If your income hasn't kept pace with inflation this year, you may soon get some financial relief in the form of a tax cut.

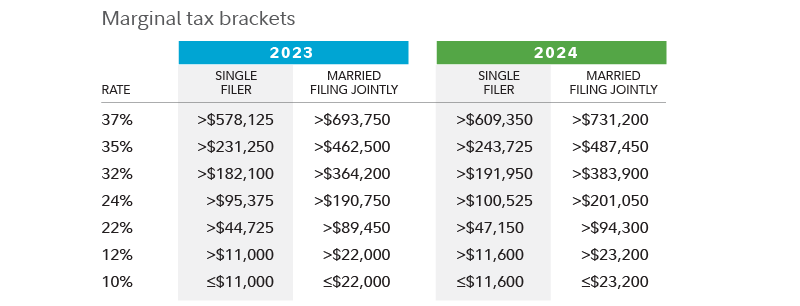

The Internal Revenue Service (IRS) has released adjustments to tax brackets for 2024, adding thousands of dollars to most marginal tax brackets, and potentially protecting more of your income from taxes next year. The 5.4% adjustment is lower than the 7.1% increase for 2023, but still one of the highest in years, and higher than the current rate of inflation.

Additionally, the standard deduction will rise. For married couples the bump up is $1,500 to $29,200. For single filers, it's an increase of $750 to $14,600. The adjustment reflects inflation through October 2023, and if your income didn't quite keep up with continuing price increases on everyday items from gas to groceries, the good news is you may find yourself with a bit more money after you settle your tax bill.

Why do tax brackets change?

The US has a progressive tax system, meaning as someone's income rises, it's taxed at a gradually increasing rate corresponding to 7 brackets, which rise like a set of steps. Every year the IRS announces changes to the tax brackets. Those changes are pegged to inflation, and the adjustments occur at roughly the same time the federal government makes changes to Social Security payments through the cost-of-living adjustment (COLA).

How the 2024 tax brackets might affect you

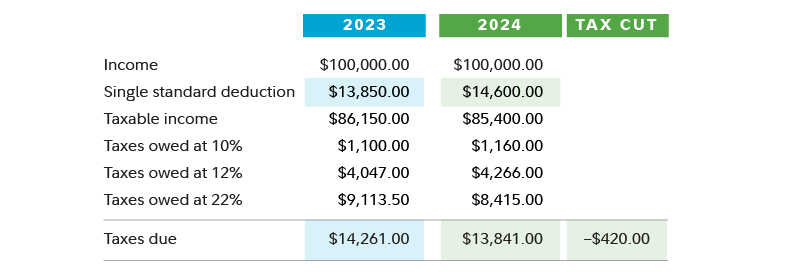

Here's how the changes might play out for an individual filer who earns $100,000 both in 2023 and 2024, and who takes the standard deduction in both years.

The $420 in savings is the result of the higher standard deduction, as well as a lower effective tax rate (the total percentage of income that is taxed.) As brackets widen, more of your taxable income is taxed at a lower rate.

While the changes affect everyone, they particularly have an impact on people whose income did not keep pace with inflation this year. Real weekly earnings decreased on average by 0.1% from September 2022 through September 2023, according to the US Department of Labor.1

Tactics to help manage tax bracket changes

There are 2 ways you can take deductions on your federal income tax return: You can itemize deductions or use the standard deduction. The standard deduction is a dollar amount preset by the IRS. Itemizing means adding up all the deductions you may qualify for, up to a certain limit that could be higher than the standard deduction.

- The higher standard deduction and the new tax brackets next year mean it may be better for more people to take the standard deduction. For example, if you itemized last year and your itemizations this year will be less than the higher $29,200 standard deduction for married couples, or $14,600 for single people, switching to the standard deduction could make sense.

- If you're close to the standard deduction cutoff, additional charitable contributions could make itemizing more worthwhile. If that's the case, and donating to charity is one of your goals, you could also consider a "bunching" strategy for 2023. That essentially entails combining all your charitable deductions for several years in a single year, enabling you to exceed the standard deduction next year, and potentially dropping you into a lower tax bracket. The following year, while you may not make charitable donations, you'd still qualify for the standard deduction, which could save you thousands of dollars in taxes over several tax years, while still making the same total charitable donations.

- Finally, if you've been thinking about a Roth conversion, next year might be a good time to do one. The new tax rates, combined with the recent fluctuations in stock prices, may mean the money you convert from a traditional IRA to a Roth could be taxed at a lower rate. A conversion for tax year 2024 might be particularly helpful for people who expect their tax rate to be higher in future years.

Important to know

An opportunity to save more in a 401(k)

In addition to tax savings, the IRS made adjustments to numerous other parts of the tax code that have an impact on retirement saving and more.

People who have access to a 401(k) plan through work can consider putting more money away next year, as the IRS also announced annual contribution limit increases for 2024. Participants in such plans can contribute $23,000 (pretax or to a Roth depending on plan rules), up from $22,500 in 2023. People 50 and older can make catch-up contributions of $7,500, the same as 2023.

2024 IRA contribution limits

IRA contribution limits have also increased to $7,000 for 2024, compared to $6,500 for 2023. (Catch-up contributions also did not change.)

Contributions to a traditional 401(k) or a traditional IRA can reduce your taxable income, and deferred amounts are not taxed until you begin withdrawals in retirement.

2024 HSA contribution limits

Lastly, the IRS also increased health savings account (HSA) annual contribution limits. The inflation adjustment lets individuals save $4,150 in 2024, up from $3,850 in 2023. For family coverage, contribution limits for next year have jumped to $8,300 from $7,750. Those 55 and older can contribute an additional $1,000 as a catch-up contribution, which is unchanged from 2023. HSAs can help people save for rising health care costs now and in retirement.

All in all, the tax changes for 2024 should help offset some of the pain from continuing inflation and help people save for retirement. To make the most of these changes as you plan for the end of 2023 and beyond, consider working with a tax professional.