Fidelity® Dividend Income StrategyA separately managed account that seeks to provide dividend yield and total return greater than that of S&P 500 with the potential for less volatility than the U.S. stock market by investing primarily in large cap stocks. The strategy uses tax-smart strategies in an effort to enhance after-tax returns in taxable accounts.4 |

Investment strategy: Focuses on higher-quality dividend-paying stocks that have the potential to sustain and grow dividends over time

Types of investments: Primarily higher-quality dividend-paying stocks1 within the S&P 500® Index

Investment minimum: $100,0002

Eligible Registration Types: Taxable & Retirement

Gross annual advisory fee: 0.30%–0.70%3 (varies based on total assets invested)

Strategic Advisers LLC (Strategic Advisers) will actively manage the strategy in an effort to deliver long-term capital growth and dividend income greater than the S&P 500® Index. They seek securities primarily from a diversified core of dividend paying companies and supplement the portfolio with those securities of either companies transitioning to a more of quality dividend-orientation or those they find that provide a unique opportunity to offer value.

The strategy may hold securities of varying types:

- Large-cap and established dividend-paying companies

- Generally a diversified and financially sound business

- Stable dividend growth

- Strong growth potential for free cash flow growth

- Building history of dividend growth

- Potentially out of favor cyclically

- Fidelity's differentiated view

- Intrinsically undervalued

- Special situations

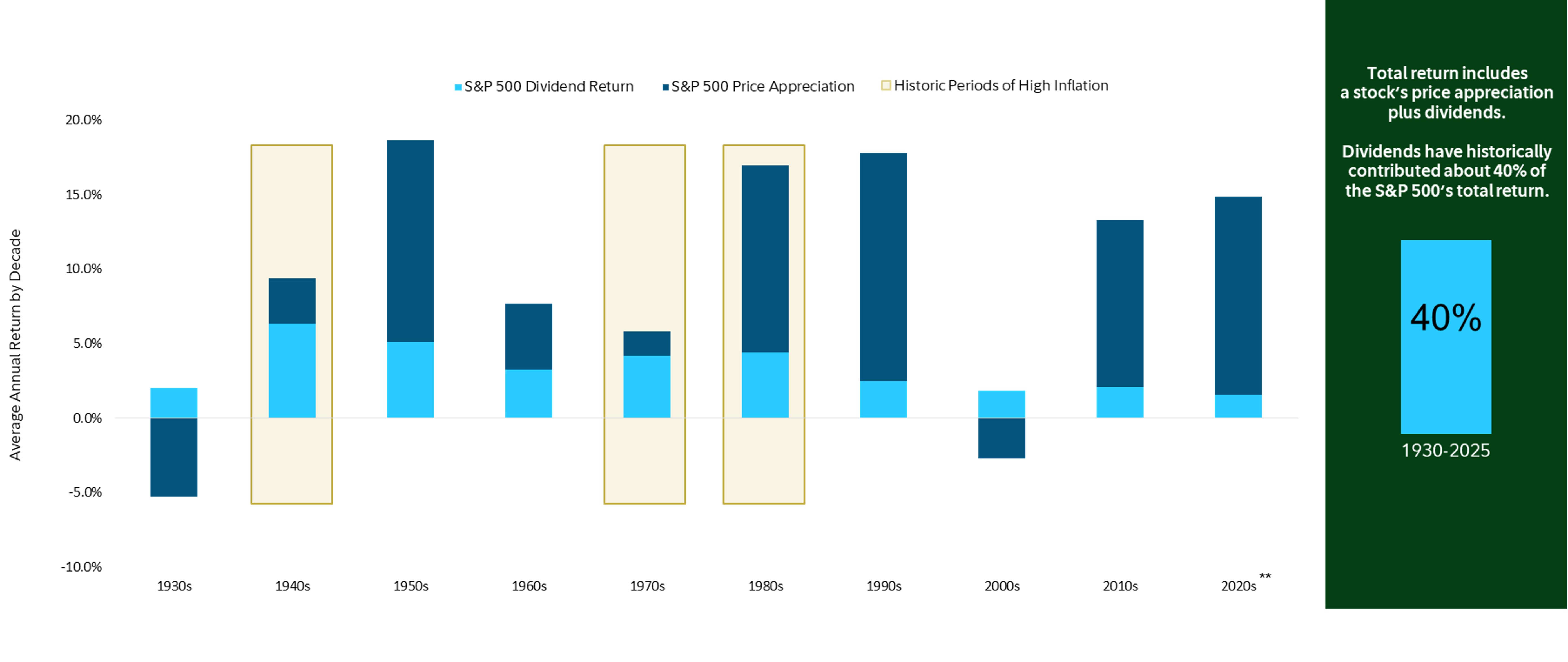

Stocks that pay dividends have been a key contributor to the S&P 500's total return*

Dividends have historically made positive contributions to total stock market return, even during periods of higher inflation. As shown below, dividends have produced approximately 40% of the S&P 500's total return over time, with the remainder coming from price appreciation (the increase in a stock's value). This powerful combination of income and growth may help provide increased long-term returns.

Source: Bureau of Labor Statistics, Fidelity Investments, and Morningstar, as of 12/31/25.

**2020s data is from 1/1/2020 to 12/31/2025.

For each decade, the total return for the S&P 500 was calculated and then converted into an average annual return number. The total return for each decade was also decomposed into its two constituent parts: price appreciation and dividend income. The bars for each decade represent annualized total return, annualized return from price appreciation only, and annualized return from dividends (which are assumed to be reinvested in the index).

S&P 500 is a registered service mark of Standard & Poor's Financial Services LLC. It is a market capitalization–weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance

A history of weathering different market conditions

