Required minimum distributions (RMDs)

If you’ve reached age 731, it’s time to start withdrawals—the IRS requires you to begin taking Required Minimum Distributions (RMDs) from your IRA and workplace retirement accounts every year. That’ll mean new income that’s taxable, with stiff IRS penalties for not taking it on time. Let’s help you maximize this new income.

Why do I have to take an RMD?

- Traditional IRA

- Rollover IRA

- SIMPLE IRA

- Workplace plans, such as 401(k) or 403(b)

- SEP IRA

- Inherited IRA

- Inherited Roth IRA

- Profit sharing

- Money purchase

- Self-employed 401(k)

If you need help with an RMD for your inherited IRA, visit our Inherited IRA RMD page.

2 rules that help simplify things

Rule 1: Aggregating RMDs: RMDs are calculated separately for each of your retirement accounts. Seems like a lot to manage, but here’s an important rule making it a bit easier: If you have more than one IRA, you can total up their RMDs and withdraw it from a single IRA. Same thing for 403(b) accounts—you can take all their RMDs from a single 403(b). But there’s one big exception to the rule: 401(k)s. If you have more than one 401(k), you need to withdraw the RMD from each individual 401(k).

Rule 2: The Working Non-owner: Are you still working, while not owning more than 5% of the company? Then you generally do not have to take RMDs from your workplace retirement plan until you retire.

How is my RMD calculated?

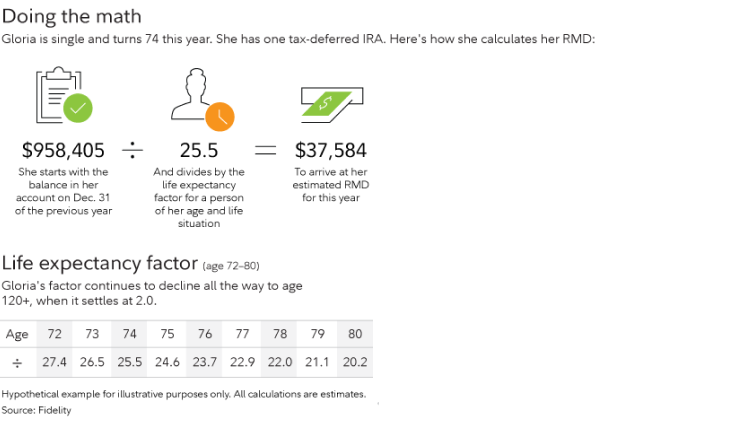

If you’re the original account owner, your RMD is calculated by dividing the account’s year-end balance from the prior year by your current year's life expectancy factor from the IRS Uniform Life Expectancy Table (PDF). Each year, your life expectancy factor and year-end balance will change—so your RMD amount will change each year, too.

One exception: Is your spouse more than 10 years younger—and have they been listed as the 100% primary beneficiary of your account for the entire year? Then lucky you: You can calculate your RMD using the IRS Joint Life Expectancy Table, which factors both your age and your younger spouse’s age, resulting in a longer life expectancy. The net result? Less money you’re required to withdraw as an RMD.

Guide to retirement distributions

Got all your retirement accounts at Fidelity? We’ve calculated your RMD for you.

RMD calculator

Not a Fidelity customer or have your retirement accounts at multiple firms? We’ll help you estimate your RMD.

When do I have to take my first RMD?

The deadline to withdraw your RMD is December 31st in the year you reach age 731. You can opt to delay your first RMD until April 1st of the year after you reached age 731.

December 31

April 1

December 31

Note: If you delay your first RMD until April, you'll have to take two RMDs your first year. The first will still have to be taken by April 1; the second, by December 31. You should consider the tax consequences of taking two RMDs in one year.

When do I have to take RMDs after my first one?

December 31

Deadline for withdrawing your RMD each year once you’ve taken your first RMD.

How do I withdraw my RMD?

When it’s time to withdraw RMDs from your Fidelity accounts, you have choices:

Move cash and/or shares to your Fidelity non-retirement account

Fidelity automatic withdrawal plan

Qualified Charitable Distribution

Electronic funds transfer (EFT) to your bank (instructions must already be on file). Link your bank nowLog In Required

Bank wire

Check via US Mail

Get started today by withdrawing your RMD from your Fidelity IRA.

Fidelity can calculate your RMD and send it to your Fidelity non-retirement account or bank automatically.

With so many options for taking your RMDs, Fidelity can’t assume you want us to automatically distribute them—so, you do need to sign up for a Fidelity RMD automatic withdrawal planLog In Required. Ultimately, the responsibility to satisfy your RMD requirements lies with you.

Looking for ways to keep your money working for you?

Qualified Charitable Distribution (QCD)

If making charitable donations is important to you, using your RMD to make a qualified charitable distribution (QCD) is something to consider. As long as certain requirements are met, the IRS allows you to exclude up to $100,000 in IRA withdrawals (if paid directly to a qualified charity) from income each year. QCDs also count toward your RMD.

For more information on QCDs or to send a QCD from you account, see our Qualified Charitable Distributions information.

Send a QCD from your accountLog In Required

Taxes

The IRS taxes RMDs as ordinary income. This means withdrawals will count toward your total taxable income for the year, and they will be taxed at your applicable individual federal income tax rate. They may also be subject to state and local taxes.

If your IRA balance includes after-tax contributions, you must calculate your RMD based on the total balance; however, the taxable amount of your RMD will be reduced proportionally by the percentage of after-tax money in your IRA accounts. If you need help calculating the after tax portion of your IRAs, the instructions for IRS Form 8606 are a good place to start.

Keep in mind: The additional income from your RMD may increase your federal, state, and local taxes as well as the taxes you pay for Social Security and Medicare.

Missed RMD

It is important to complete your RMD by the required deadline. The IRS penalty for late withdrawals is 50% for calendar years 2022 and earlier.

If you have missed a part or all of your RMD you must report it on Form 5329 and file it with your 1040 (you cannot use the 1040A if you file Form 5329). For help with this tax form, see the IRS Instructions for Form 5329 (PDF)Log In Required.

SECURE 2.0 Act of 2022 reduced the late withdrawal penalty from 50% to 25% and also allows for an additional reduction to 10%, if the late withdrawal is removed from the account by the appropriate deadline. The reduced penalty applies to late withdrawals for calendar years 2023 and later.

Don't miss future RMDs, sign up for a Fidelity RMD automatic withdrawals planLog In Required.

How Fidelity can help you plan

If you’re considering withdrawing from your IRA, we can help:

Understand potential ways to use your RMDs

Understand potential ways to use your RMDs

Fidelity Viewpoints

Consolidate your retirement accounts

Consolidate your retirement accounts to help make RMDs easier*

Consolidate your accountsLog In Required

Get a holistic view of your retirement income plan

Get a holistic view of your retirement income plan, including how long your money may last, with our Planning & Guidance Center

Planning & Guidance Center

Schedule an appointment

Our experienced representatives can help you create a plan and adjust your portfolio.

Schedule an appointment