from the analysis). We estimate potential capital gains tax savings by multiplying each harvested tax loss by the relevant short- or long-term capital gains tax rate for each client account at the end of each year. Our analysis assumes that any losses realized are able to be offset against gains realized inside or outside of the client account during the year realized. However, all capital losses harvested in a single tax year may not result in a tax benefit for that year. Remaining unused capital losses may be carried forward to offset up to $3,000 of ordinary income per year.

5. We believe that appropriate diversification is of primary importance and apply tax-smart investing techniques as a secondary consideration. Accordingly, clients who fund an account with appreciated securities should understand that we could sell such securities notwithstanding that the sale may trigger significant tax consequences within an account managed with tax-smart investing techniques.

The Fidelity U.S. Large Cap Index℠ is a float-adjusted market capitalization–weighted index designed to reflect the performance of the stocks of the largest 500 U.S. companies based on float-adjusted market capitalization.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Stock markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. Investing in stock involves risks, including the loss of principal.

Indexes are unmanaged. It is not possible to invest directly in an index. Securities indices are not subject to fees and expenses typically associated with managed accounts.

The Fidelity U.S. Large Cap Index℠ is a float-adjusted market capitalization–weighted index designed to reflect the performance of the stocks of the largest 500 U.S. companies based on float-adjusted market capitalization.

Fidelity® Strategic Disciplines provides nondiscretionary financial planning and discretionary investment management for a fee. Fidelity® Strategic Disciplines includes the Fidelity® U.S. Large Cap Index Strategy. Advisory services offered by Strategic Advisers LLC (Strategic Advisers), a registered investment adviser. Brokerage services provided by Fidelity Brokerage Services LLC (FBS), and custodial and related services provided by National Financial Services LLC (NFS), each a member NYSE and SIPC. Strategic Advisers, FBS, and NFS are Fidelity Investments companies.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

© 2026 FMR LLC. All rights reserved.