Companies that have paid stable dividends are often well-run, high-quality businesses. As a result, these high-dividend-paying stocks* have a history of competitive returns, with dividends contributing to returns even in down markets. High-dividend-paying stocks also have had less volatility than stocks that did not pay dividends†, making for the potential of less extreme ups and downs when participating in the long-term growth of the stock market.

High-dividend-paying stocks had attractive returns and lower volatility (1994–2025)†

* High-dividend-paying stocks represent the top third of S&P 500® stocks by dividend yield.

† Volatility as measured by standard deviation. Standard deviation is a measure of the dispersion of a set of values from its mean. It is an annualized figure that measures how much a return varies over an extended period of time. The more variable the returns, the larger the standard deviation. A higher standard deviation indicates a wider dispersion of past returns and thus greater historical volatility. Standard deviation indicates the volatility of the index return over time, not the actual performance of the index.

Past performance is no guarantee of future results. The index performance includes the reinvestment of dividends and interest income. An investment cannot be made in an index. Securities indices are not subject to fees and expenses typically associated with managed accounts. This chart is for illustrative purposes only and is not intended to represent the actual or future performance of any investment option or strategy.

The power of Fidelity's active management

Experienced and reliable with deep investment and research capabilities

Strategic Advisers LLC (Strategic Advisers) provides portfolio management capabilities for this strategy and has partnered with Fidelity Management & Research Company LLC (FMRCo) to leverage their investment research capabilities. FMRCo provides model holdings and Strategic Advisers executes the trades and provides ongoing active management of the portfolios, including the use of tax-sensitive investment management techniques.4

FMRCo leverages its in-depth experience, access to corporations, and proprietary tools to identify stocks they believe to be consistent with the investment strategy.

If held within a taxable account, your equity SMA will be managed in an effort to harness the long-term growth potential of stocks while seeking to enhance after-tax returns through the ongoing monitoring and application of tax-smart investing strategies.4 In fact, 94% of our clients investing in SMAs in taxable accounts have had their advisory fees covered by the tax savings provided.5

We take a disciplined and thoughtful approach to building and maintaining a portfolio focused on capital appreciation and dividend income, with the potential for less volatility than the US stock market, in an effort to help you achieve your financial goals. The investment team also provides day-to-day management looking for opportunities to apply tax-smart investing techniques that seek to help outperform the benchmark after-taxes in taxable accounts.