Thanks to providers like Fidelity, people can rely on easy, convenient systems to stay on track with their retirement savings. But when it comes to saving for important near-term goals (think: vacation, house, or wedding), people tend to be less organized. Some rely on a basic savings account and miss out on other options, like investing. Others lack visibility into how, when, or if they’ll reach their savings goals.

It’s no wonder, then, that many savers don’t see more returns from their savings, or worse, don’t reach their savings goals at all. What could we do to help people see more success with near-term savings? We talked to Emily Kolle, vice president of product management, to see how her internal startup approached building its solution.

What tends to derail people from their near-term savings goals?

Saving for the near term can be challenging because it’s not systematized, like retirement savings. Without more comprehensive support, savers often default to thoughtless systems that don’t keep them accountable, don’t give them a clear sense of their progress, and don’t help them think smarter about how they save and invest for a goal.

What about investing? Why don’t people invest to get more from their near-term savings?

Honestly, for many, it feels like something they aren’t meant to do. When people liken investing to gambling, they mean it. If you’re investing, and not sure that you should be, it can feel like you’re gambling at your chance to, say, get married, or buy a new home.

It feels safer to leave near-term savings in cash, like in a basic savings account at the bank with FDIC insurance.

And yet, one could be leaving hundreds of dollars on the table—if not thousands.

"Saving for the near term can be challenging because it's not systematized, like retirement savings." — Emily Kolle

Okay, so we’re trying to help people optimize their near-term savings. What solution did the team come up with?

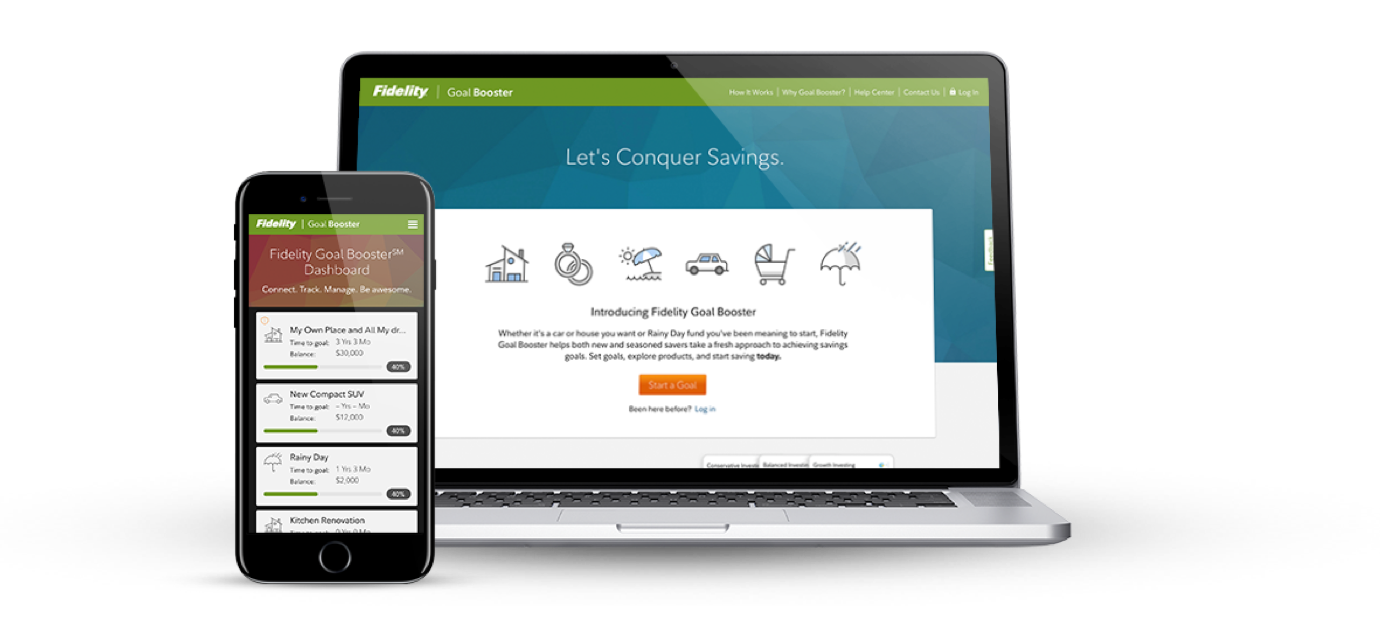

One easy-to-use platform for all of your near-term savings goals, whether you prefer a cash-based vehicle or want to try investing. We’d present a wider range of savings and investment options in a way that’s easy to understand. These would come with basic information, and pros and cons, so that savers could take action with confidence.

Any unexpected challenges in building this solution and going live with your first pilot customers?

Our biggest challenge was also our greatest responsibility. Fidelity must carefully vet and deliver written content that is clear, straightforward, and fully in line with any applicable laws or regulations. We also have a responsibility to our customers and users to avoid jargon and overwhelming, overly complex descriptions.

While this was not necessarily unexpected, it is sometimes startling to see how those two very important responsibilities can often feel like they are at odds.

"The words we use—the atmosphere we create in our product experience—can help you feel good about putting $50 towards your goal, instead of spending it on a night out." — Emily Kolle

The right language can be a real balancing act in our industry. But it can be an opportunity, too. Is there room for delight, maybe, in a product that helps people achieve their savings goals?

Delight plays such a big role! If you’re working hard to build up savings over a few years, sometimes it doesn’t feel like you’ll ever get there. The words we use—the atmosphere we create in our product experience—can help you feel good about putting $50 towards your goal instead of spending it on a night out.

The goal of the pilot phase is to prove the business model. What did a successful pilot look like for you?

We were doing something that people valued and needed. Very rarely did our customers mention using an existing short-term savings solution. More often, they just had a basic savings account at their bank. We developed a new way to bring the underlying Fidelity financial products to users—and made it easier for them to understand what our products could do for their goals.

What’s next for Fidelity Goal Booster?

In December 2019, we broadly released our product within our workplace channel to help retirement customers with their non-retirement goals. Now that we’ve moved beyond pilot into broad release, the next phase of this innovation adventure is to determine how to successfully integrate Goal Booster within the existing infrastructure of our core business.